You open your inbox and see a note from your payment processor asking you to complete PCI paperwork. You didn't start a café, clinic, online store, or software business because you wanted to decode security questionnaires. Yet now someone wants to know where card data travels, who can see it, what systems touch it, and whether your vendors can prove they're doing their part.

That's where most businesses get stuck. Not on the idea of security itself, but on the practical questions: what exactly is in scope, which supplier documents matter, why does your website host, payment gateway, IT provider, and booking platform suddenly belong in the same conversation.

PCI DSS regulatory compliance gets presented as a list of controls. For many owners, that list is the least confusing part. Actual friction sits elsewhere: scoping, vendor management, and evidence collection. If you can get those three right, the rest becomes far more manageable.

Why PCI DSS Compliance Is Not Just an IT Problem

A familiar pattern goes like this. A business starts taking card payments through a website, point-of-sale device, or phone orders. Payments work. Revenue comes in. Then an acquirer, processor, or bank asks for PCI validation. The owner forwards it to IT. IT asks which systems are in scope. Finance asks who owns the merchant account. Operations asks whether the booking tool stores anything. Nobody has the full picture.

That confusion happens because PCI DSS feels technical on the surface, but the obligation starts as a business commitment. PCI DSS is not a statute. It is a contractual security standard enforced through card-brand and acquiring-bank agreements, and merchants that store, process, or transmit payment cards must implement the 12 PCI DSS control families, including network security controls, encryption in transit, access restriction, logging, and regular testing, as explained in this overview of PCI compliance obligations.

Why owners get pulled into it

PCI questions quickly move beyond the server room.

Contracts matter: Your merchant agreement can create obligations even if you outsource most of the payment flow.

Process choices matter: A receptionist taking card details by phone creates a different risk profile than a hosted checkout page.

Vendor choices matter: A cloud app, payment form, or managed support provider can expand or reduce your compliance burden.

Practical rule: If your business accepts card payments, PCI DSS belongs to leadership, operations, finance, procurement, and IT. Not just the technical team.

A good way to think about it is this. IT installs locks. The business decides how many doors exist, who gets keys, and which third parties can walk through them.

That's also why infrastructure decisions deserve business-level attention. Reliability and security often overlap in ways owners can feel directly, especially when payment systems sit on customer-facing platforms. This guide to business hosting reliability is useful because it frames hosting as an operational decision, not a back-office checkbox.

The real business reason behind the rules

PCI DSS exists to reduce the chance that payment data is exposed, mishandled, or left unguarded. Customers never see your segmentation diagram or access log. They only notice whether your business feels safe to buy from.

That's why PCI DSS regulatory compliance shouldn't be treated like annual paperwork. It's closer to basic financial control. You wouldn't let anyone edit payroll records without oversight. Card data deserves the same discipline.

Decoding The Core Concepts of PCI DSS

PCI DSS stands for Payment Card Industry Data Security Standard. In plain language, it's the security baseline for organisations that store, process, or transmit payment card data. The standard has moved from a broad industry framework into a structured compliance regime with clearly defined merchant tiers and 12 core security requirements, as outlined in this PCI compliance reference.

The first concept to understand is scope.

Think of the CDE as a secure room

The Cardholder Data Environment, usually shortened to CDE, is the part of your business where card data lives, passes through, or can be affected. A useful analogy is a secure room inside your building.

If card data enters that room, anything connected to the room may also matter. The card terminal matters. The checkout page matters. The server that receives the payment details matters. Sometimes the support tool, logging platform, or outsourced admin access matters too.

The smaller the room is, the easier compliance becomes.

A narrow CDE is like a locked cash box in one office.

A sprawling CDE is like leaving invoices, keys, and till drawers scattered across the whole building.

What data are you actually protecting

At a practical level, PCI DSS focuses on protecting payment account data, especially where full card details are present and could be exposed. That's why businesses often aim to avoid storing card data themselves whenever possible.

Layered security helps. If you want a non-PCI-specific explanation of how defences work together, this guide to comprehensive business cybersecurity is a solid companion read. PCI works best when you stop treating each control as a separate chore and start seeing them as overlapping protections.

The cheapest scope reduction usually happens before any audit starts. It happens when a business redesigns the payment flow so fewer systems ever touch card data.

Why scoping comes first

Many businesses begin with the questionnaire. That's backwards. Start by tracing the payment journey:

Entry point: Where does the customer enter card details?

Movement: Which applications, staff, or vendors can see or transmit them?

Storage: Whether anything keeps those details after the transaction.

Administration: Who can change the systems around that process?

Once you can answer those four questions, PCI DSS regulatory compliance becomes more concrete. Until then, every control feels abstract because you don't know what you're securing.

Finding Your Place: The Four Merchant Levels

A retailer can process a modest number of transactions and still have a messy PCI job. Another business can handle far more volume with less pain because its payment flow is cleaner, its vendors are better controlled, and its evidence is easier to collect. That is why merchant level matters, but it does not answer the whole compliance question.

The card brands and acquirers use merchant levels to sort businesses into validation paths based largely on transaction volume. The general thresholds commonly referenced by acquirers. In broad terms, Level 1 covers merchants processing over 6 million card transactions annually, Level 2 covers 1 to 6 million, Level 3 usually covers 20,000 to 1 million e-commerce transactions, and Level 4 sits below that.

PCI DSS Merchant Compliance Levels

| Merchant Level | Annual Transaction Volume | Validation Requirement |

|---|---|---|

| Level 1 | Over 6 million transactions per year | Typically a Report on Compliance, or ROC, with a QSA-led assessment |

| Level 2 | 1 to 6 million transactions per year | Commonly validated through a Self-Assessment Questionnaire, subject to acquirer rules |

| Level 3 | 20,000 to 1 million e-commerce transactions per year | Commonly validated through a Self-Assessment Questionnaire, subject to acquirer rules |

| Level 4 | Under 20,000 e-commerce transactions per year | Commonly validated through a Self-Assessment Questionnaire, subject to acquirer rules |

The easy mistake is to treat this table like a difficulty rating. It is closer to a filing route. Your merchant level helps determine how you prove compliance. It does not shrink the underlying duty to protect cardholder data.

What the levels mean in practice

Level 1 merchants usually face the most formal validation process. A ROC is detailed, evidence-heavy, and usually involves a Qualified Security Assessor. If your systems, logs, access reviews, and vendor records are disorganised, the assessment becomes expensive because your team spends time hunting for proof instead of showing a controlled process.

Levels 2 through 4 often use an SAQ. Owners sometimes hear “self-assessment” and assume it means light work. It often means the opposite for smaller teams. You still need to know which systems are in scope, which service providers touch payment data, and which controls you can demonstrate with screenshots, policies, tickets, scan results, and logs.

That evidence problem is where many SMBs get stuck.

A company may qualify for a shorter SAQ because it uses a hosted payment page, yet still struggles because no one can clearly show who manages the website, how changes are approved, or whether the vendor setup was reviewed properly. If your checkout starts on your own web page, even briefly, controls around secure coding and browser-side payment security matter much more. Good web application security best practices help reduce avoidable PCI headaches later.

Merchant level is only one piece of scope

Three businesses can share the same merchant level and have very different compliance workloads.

A shop using standalone payment terminals may have a narrower cardholder data environment.

An e-commerce brand with a custom checkout usually has more scoping questions.

A business that outsources payment capture but keeps weak oversight of its providers can still create audit pain.

Vendor management often decides whether PCI feels manageable or chaotic. If a gateway, hosting company, shopping cart plugin, fraud tool, or support provider can affect payment security, you need more than a contract and a logo on a diagram. You need to know what they handle, what they attest to, and what evidence you can produce when your acquirer asks.

Security testing fits into that picture, too. If your payment flow depends on a web application, periodic affordable web app security testing can help confirm that the controls you documented match the risks in the actual environment.

Don't guess based on the label

Merchant level does not tell you which SAQ applies. It does not tell you whether your website is in scope. It does not tell you whether a service provider has shifted responsibility back onto your team through a gap in configuration or oversight.

A better approach is to pair the level question with three operational questions:

How do customers submit payment data?

A terminal, hosted page, embedded iframe, call centre workflow, and custom checkout all create different scope boundaries.

Which third parties can affect payment security?

Include payment processors, web hosts, ecommerce platforms, plugins, MSPs, and support vendors.

What evidence can you show today?

Policies alone are not enough if no one can produce access reviews, scan reports, inventories, or change records.

A lower merchant level usually means a lighter validation route. It does not mean lighter responsibility.

For SMBs and mid-market companies, that is the practical lesson. Start with your likely level, but spend equal time on scoping, vendor accountability, and evidence collection. Those are usually the main obstacles.

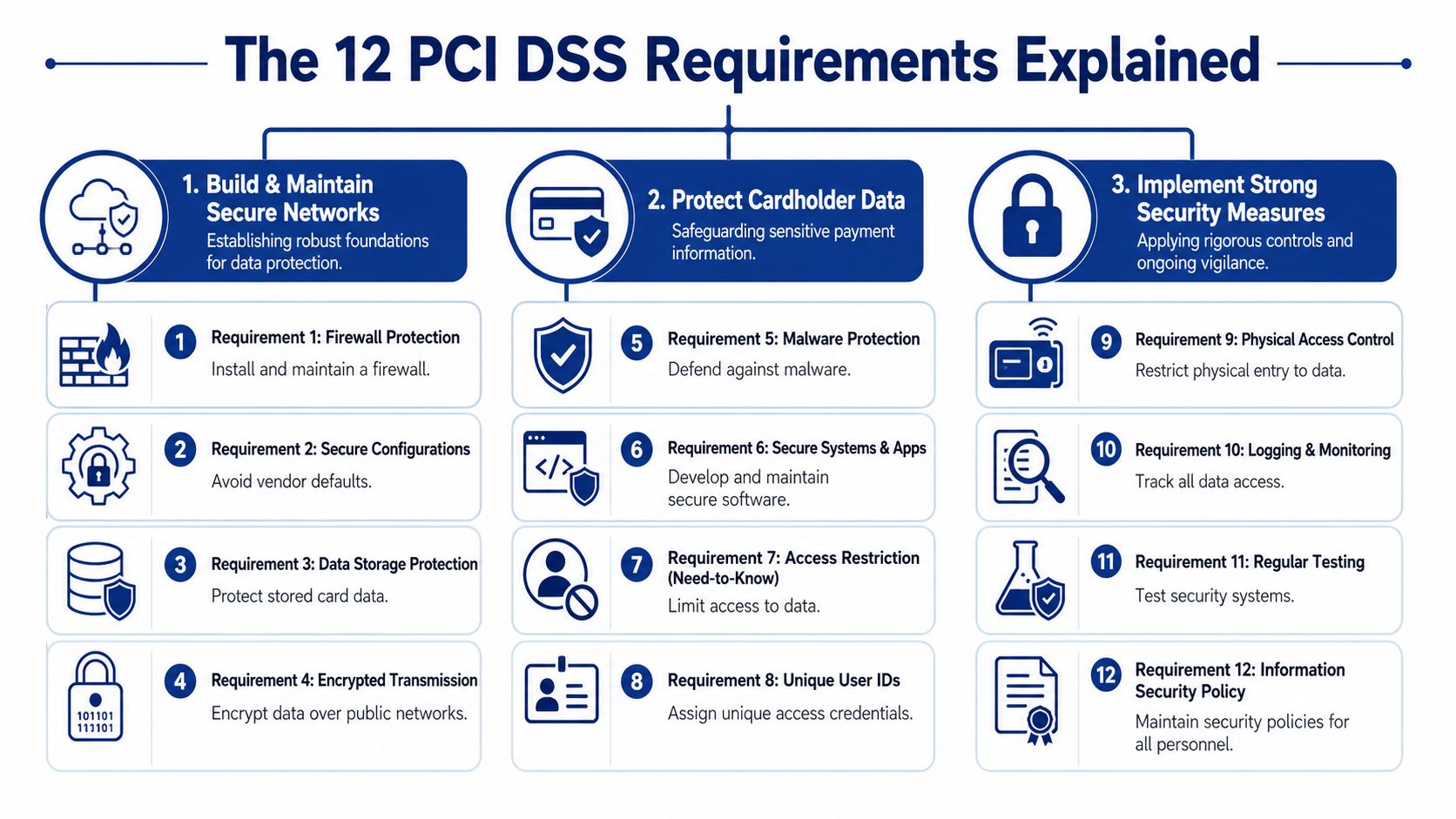

The 12 PCI DSS Requirements Explained

The 12 requirements can look like a wall of jargon. They make more sense when you group them by purpose. Think of PCI DSS as a security programme with three jobs: build safe foundations, protect the data itself, and keep watch over the whole environment.

Build and maintain secure networks

These controls are about basic discipline. You don't want payment systems sitting in a wide-open environment with factory settings still in place.

Install and maintain network security controls so traffic to sensitive systems is limited and inspected.

Apply secure configurations so devices and systems don't rely on default settings that attackers already know.

Protect stored account data so retained card information isn't left readable or casually accessible.

Protect cardholder data in transit so payment details aren't exposed while moving across public networks.

A good analogy is a shopfront. Requirement 1 locks the doors. Requirement 2 changes the default alarm code. Requirements 3 and 4 protect the cash once it's inside and while it's being transported.

Protect cardholder data through secure systems and access

The next group is about reducing exposure from malware, weak development practices, and excessive access.

Protect systems from malicious software so common forms of compromise don't gain an easy foothold.

Develop and maintain secure systems and applications so software changes don't introduce avoidable weaknesses.

Restrict access by business need-to-know, so only the right people can reach card-related systems or data.

Identify users and authenticate access so actions can be tied to specific individuals instead of shared accounts.

Restrict physical access so someone can't walk up to a device, terminal, or stored media and tamper with it.

If your payment flow depends on a custom portal or web application, application-layer testing becomes part of the conversation. This overview of affordable web app security testing helps explain why businesses often test customer-facing software separately from general infrastructure. For a broader technical checklist, these web application security best practices are also relevant when payment features live inside custom software.

Keep watching and keep proving

The last requirements are where compliance stops being a setup task and becomes an operating habit.

Log and monitor access so unusual activity leaves a trail that investigators can follow.

Test security systems regularly so controls are verified instead of assumed.

Maintain an information security policy so staff know the rules, responsibilities, and response process.

Security controls you can't demonstrate usually don't count for much during an assessment. PCI is as much about evidence as intent.

Why the list feels harder than it looks

Each requirement sounds sensible on its own. The difficulty appears when they overlap. Logging depends on access design. Secure development affects data protection. Vendor tools can affect segmentation. A policy only works if staff procedures match it.

That's why PCI DSS regulatory compliance shouldn't be treated like a memorisation exercise. The 12 requirements are a framework for running payment handling in a controlled, provable way.

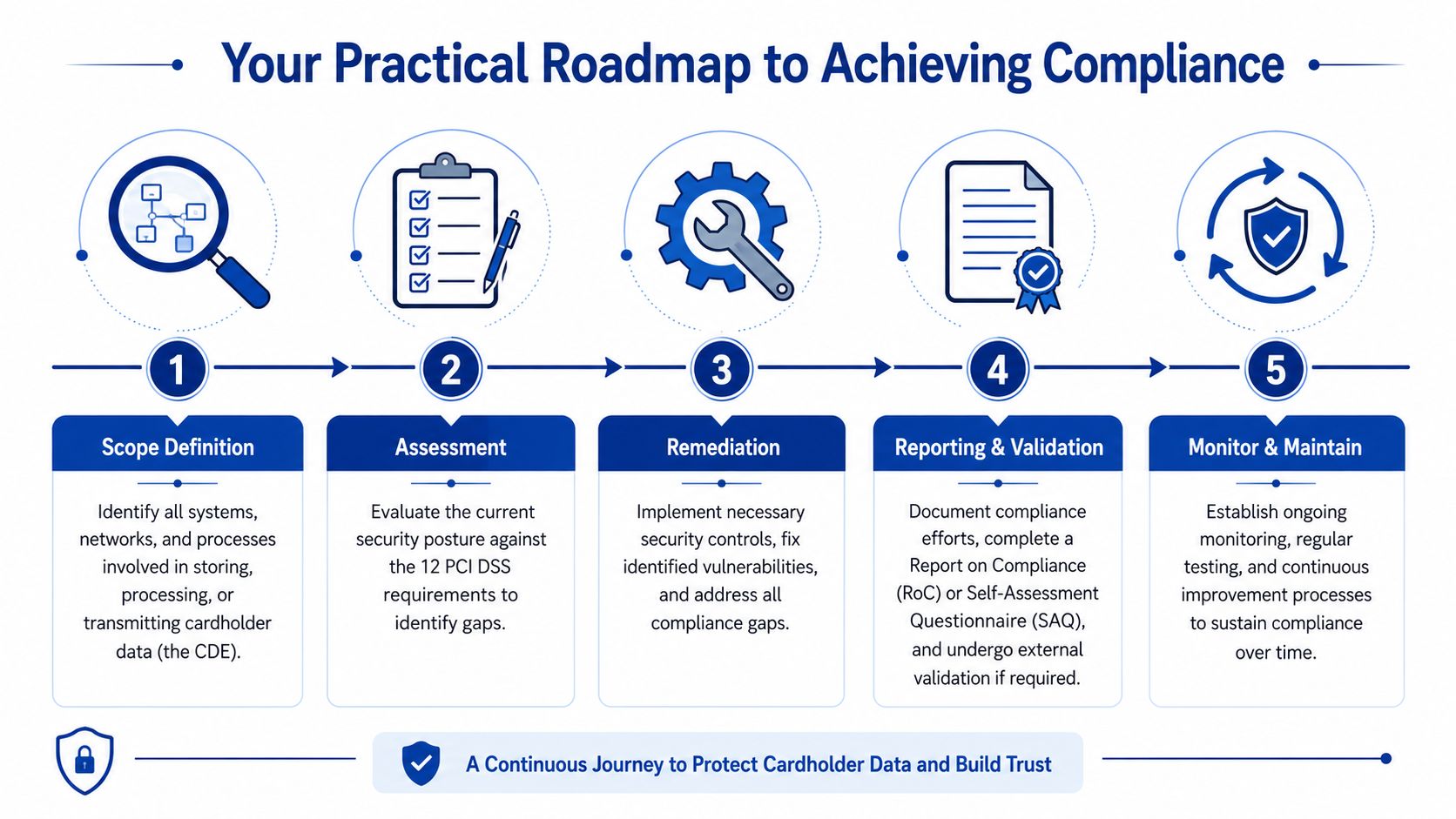

Your Practical Roadmap to Achieving Compliance

Most organisations need a project path, not another definition. PCI work tends to move more smoothly when you treat it as a cycle with a clear sequence: define, assess, fix, validate, maintain.

Stage 1 and Stage 2

Scope definition comes first because everything else depends on it. Identify every system, process, person, and vendor involved in storing, processing, or transmitting card data, and anything that can affect that environment. If your map is wrong, your assessment will be wrong too.

Assessment comes next. Compare your current controls against the relevant PCI expectations and note where practice, policy, and evidence don't line up. During this stage, many firms discover they have a tool in place but no proof that it is configured, reviewed, or maintained consistently.

Stage 3 and Stage 4

Remediation means fixing what the assessment uncovered. That may include tightening access, reducing stored data, removing risky workflows, hardening systems, or redesigning how payments are handled.

Reporting and validation are where your work becomes formal. Depending on your validation route, that may involve an SAQ or a ROC-style process. Either way, the documents only go smoothly when the evidence has been organised in advance.

A practical way to lower complexity is to design payment flows so fewer internal systems touch card data. Teams building or replacing payment functionality often review architecture choices alongside this guide to payment gateway software development, because integration decisions can change scope before any paperwork starts.

Stage 5

Monitor and maintain is the stage most often neglected. Businesses pass a questionnaire, file the documents, and mentally close the project. Then a new plugin is installed, a vendor changes process, admin access expands, or a support shortcut bypasses the intended controls.

That's why PCI DSS regulatory compliance is ongoing. You maintain it by keeping the environment stable, documented, and reviewable.

A workable operating rhythm

This doesn't need to become bureaucratic. It needs to become repeatable.

Review changes: Check whether new apps, vendors, or workflows affect payment scope.

Collect evidence as you go: Save approvals, configurations, access reviews, and vendor documents during normal operations.

Reconfirm ownership: Make sure someone owns the merchant relationship, someone owns technical controls, and someone coordinates evidence.

Treat payment design as a compliance control: Architecture decisions can remove risk before monitoring tools ever come into play.

The smoothest PCI projects don't start with an auditor. They start with an accurate system map and disciplined evidence handling.

Common Pitfalls and Industry-Specific Challenges

Most PCI content spends its energy on internal controls. That's useful, but incomplete. For many small and mid-sized organisations, a critical failure point is somewhere else: vendor and SaaS scope ambiguity.

A major gap in typical guidance is that it rarely answers the question businesses want to know: which third parties bring the environment into scope, and how to prove they are compliant. The harder burden for many SMBs and mid-market firms is scoping and collecting evidence from vendors, as noted in this analysis of PCI DSS vendor scope ambiguity.

The most common pitfall is false scope reduction

A business uses a payment processor and assumes that means PCI is “handled”. Sometimes the processor does reduce the scope significantly. Sometimes it doesn't. The difference depends on your integration model and who controls adjacent systems.

Examples of third parties that can affect the scope include:

Hosted checkout providers: These may reduce exposure if card entry is fully outsourced.

Custom website or app vendors: They can affect the payment flow even if they never view a full card number.

Managed IT providers: Admin access to systems around the CDE can matter.

Cloud and SaaS platforms: Logs, storage, support access, or embedded scripts can create additional questions.

What evidence from vendors usually matters

If a third-party service provider stores, processes, or transmits cardholder data, it must comply and provide proof, such as an Attestation of Compliance, often called an AOC. That single document won't solve everything, but it is often a core piece of evidence.

Owners should ask practical questions, not vague ones.

Which service are you providing?

Get a precise description of what the vendor touches.

What is your PCI responsibility?

Ask which parts of the control set they cover and which remain with you.

What proof can you provide?

Request current compliance artefacts, including the AOC where relevant.

What changes require notice?

Contract terms should support visibility when their environment changes.

A vendor can reduce your workload, but it can't inherit your accountability.

Industry-specific friction points

Healthcare organisations often face a split-brain problem. Clinical systems, billing systems, and patient-facing payment journeys may sit under different teams. Even when payment data and health data are treated separately, staff workflows can blur the boundaries.

Insurance businesses often run complex payment flows across broker portals, policy systems, call centres, and renewal processes. The challenge isn't just technical security. It's proving who owns each step in the transaction path.

Small businesses usually struggle with staffing and documentation. They may have decent practical security, but weak evidence. In PCI, undocumented control is often indistinguishable from absent control.

The contrarian lesson

The hard part of PCI DSS regulatory compliance usually isn't remembering the 12 requirements. It's governance across the payment ecosystem. If you can inventory vendors, define the scope carefully, and gather the right evidence before someone asks for it, the standard becomes far less intimidating.

How a Development Partner Supports Your Compliance Journey

A development partner doesn't certify your business as compliant. That responsibility stays with the merchant or service provider. What a technical partner can do is reduce avoidable complexity before it turns into audit pain.

Where a software team helps most

A strong development team can support PCI work in practical ways:

Payment flow design: They can build integrations that minimise direct handling of card data.

Secure application development: They can implement access controls, logging hooks, and safer coding patterns from the start.

Scope reduction: They can separate payment functions from the rest of the application so the CDE stays smaller.

Evidence support: They can produce architecture notes, data flow diagrams, and implementation details that compliance teams often need later.

This matters most when the payment experience is custom. A home-grown checkout, policy portal, patient billing system, booking flow, or mobile app can inadvertently expand the CDE if nobody designs for scope.

For businesses building regulated systems, compliance-driven software development is the right mindset. Security controls shouldn't be added after launch like trim on a finished building. They belong in the blueprint.

A firm such as Cleffex Digital Ltd can fit into that process as a software development partner by building payment-enabled applications, integrating gateways in ways that can reduce direct card-data exposure, and implementing technical controls inside custom platforms. That's especially relevant for healthcare, insurance, SaaS, and mid-market businesses that need customised software rather than a generic checkout plugin.

The key is choosing a partner who understands that compliance isn't only about features. It's about architecture, traceability, and disciplined change control.

If your business is planning a payment-enabled website, app, portal, or platform, Cleffex Digital Ltd can help you build with security and compliance considerations in mind from the start. That approach can make PCI DSS regulatory compliance more manageable by reducing scope, clarifying data flows, and embedding the technical controls your team will need to maintain over time.