You start taking more card payments. Maybe your clinic begins collecting balances online. Maybe your insurance office adds recurring billing. Maybe your retail shop launches ecommerce on top of in-person sales. Revenue goes up, but so does the number of places payment data might pass through.

That's usually the moment PCI DSS stops sounding like abstract compliance jargon and starts feeling uncomfortably real.

Most small and mid-sized businesses don't get into trouble because they set out to be careless. They get there because payment handling grows faster than their controls do. A receptionist keys in cards over the phone. A web developer adds a checkout plugin. A finance team keeps card details longer than necessary because it feels convenient. Suddenly, the business has created a small cardholder data environment without naming it.

If you need a plain-language refresher on what a data breach is, it helps to frame PCI DSS correctly. This isn't only about passing an assessment. It's about reducing the chance that a payment workflow turns into a security incident, a customer trust problem, or a difficult call with your processor.

For Canadian SMBs, healthcare groups, and insurance teams, PCI DSS compliance is rarely a side issue. It sits inside everyday operations: who can access payment records, how card data moves through your website, what logs your team reviews, and whether your software stack stores something it shouldn't. The businesses that handle this well treat PCI as part of how they run, not as paperwork they scramble to finish once a year.

Why PCI DSS Compliance Suddenly Matters to Your Business

A common story goes like this. A business has been processing payments for years through a trusted provider and assumes the hard part is covered. Then the bank asks for compliance documents, the website gets redesigned, or someone realises staff are taking card details in a way nobody has documented.

That's when PCI DSS compliance becomes urgent.

Growth changes your risk faster than you expect

A dental clinic may start with a terminal at the front desk. Later, it adds invoices by email, payment links, and phone payments. An insurance brokerage may use a billing platform that integrates with a CRM and accounting software. A small retailer may sell in-store, on Shopify, and through occasional manual orders. Each new channel can expand the places where payment data is stored, processed, or transmitted.

The issue isn't just volume. It's sprawl.

Once payment handling spreads across browsers, inboxes, booking tools, point-of-sale systems, support workflows, and vendor integrations, it becomes much harder to answer basic questions. Where does card data go? Who can see it? What systems touch it? What evidence do you have that controls are working?

Practical rule: If your staff can't draw the path a card number takes through your business, your PCI scope is probably larger than you think.

Trust is the real business driver

Clients don't separate payment security from your brand. If a patient pays a clinic or a customer buys from your online store, they assume the business handles card data competently. They won't care whether the gap came from your plugin, your staff process, or your hosting arrangement.

That's why PCI DSS matters even when you're small. Acquiring banks and payment brands still expect a defensible control model. And in practical terms, businesses that ignore it can face penalties, higher fees, or loss of processing privileges according to the PCI Security Standards Council standards overview.

For many Canadian businesses, the shift is mental before it's technical. PCI isn't a punishment for growth. It's the operating discipline that lets you keep growing without turning payments into your weakest point.

Understanding the Fundamentals of PCI DSS

A clinic in Ontario adds online bill payment, keeps taking cards at the front desk, and still processes a few payments by phone. Nothing about that setup feels unusual. Then the first PCI questionnaire arrives, and the core problem shows up. The business is no longer asking, “Do we take cards?” It is asking, “Which systems, people, and vendors now touch card data, and who is checking them every month?”

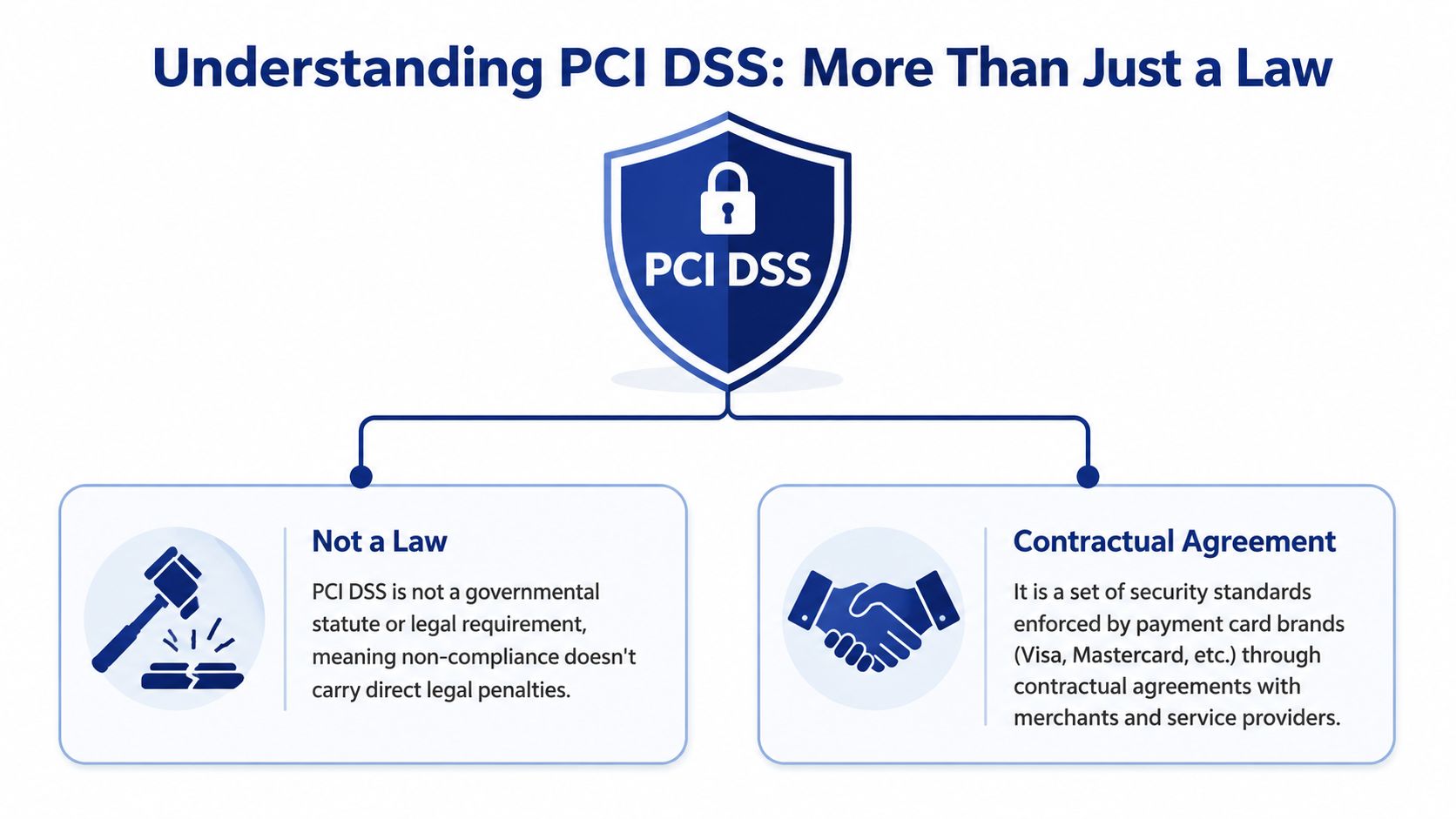

PCI DSS gives structure to that answer. It works like a building code for payment security. The standard sets the baseline for organisations that process, store, or transmit payment card data, and those requirements cover areas such as network security, access control, monitoring, testing, and policy governance.

Who sets the rules and who enforces them

The ecosystem breaks down like this:

The PCI Security Standards Council maintains the standard.

Card brands and acquiring banks push those requirements into merchant agreements and validation expectations.

Merchants and service providers must show they meet the controls that apply to their environment.

Assessors and Approved Scanning Vendors may test or validate parts of that work.

For clients, I usually frame PCI as a payment-industry obligation carried through contracts, processor requirements, and validation rules. That distinction matters. A small healthcare clinic or insurance broker may assume a gateway provider “handles PCI,” then discover their own staff workflows, connected systems, and evidence requirements still sit squarely on their side.

If you work in online selling, this broader context around ecommerce payment security is useful because a hosted gateway reduces risk, but it does not automatically remove your responsibilities.

The Cardholder Data Environment is your real scope

The Cardholder Data Environment, or CDE, is the part that drives effort and cost. It includes the systems and processes that store, process, or transmit cardholder data, plus any connected systems that can affect the security of that environment.

In practice, the scope expands faster than teams expect.

A receptionist's workstation can be in scope if the staff key card details into a portal. A call recording platform becomes a problem if patients or customers read card numbers aloud. A web server may be in scope if the payment form is hosted there or if the site can influence how payment data is captured. An IT support jump box can matter too if administrators use it to reach payment systems.

That is why scope reduction is usually the best first move. Hosted payment pages, tokenisation, network segmentation, and cleaner vendor integrations can shrink what you need to secure and what you need to prove. For smaller organisations that want stronger security habits across the business, this guide to cybersecurity for small businesses gives useful background.

Validation happens annually. Operations happen all year.

Many SMBs get tripped up here. They treat PCI like a tax filing. Fill out the SAQ, submit the paperwork, and move on.

The work is recurring. Vulnerability scans come back on schedule whether, your team is ready or not. Logs still need review. User access still needs to be checked when staff change roles. Evidence still needs to be collected when your processor or assessor asks how you know a control is working. For Canadian businesses with multiple locations, bilingual support teams, remote staff, or a mix of in-person and online payments, that operational burden is often the hidden cost.

A simple summary of common validation paths is below.

| Level | Annual Transaction Volume (All Channels) | Validation Requirements |

|---|---|---|

| Level 1 | Varies by card brand and acquiring bank rules | Typically a ROC or equivalent assessor-driven validation path |

| Level 2 | Varies by card brand and acquiring bank rules | Often SAQ-based or assessor-guided validation, depending on environment |

| Level 3 | Varies by card brand and acquiring bank rules | Commonly SAQ-based with required supporting evidence |

| Level 4 | Varies by card brand and acquiring bank rules | Usually SAQ-based, often with scans if applicable |

Keep the table at a planning level only. Your acquiring bank and processor decide the exact validation route, and those expectations can differ based on how you accept payments. Confirm your level early, then map the recurring tasks behind it. That is how PCI becomes manageable. It stops being a yearly scramble and becomes part of normal operations.

The 12 PCI DSS Requirements Explained

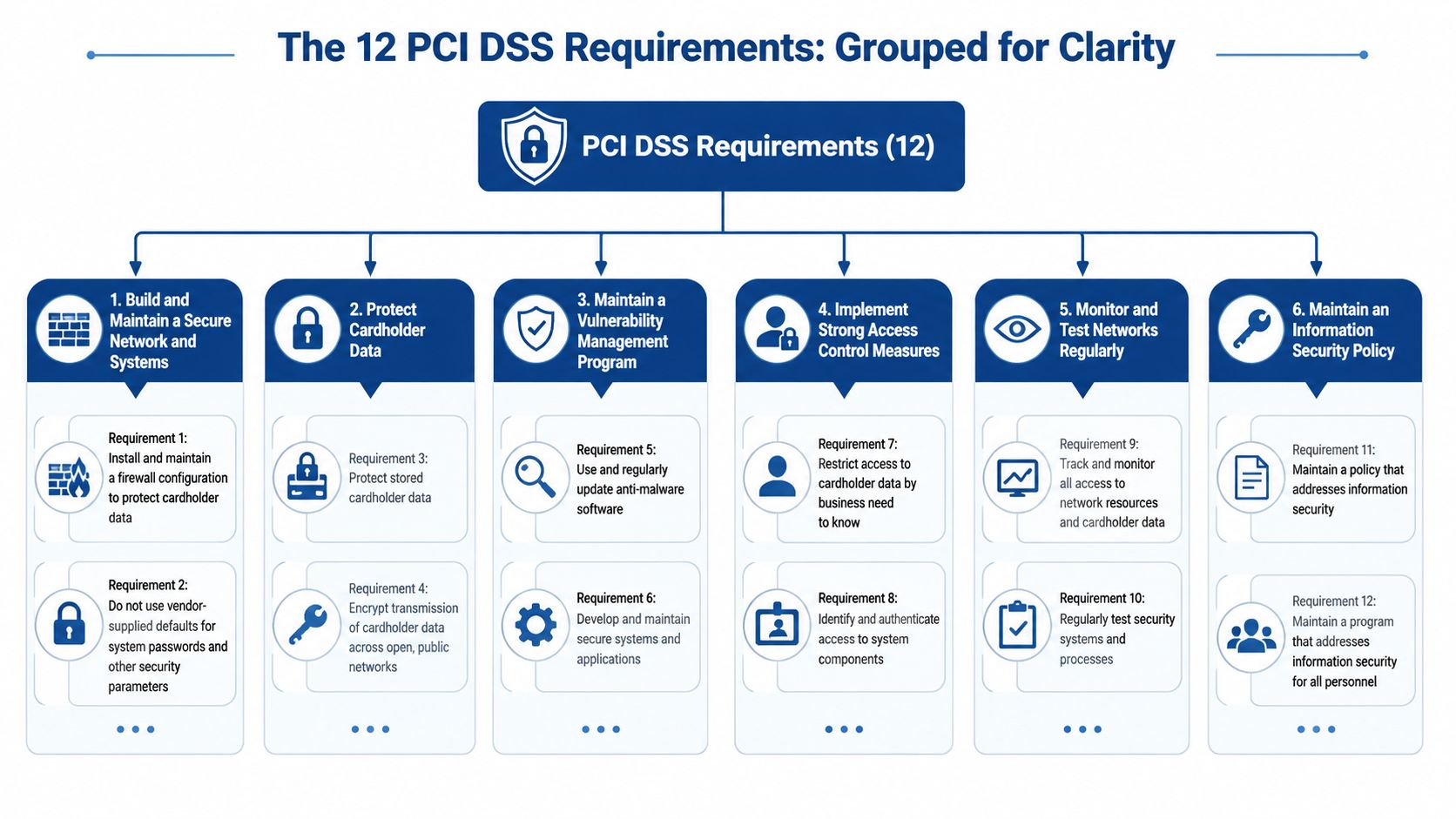

The fastest way to make the standard less intimidating is to stop reading it as a flat list. The 12 requirements make more sense when grouped by security goal.

PCI DSS imposes technical controls across the cardholder data environment, including network security, secure configurations, encryption, logging, and recurring testing. Requirement 4 covers strong cryptography for cardholder data in transit over open or public networks, and Requirement 10 covers time-stamped logging and daily review of access to network resources and cardholder data, as outlined in this breakdown of the 12 PCI DSS requirements.

Build and maintain a secure network and systems

The first group is about the perimeter and the default state of your systems. In plain language, PCI expects you to control traffic and remove weak default settings.

If your payment environment is like a clinic building, the firewall is the controlled entrance and vendor defaults are the keys left under the mat. A business that leaves default credentials in place or exposes systems more broadly than necessary makes every later control less effective.

For smaller teams, baseline network hygiene matters more than fancy tooling. Even practical references like Clouddle's security recommendations are useful here because they reinforce the same operational idea: lock down what doesn't need to talk, limit access paths, and start secure rather than trying to patch around exposure later.

Protect cardholder data

This is typically the first part considered, but the emphasis is often exclusively on storage. PCI cares about both stored data and data in transit.

If card data must travel across a public network, strong cryptography protects it in motion. If card data is stored, you need to protect it properly and question why it's being retained in the first place. Encryption is the equivalent of placing the contents in a sealed container that outsiders can't read, even if they intercept it.

A practical lesson here is that convenience drives bad storage habits. Teams keep card details because recurring billing seems easier, or because they want a fallback for collections. That decision creates downstream obligations in access control, logging, retention, testing, and incident handling.

Stored card data is rarely just a storage problem. It creates a larger operating burden around every surrounding system and process.

Maintain a vulnerability management programme

This goal is about keeping malicious software and known weaknesses from becoming your everyday reality. It includes maintaining secure systems, applying patches, and running security controls that match the environment.

What works is routine. What fails is heroic cleanup after months of drift.

If your payment application sits on a server nobody has reviewed recently, or your ecommerce plugins update only when something breaks, you're already in dangerous territory. PCI pushes teams toward disciplined maintenance because attackers usually exploit neglected basics, not movie-style hacking.

Implement strong access control measures

This goal asks a simple question. Who can get to the card data and why?

Good PCI practice means limiting access by job role, assigning accountability, and avoiding shared access patterns that make activity impossible to trace. In a healthcare setting, this gets especially important when front-desk, finance, and support functions overlap. People may all be trusted, but they should not all have the same level of access.

The cleanest environments usually follow one rule. If someone doesn't need access to payment data to do their job today, they shouldn't have it.

Regularly monitor and test networks

PCI transitions from being a document to an operating model. Logs need timestamps. Access activity must be reviewed. Testing has to happen on a recurring basis.

For many SMBs, this is the hidden work. Buying a payment tool is easy. Building daily review habits, central log collection, and recurring validation workflows is harder. The standard is pushing you to create evidence, not just intention.

Maintain an information security policy

The final goal keeps everything from becoming tribal knowledge. Policies, risk review, and assigned responsibility turn one person's memory into something the business can repeat.

A strong policy doesn't need to be bloated. It needs to reflect the actual environment. If your written process says card data is never written down, but staff still jot it on paper during phone calls, the paper process is the truth and the policy is fiction.

Your Step-by-Step Compliance Journey

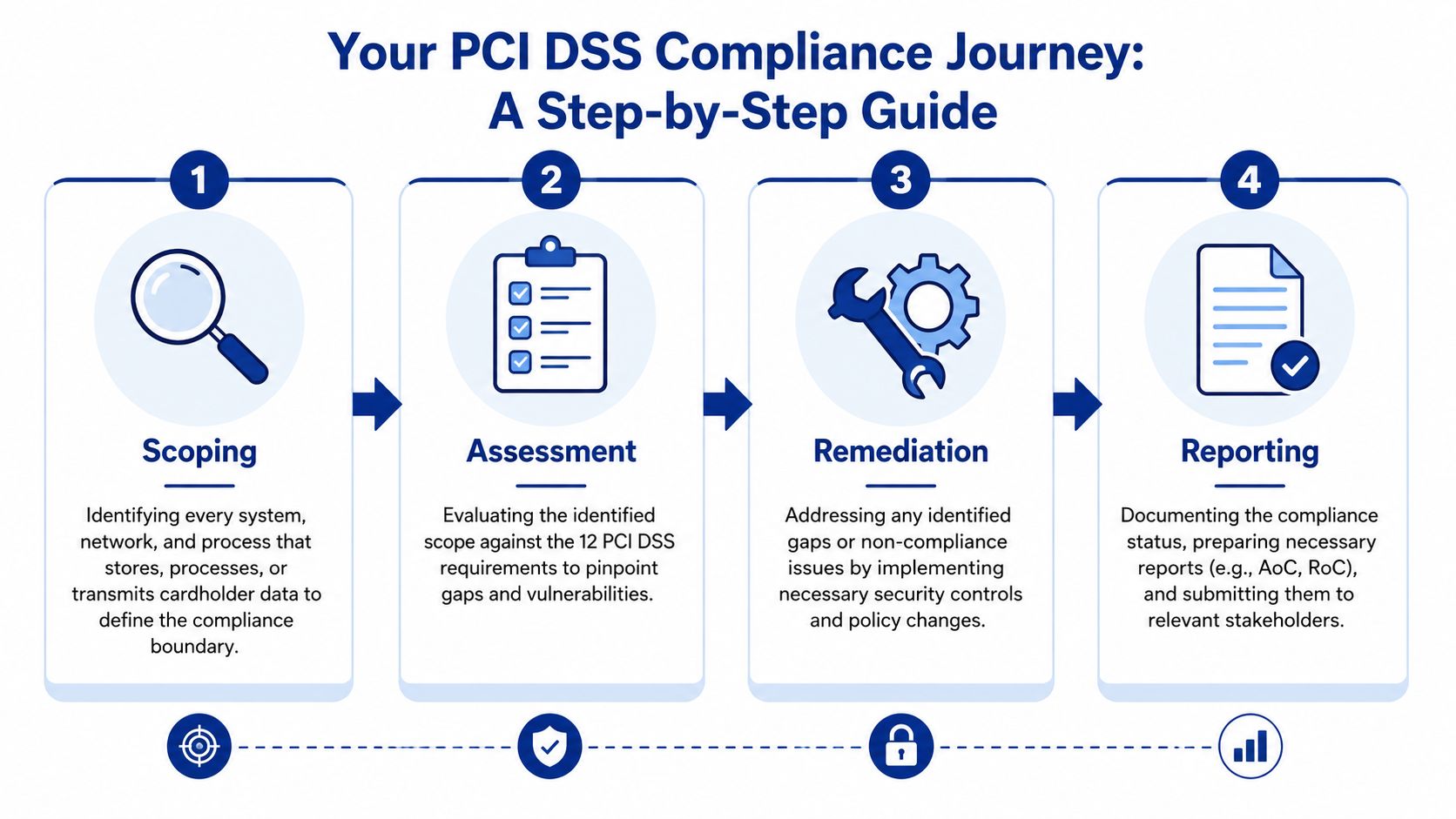

Most first PCI projects go badly for one reason. The business starts with forms instead of scope.

The right sequence is simpler. First, find where payment data touches your business. Then assess what those systems require. Then fix the gaps. Then report accurately.

Step one is scoping

Start by mapping every way card data enters, moves through, or leaves your environment. Website checkout, payment links, virtual terminals, call centre processes, POS devices, invoices, support workflows, integrations, and third-party vendors all belong on the map.

A simple data flow diagram is enough at first. Boxes and arrows beat assumptions.

Ask practical questions:

Where is payment data entered?

Browser, terminal, phone, mobile app, or back-office tool.

What systems touch it?

Website, CRM, payment gateway, accounting system, support desk, call recording platform.

Who handles it?

Front desk, finance, sales, developers, outsourced support.

What gets stored?

Full card data, tokens, transaction references, recordings, screenshots, and emailed details.

Scoping is where many businesses realise they've expanded the CDE accidentally.

Step two is choosing the right validation path

Once the scope is clear, determine whether you'll complete a Self-Assessment Questionnaire or need a Report on Compliance. For many SMBs, the practical issue is not memorising acronyms. It's choosing the path that matches how payments are implemented.

If your website redirects customers to a hosted payment page, your assessment path may be much simpler than if your server directly handles card details. That's why architecture decisions matter before compliance documentation begins.

The easiest PCI project is usually the one where engineering reduced the scope months earlier.

Step three is remediation

To achieve compliance, you fix weak controls, tighten access, remove unnecessary storage, clean up payment workflows, patch systems, improve logging, and document operating procedures.

Remediation often includes changes like:

Reducing exposure by replacing direct card handling with hosted forms or tokenisation.

Cleaning permissions so only the right staff can reach payment tools or records.

Improving evidence through centralised logs, review procedures, and retained documentation.

Closing technical gaps, such as insecure configurations or outdated software tied to payment systems.

Don't treat remediation as a one-off punch list. If the fix depends on one employee remembering to do something manually forever, it's fragile. Prefer controls built into the system or formalised into operations.

Step four is reporting and attestation

After assessment and remediation, you complete the required documentation, which may include an Attestation of Compliance and other supporting materials requested by your bank, processor, or assessor.

Good reporting is honest and specific. Don't overstate controls. Don't copy policy language that doesn't match your environment. If you've scoped narrowly because you use a hosted payment architecture, say so clearly and support it with diagrams and vendor documentation.

Teams that succeed usually keep a small evidence folder all year rather than trying to reconstruct everything later. Policies, scan reports, access reviews, vendor confirmations, diagrams, and change records are much easier to manage when collected continuously.

Best Practices for Scope Reduction and Ongoing Maintenance

A small clinic adds online billing, keeps phone payments for convenience, and assumes the PCI work is mostly paperwork. Six months later, staff are storing card details in appointment notes, the website has changed twice, and nobody is sure who reviews scan results. That is how scope grows subtly, and how PCI turns into a recurring operational burden instead of a controlled process.

The cheapest card environment is the one you do not have to secure in the first place.

For Canadian SMBs, healthcare practices, and insurance firms, scope reduction starts with a business choice. Decide whether your team will ever handle raw card data directly. If the answer is yes, expect more systems, more evidence, more recurring reviews, and more chances for card data to end up somewhere it should not. If the answer is no, design your payment flow so card entry happens in a provider-controlled page, iframe, or tokenised workflow.

A clinic analogy helps here. If lab samples never enter the front desk area, the front desk needs fewer controls, less training, and less cleanup. Payment architecture works the same way. The fewer places card data can enter, pass through, or be stored, the smaller your cardholder data environment becomes.

Scope reduction usually comes from a few practical changes:

Hosted payment pages so your server does not receive card details.

Tokenisation so billing, refunds, and recurring charges use replacement values instead of card numbers.

Network segmentation so payment-connected systems are separated from general business systems.

Process changes that stop staff from taking cards through email, chat, paper forms, or ticketing tools.

These decisions often get tangled up with platform and integration work. A business can choose a low-scope checkout, then pull payment data into other systems through custom apps, plugins, or admin workflows and expand scope again. This guide to ecommerce integrations in Canada is useful context because integration design often creates PCI exposure long after the checkout is launched.

Ongoing maintenance is where PCI gets expensive.

The hidden cost is not just the assessment. It is the repeated work needed to keep controls operating. Quarterly scans need owners. Failed findings need follow-up. Logs need review. Access needs to be checked when staff join, leave, or change roles. Significant changes to websites, networks, or payment workflows can trigger more testing and documentation. For a small business, those tasks usually fall on people who already have other jobs.

Set a simple operating rhythm and assign names to it, not just departments:

Quarterly vulnerability scans with a process for fixing and rescanning failed items.

Log review routines for the systems that remain in scope.

Access reviews tied to onboarding, offboarding, and role changes.

Annual testing and policy review scheduled before your renewal window, not during it.

Change review checkpoints for new plugins, vendor changes, web updates, and network changes that could affect payment flow or scope.

Good PCI maintenance is boring on purpose. That is a strength. A stable monthly and quarterly routine catches drift early, before an assessor, bank, or incident does. In practice, the businesses that handle PCI well are not the ones with the thickest policy binder. They are the ones that can show who reviews what, how often it happens, and where the evidence is stored.

Common Pitfalls and Industry-Specific Considerations

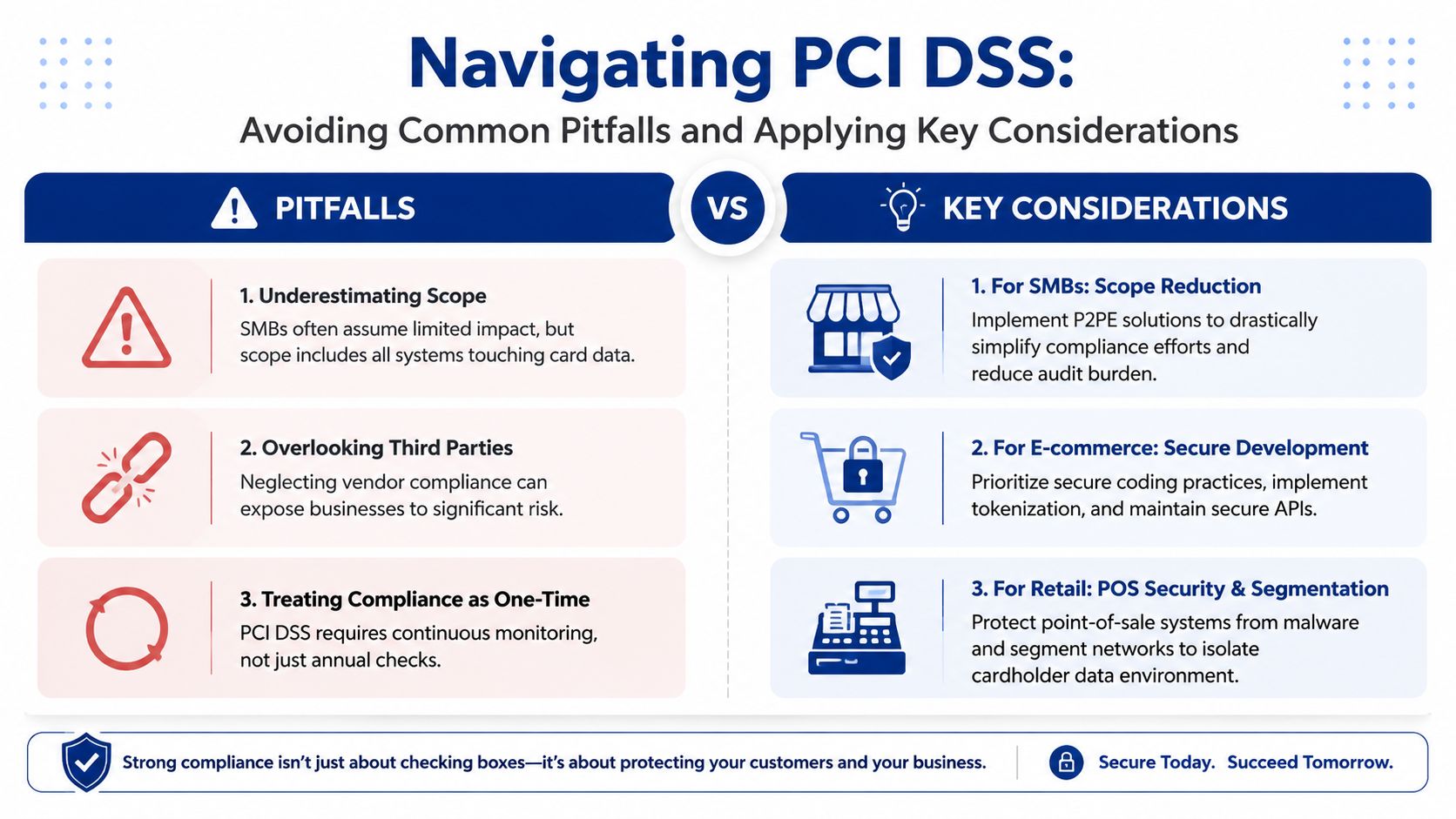

The most expensive PCI mistake isn't technical. It's assuming someone else has already handled it.

That assumption shows up in different forms. A retailer thinks Shopify makes the entire store compliant automatically. A clinic assumes its practice management vendor covers every payment-related control. A SaaS company believes its cloud provider owns security end-to-end. In each case, the business confuses a helpful platform with full responsibility transfer.

SMBs often underestimate scope

Small businesses tend to look at PCI through the lens of transaction volume. That's understandable, but it misses the operational reality. A low-volume merchant can still create a messy cardholder environment if staff take payments over the phone, store screenshots, or use email to collect card details.

The hidden burden is ongoing work. Current guidance highlights daily log review, quarterly vulnerability scans, annual penetration testing, and yearly policy and risk review, which means PCI becomes a standing security operations function rather than a yearly paperwork exercise, as discussed in this article on continuous PCI DSS compliance requirements.

What usually fails is the set-it-and-forget-it model. The processor may be compliant. Your merchant account may be active. But if your internal processes create scope, you still own that scope.

Healthcare and insurance teams face overlap risk

Healthcare and insurance environments often combine payment activity with more sensitive workflows. Front-desk staff, billing teams, patient portals, policy systems, and customer service tools may all sit close together. That doesn't mean PCI and privacy obligations are the same, but it does mean poor system design can make both harder.

A common problem is using shared systems for too many functions. If a workstation accesses patient data, insurer records, and card-processing tools with weak separation, every access issue becomes harder to contain and audit. The safest route is to keep payment workflows clean, limited, and documented.

If one system handles both sensitive business data and payment activity, design discipline matters twice as much.

SaaS and outsourced IT teams misread shared responsibility

Cloud platforms and managed vendors can reduce workload, but they don't erase merchant responsibility. Someone still has to verify who handles what, who produces evidence, and what remains in scope.

Contracts, architecture diagrams, and vendor attestations are critical elements. If your application passes payment data to a processor through an API, the implementation details affect your responsibility. If your support team can access payment-related admin tools, that access still needs control and review.

For teams building or integrating payment systems, this broader guide to payment gateway software development is useful because PCI problems often start in design decisions long before assessment time.

The process mistakes that repeat

Some pitfalls show up across almost every industry:

Treating the SAQ as the project instead of the final paperwork.

Keeping card data “just in case” without a retention justification.

Ignoring call recordings and support tools that may capture payment details.

Letting developers or admins share accounts in payment-related systems.

Failing to re-scope after changes to websites, vendors, networks, or billing workflows.

The businesses that handle PCI well are rarely the most complex. They're the most honest about how payments move through the business.

Your PCI DSS Compliance Checklist and Next Steps

If you're starting your first PCI DSS project, don't aim for elegance on day one. Aim for a clear picture of reality.

Use this checklist as your starting point:

Map payment flows across web, phone, in-person, billing, and support channels.

List every system and vendor that stores, processes, transmits, or can influence payment data.

Confirm your merchant validation path with your acquiring bank or processor.

Identify unnecessary storage and remove it where possible.

Review website and app architecture to see whether hosted payment pages or tokenisation could reduce scope.

Check access rights for staff, admins, and third parties involved in payment workflows.

Set up evidence collection for policies, scan results, change records, access reviews, and vendor documentation.

Schedule recurring work so reviews, scans, testing, and updates happen as operations, not as panic.

Document real processes rather than idealised versions of how payments should work.

Reassess after significant changes to checkout, integrations, network design, or billing tools.

Keep a short resource list close at hand. The official PCI Security Standards Council materials should be your baseline for the standard itself, SAQ options, and validation documents. If your environment is complex, involve a qualified assessor early, especially before redesigning payment flows or finalising scope assumptions.

PCI DSS compliance can feel heavy the first time through. It gets much more manageable when you treat it as a discipline of reducing scope, tightening operations, and collecting evidence as you go. That approach protects the business, makes bank conversations easier, and shows customers you handle payments with the care they expect.

If your team needs help designing secure payment workflows, reducing PCI scope, or building software that supports compliance from the start, Cleffex Digital Ltd can help you plan and deliver practical solutions for Canadian businesses in healthcare, insurance, retail, and beyond.