In 2024, the global ecommerce payments market reached $8.3 trillion, and it is projected to reach $13 trillion by 2030, a 57% increase over six years, according to Juniper Research's ecommerce payments market report. That number changes how business owners should think about payments.

Payments aren't just the final box to tick at checkout. They shape whether a customer trusts your store, whether a transaction gets approved, how much operational overhead your team carries, and how easily you can expand into new markets. A weak stack creates friction. A strong one quietly removes reasons for customers to leave.

Most advice on ecommerce payment solutions stops at provider lists. That's rarely enough. A startup launching fast, an established Canadian retailer selling cross-border, and an enterprise managing multiple channels should not choose the same payment setup for the same reasons.

Why Your Ecommerce Payment Solution Defines Your Success

Many merchants still treat payments like plumbing. That's expensive thinking.

If your checkout is clunky, customers hesitate. If your fraud rules are too strict, good orders get blocked. If your provider doesn't support the right wallets or regional methods, customers drop off before they even reach the final click. The payment layer influences revenue, trust, support workload, and how quickly you can launch new products or geographies.

Payments affect more than approval rates

A payment system sits at the intersection of four business concerns:

Revenue capture: Fewer failed transactions and fewer abandoned carts mean more completed orders.

Customer experience: Fast checkout matters, especially on mobile and repeat purchases.

Risk management: Security design affects fraud exposure, chargeback handling, and compliance efforts.

Growth readiness: Cross-border support, multi-currency handling, subscriptions, and new payment methods all depend on the stack you choose.

That's why payment architecture should be discussed alongside pricing, fulfilment, and marketing. It's part of your growth model.

Practical rule: If a payment decision changes conversion, compliance burden, and expansion options, it's not a back-office detail. It's a strategy.

The hidden cost of choosing convenience alone

The easiest option isn't always the right one. An all-in-one platform can get you live quickly, but it may limit custom flows later. A fully custom integration gives you more control, but it also hands your team more responsibility for security and ongoing maintenance. The right choice depends on where your business is now and what it needs next.

If conversion is already a priority, it helps to view payments through the same lens as checkout optimisation. Fundl's guide on driving growth is useful because it ties conversion performance back to practical customer journey decisions, which is exactly where payment friction shows up.

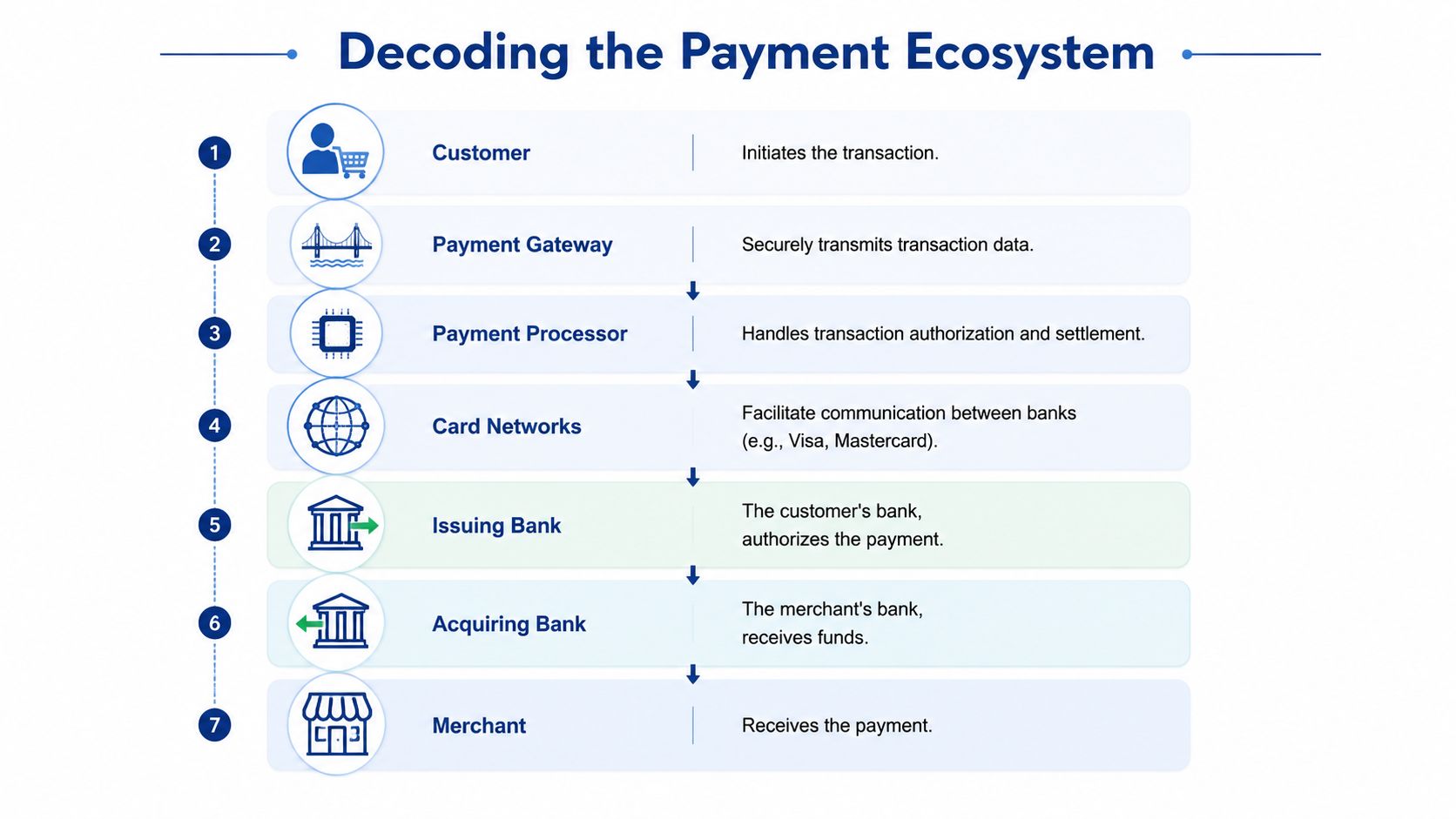

Decoding the Payment Ecosystem

A single card payment can pass through several companies before the money reaches your bank account. If those roles are unclear, it becomes hard to compare fees, explain declines, or predict cash flow.

People often use gateway, processor, and merchant account interchangeably. For buying decisions, that creates confusion. Each part affects a different business outcome, from checkout conversion to payout timing to fraud controls.

The core players

Payment gateway

The payment gateway handles the secure transfer of payment data from your checkout to the payment stack. In practice, it is the part closest to the customer experience. It affects page load, wallet support, 3D Secure flows, and whether checkout feels smooth or frustrating.

A poor gateway setup does more than create technical issues. It can increase cart abandonment, create duplicate payment attempts, and add support tickets from customers who are not sure whether an order went through.

Payment processor

The payment processor passes the transaction through the card and banking systems for authorisation and settlement. It communicates with card networks and issuing banks, then returns an approval or decline response.

This layer has a direct effect on approval rates and operating costs. Two providers can advertise similar pricing but perform differently on retries, local acquiring, and cross-border transactions. That matters for Canadian merchants selling into the U.S., accepting international cards, or trying to reduce declines from customers outside their home market.

Merchant account

A merchant account is the account structure that temporarily holds approved card funds before they are paid out to your business bank account. Some providers bundle it into one service, so you may never see it as a separate line item. It still shapes your day-to-day operations.

Reserve requirements, rolling holds, payout schedules, and underwriting rules usually sit here. For a startup, it can determine whether cash arrives in two days or a week. For a larger merchant, it can affect working capital, forecasting, and how much operational friction the finance team has to manage.

How a transaction actually moves

A standard ecommerce card payment usually follows this path:

The customer submits payment details on your checkout page or a hosted payment form.

The gateway secures and passes the data to the processor or payment platform.

The processor routes the authorisation request through the relevant card network.

The issuing bank reviews the request and decides whether to approve or decline it.

The response returns to checkout so the order can be confirmed or rejected.

Settlement happens after authorisation, and the approved funds move through the merchant account before payout to your bank.

The customer sees one checkout button. Your business is relying on several separate systems to approve the payment, screen risk, and release funds on time.

Why this matters to a non-technical owner

You do not need to master card network rules. You do need to know which layer controls which problem.

Checkout friction usually starts with the gateway or the way it is implemented.

Bank declines and approval rate issues usually involve the processor, acquirer, or issuer relationships.

Payout delays and reserve questions usually trace back to the merchant account and underwriting terms.

This matters even more if your business serves different customer segments at different stages. A startup may value fast setup and simple underwriting. An SMB may need better reporting, subscription support, and lower cross-border friction. An enterprise team may care more about routing control, redundancy, and negotiated interchange optimisation.

Canadian merchants often face extra complexity here. Cross-border sales, CAD and USD settlement, and support for customers who prefer non-card methods can all expose gaps in a basic payment setup. Businesses exploring alternative payout rails or understanding crypto-to-fiat solutions should treat those options as part of the wider payment ecosystem, not as separate experiments.

The practical takeaway is simple. “Payments” is not one tool. It is a stack of functions, and each function affects margin, customer trust, and how easily you can grow.

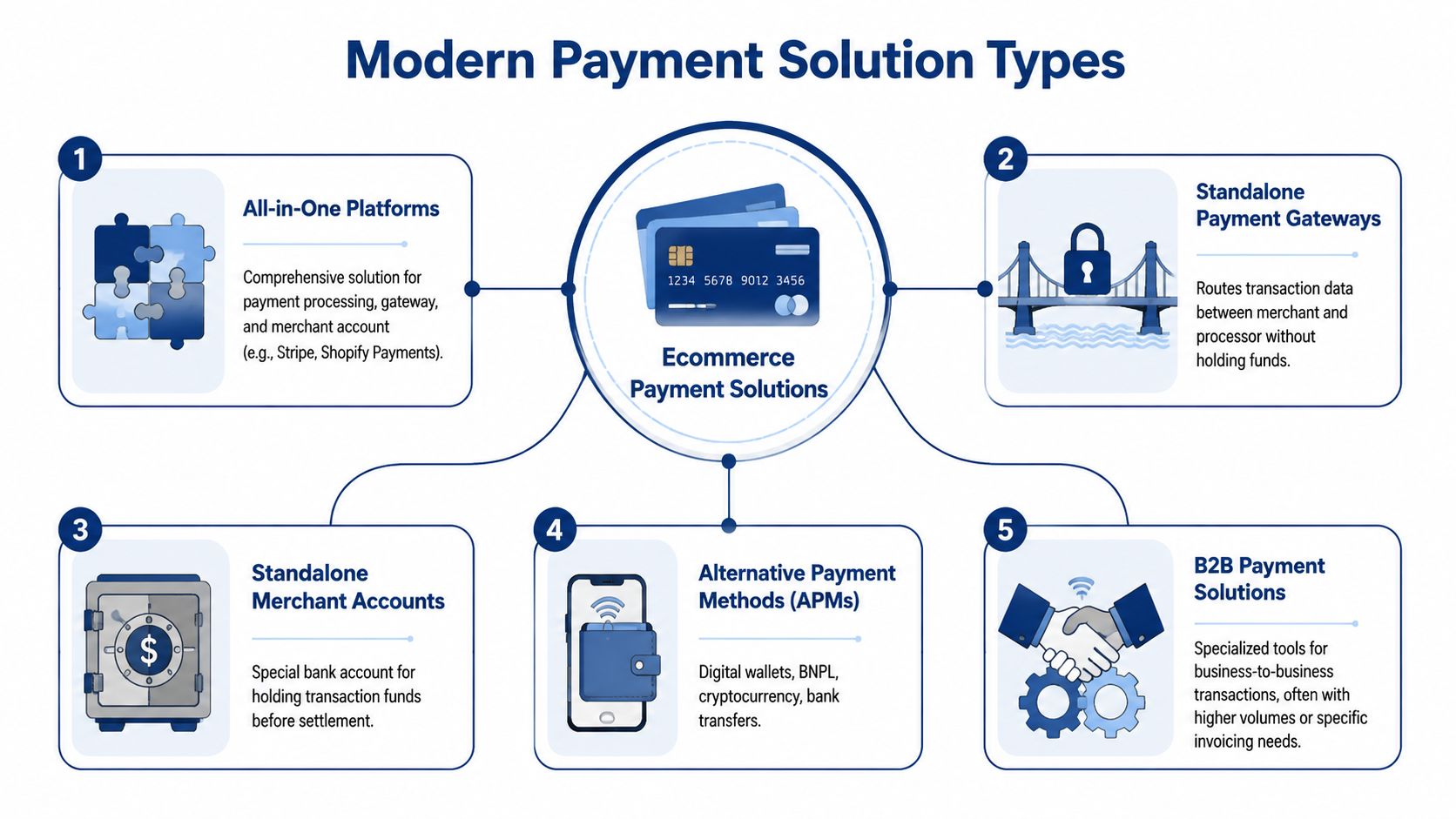

A Guide to Modern Payment Solution Types

When merchants ask for ecommerce payment solutions, they're often asking for several different tools at once. The label covers bundled platforms, standalone infrastructure, alternative payment methods, and specialised systems for business models like subscriptions or wholesale commerce.

The useful question isn't “Which provider is best?” It's “Which model fits how you sell?”

All-in-one platforms

Stripe, Shopify Payments, Square, and Adyen are common examples of platforms that bundle gateway functions, processing, and merchant account services into one package.

These platforms work well when you want speed, a simpler setup, and fewer vendor relationships to manage. They're especially useful for startups and lean teams that don't want to stitch together separate systems.

The trade-off is control. Bundled systems can limit how much flexibility you have over checkout design, routing logic, or specialised back-office workflows.

Standalone gateways and separate merchant accounts

This model splits the stack. One provider handles the secure transaction handoff, while another financial institution or processor handles settlement and merchant account services.

This approach can make sense if you need a specific acquiring setup, already have a merchant banking relationship, or want more flexibility in how the payment chain is assembled. It can also suit businesses with unusual risk profiles or strong internal technical capability.

It does create more operational coordination. When something goes wrong, your team may have to determine whether the issue sits with the gateway, processor, acquirer, or your own implementation.

Hosted checkout

Hosted checkout pages redirect the customer to a provider-managed payment page or display a provider-controlled payment environment to complete the purchase.

This is often the fastest way to launch securely. It also reduces the merchant's exposure to sensitive card handling. For many small businesses, that's a smart trade.

Hosted checkout is less ideal when branding and experience are central to the sale. Luxury retail, heavily customised subscriptions, and advanced upsell flows often outgrow a rigid hosted approach.

Embedded fields and direct API integrations

These options keep more of the payment experience inside your own site or app. With embedded fields, the provider still handles the sensitive card capture elements, but the customer experience feels more native. Direct API models give even more flexibility.

Businesses choose this route when checkout is part of the product experience, not just an admin task. It's common in custom ecommerce builds, marketplaces, mobile apps, and enterprise storefronts.

More control usually means more responsibility. That applies to payment design as much as it does to software in general.

Alternative payment methods

This group includes digital wallets such as Apple Pay and PayPal, bank transfers, BNPL services, and other non-card options.

These methods matter because customers don't all want to pay the same way. Some prefer the speed of a wallet. Others want instalment options. In some markets, local bank-based methods carry more trust than cards. Adding options can improve convenience, but too many poorly integrated methods can clutter checkout and complicate reconciliation.

For merchants exploring newer rails, it helps to understand how crypto-to-fiat settlement is being positioned in payout and cross-border contexts. The Coin Course offers a useful example in its coverage of understanding crypto-to-fiat solutions. That doesn't mean every merchant should accept crypto. It means the payment method strategy is broadening beyond traditional cards.

Subscription and recurring billing platforms

Recurring revenue businesses need more than one-time payment acceptance. They need dunning logic, proration rules, saved payment methods, invoice workflows, and failure recovery.

A standard processor can take recurring payments, but dedicated billing tools are often better for SaaS, membership businesses, replenishment commerce, and service retainers. If your revenue depends on renewals, retry logic and account updater features matter as much as the initial checkout.

B2B and omnichannel payment systems

B2B commerce often requires invoice support, account-based payment flows, approval processes, and higher-value transactions. Omnichannel businesses need online and in-person payment records to stay in sync.

If you run wholesale, field sales, retail, or service operations alongside ecommerce, the quality of integration between your online store, accounting system, POS, ERP, and payment tools becomes a serious selection factor.

How to Compare and Evaluate Payment Providers

Most provider pages are polished. That doesn't make them comparable.

A useful evaluation framework focuses on trade-offs you'll feel after launch: how much you'll pay, how much compliance work your team inherits, how smooth checkout feels, and whether the provider still fits once your business becomes more complex.

Start with the friction question

For Canada-focused ecommerce, checkout friction is a technical and commercial issue. Industry guidance notes that digital-wallet and autofill options remove manual card-entry steps and can shorten the authorisation path. It also notes that adding methods such as Apple Pay and PayPal can reduce input errors and fraud-review triggers, which improves approval probability and lowers abandonment, as described in Luqra's guide to ecommerce payment providers.

That changes the conversation. Payment method support isn't just a feature checklist. It affects whether a willing buyer completes the order.

The criteria that actually matter

Cost structure

Look beyond the headline transaction fee. Ask how pricing behaves across your order sizes, refund patterns, chargebacks, international payments, and payout schedule.

Flat-rate pricing is easier to understand. It's often suitable early on. More complex pricing models can become attractive once volume rises or your team can actively manage payment costs.

PCI and security burden

Some providers remove a lot of compliance work from your environment. Others leave more responsibility with your team.

If you don't have an in-house security capability, a solution that reduces your exposure is often worth more than a small fee difference. Cheap pricing can become expensive if your implementation increases compliance effort or incident risk.

Brand control

A checkout page that looks disconnected from the rest of your store can weaken trust. For some businesses, that's acceptable. For others, especially premium brands or custom buying journeys, it isn't.

Control matters most when checkout is tightly connected to conversion tactics like upsells, bundled offers, saved baskets, or account-based pricing.

International and cross-border readiness

If you sell outside Canada, ask practical questions:

Can the provider support multi-currency checkout without awkward redirects?

Does it handle local methods and regional compliance needs in your target markets?

Can your finance team reconcile international transactions cleanly without manual patchwork?

Integration effort

A provider can have strong features and still be the wrong choice if it creates too much implementation drag. Review API quality, SDK maturity, documentation, test tooling, and how well the provider integrates with your ecommerce platform, ERP, or CRM.

If you're planning a custom build, this guide to payment gateway software development gives a useful technical lens on what sits behind the integration decision.

Comparison of Payment Solution Models

| Model | PCI Compliance Burden | Cost Structure | Brand Control & Customisation | Ideal For |

|---|---|---|---|---|

| All-in-one platform | Lower relative burden | Usually simple and predictable | Moderate | Startups, lean teams, fast launches |

| Hosted checkout | Lower relative burden | Often straightforward | Lower | Small merchants prioritising speed and reduced security scope |

| Embedded fields or direct API | Higher relative burden | Varies by provider and setup | High | Brands that need custom checkout experiences |

| Separate gateway plus merchant account | Moderate to higher | Can be more tailored | Moderate to high | Businesses with specific banking or processing requirements |

| B2B or subscription-specific stack | Varies by architecture | Depends on workflow complexity | Moderate to high | SaaS, wholesale, invoicing-heavy, recurring billing models |

Decision test: Don't ask which provider has the longest feature list. Ask which one creates the least expensive problems for your current stage.

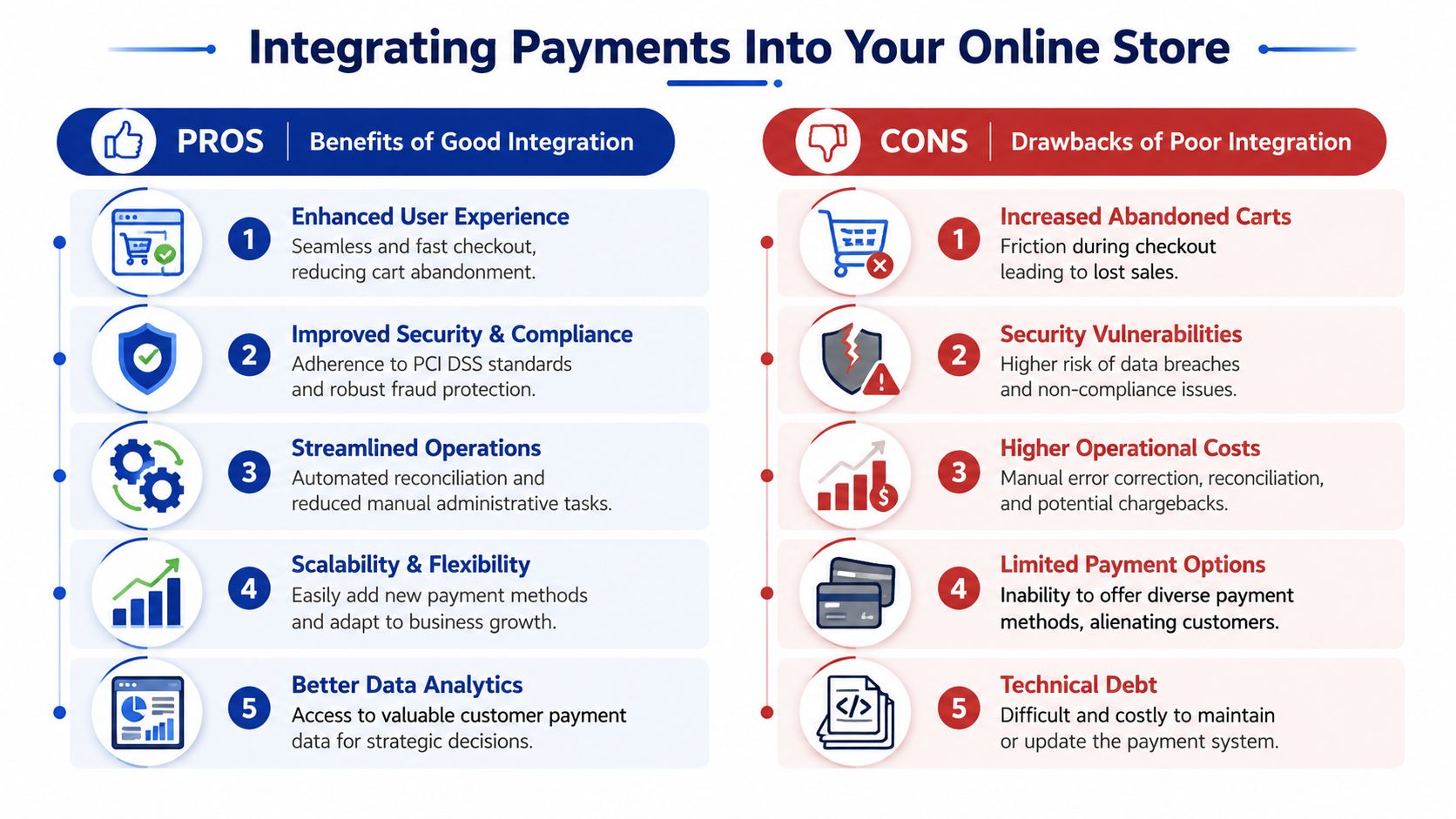

Integrating Payments Into Your Online Store

Checkout failures usually show up as lost revenue, support tickets, and abandoned carts long before they show up as a technical issue on an engineering roadmap. Integration choice decides how much of that risk you carry.

The practical decision is not just "can this provider process cards?" It is how payments will behave inside your store, your finance workflow, and your customer journey. For a startup, that usually means keeping implementation short and security scope contained. For an SMB, it often means balancing better conversion with manageable operational overhead. For an enterprise, the question shifts to control, resiliency, and how payments connect across channels, regions, and internal systems.

Hosted checkout keeps things simpler

Hosted checkout shifts more of the card-handling burden to the provider. That usually means less PCI exposure for your team, a faster launch, and fewer security decisions for your developers to get wrong.

That trade-off makes sense for merchants that need reliability more than design freedom.

Hosted checkout is often the better fit when:

You need to launch fast: A standard integration gets you to market without a long custom build.

Your team is lean: You avoid taking on extra compliance and security work internally.

Your checkout flow is conventional: Redirects or provider-controlled steps will not hurt your conversion enough to justify a custom implementation.

You are testing a new market: This is common for Canadian startups validating cross-border demand before investing in a more customised checkout.

The downside is control. A hosted flow can limit branding, add friction between cart and payment, and make it harder to support special cases such as mixed subscriptions, account credits, or underbanked customers who need payment methods beyond standard cards.

Direct integrations give you more control

A direct API or embedded payment-fields integration gives your team tighter control over checkout design and business logic. You can keep users on-site, shape mobile behaviour more carefully, and connect payment steps to loyalty, saved payment methods, subscriptions, or account-based purchasing.

That can improve conversion, but only if the team can support it well. Custom payment flows introduce more failure points. Decline handling, tokenisation, retries, webhook timing, reconciliation, and fraud review all need clear ownership.

This approach usually fits when:

Checkout is a conversion project, not just a payment form

Your business has special logic, such as subscriptions, B2B approvals, marketplace flows, or multi-entity tax and payout rules

You need regional flexibility, including cross-border selling or alternative payment methods that matter to Canadian buyers and newcomers with limited access to traditional banking

APIs and SDKs in business terms

For a business owner, the API is how your store sends payment requests and receives status updates. The SDK is the provider's developer toolkit that reduces custom work and speeds up implementation.

The business impact is straightforward. Good developer tools lower build time, reduce launch risk, and make later changes cheaper. Weak documentation or poor testing tools create delays, billing mistakes, and hard-to-diagnose checkout issues.

Payments also do not live in isolation. Refunds affect finance. Order status affects fulfilment. Failed captures affect customer service. If you are planning wider system work, this guide to ecommerce integrations in Canada is worth reviewing because payment data usually needs to flow into inventory, shipping, accounting, analytics, and CRM systems.

Poor integration creates costs in places many merchants do not budget for at the start. Staff spend more time fixing orders manually. Finance teams reconcile payouts by hand. Customers lose confidence when payment status and order status do not match. Those are integration problems, but they land as business problems.

Selecting the Best Payment Stack for Your Growth Stage

There isn't one best payment stack. There's a best-fit stack for the stage your business is in today, the team you have, and the kind of growth you expect over the next few years.

That's why a startup shouldn't copy an enterprise architecture, and an enterprise shouldn't keep operating with a startup payment setup once scale, channels, and geography become more complex.

For startups

A startup usually needs three things from payments: fast launch, acceptable risk, and low operational drag.

In practice, that often means an all-in-one platform with hosted or semi-hosted checkout, standard wallet support, and simple reporting. The goal isn't perfection. It's getting to market with a checkout that customers trust and a back office your team can manage.

A startup should prioritise:

Fast implementation: Choose a provider with strong out-of-the-box ecommerce support.

Clear operations: Keep refunds, payouts, disputes, and reporting manageable.

Basic flexibility: Make sure wallets, recurring billing, or cross-border support can be added later if needed.

What usually doesn't work at this stage is overbuilding. A custom payment orchestration layer sounds advanced, but most early-stage teams don't need it and won't maintain it well.

For small and mid-sized businesses

SMBs need balance. At this stage, you've likely learned that checkout design, fraud controls, and international sales start to affect margins and growth more visibly.

At this point, merchants should become more deliberate about payment method mix, customer trust signals, and regional support. For Canadian businesses, one frequently ignored issue is inclusion. Guidance on underserved payment users notes that useful design should address whether merchants need cardless, wallet-based, and lower-friction options for shoppers who may have access to digital payments but do not consistently use them, which is especially relevant for small and mid-sized Canadian merchants trying to reduce abandonment, as discussed in the Boston Fed's framework for underserved digital payment households.

That has practical consequences. If your checkout assumes every customer is comfortable with saved cards, one-click flows, or repeated credential prompts, you may be losing legitimate buyers without realising it.

What SMBs should add:

Wallet and lower-friction methods: These help customers who don't want to type card details or don't fully trust card storage.

Cross-border capability: If you sell into the U.S. or beyond, review currency display, settlement flow, and support for international transactions.

Better fraud tuning: Don't rely only on default rules if false declines are hurting approvals.

Reconciliation discipline: As methods expand, operations can get messy unless reporting stays consolidated.

Some SMBs reach the point where a custom integration or a more customised payment layer makes sense. That's often where firms like Cleffex Digital Ltd's custom fintech software development team can fit, alongside providers and platforms, when a business needs software around the payment stack rather than just a standard plugin.

A growing merchant doesn't just need more payment methods. It needs a checkout that serves different levels of trust, comfort, and buying intent.

For enterprises

Enterprises should think in terms of resilience, control, and optimisation.

A large retailer, insurer, marketplace, or multi-brand operation often needs more than one provider relationship. It may want routing flexibility, regional acquiring options, failover capability, and tighter links to ERP, CRM, fraud tooling, and finance systems. At this level, payment operations become a core business function.

Enterprise priorities usually include:

Payment orchestration

Using multiple providers can reduce dependency on a single vendor and support regional optimisation.Cross-border and multi-currency design

Generic advice says to “accept more currencies.” In reality, the challenge is balancing conversion benefits against processing cost, fraud controls, and compliance overhead.Channel consistency

Online, mobile, subscription, invoice, and in-person data should reconcile into one operational view.Governance

Finance, legal, security, product, and engineering all need a say in how payments evolve.

What fails at the enterprise level is fragmented ownership. If marketing optimises checkout, finance owns reconciliation, legal reviews compliance, and engineering controls implementation, but no one owns the full payment strategy, the stack becomes expensive and slow to improve.

A stage-based shortlist mindset

A useful rule of thumb is simple:

| Business stage | Sensible starting model | Main risk to avoid |

|---|---|---|

| Startup | All-in-one, hosted or semi-hosted | Overengineering |

| SMB | Flexible platform with stronger method mix and selective customisation | Adding complexity without operational control |

| Enterprise | Multi-provider, integrated, strategically governed stack | Fragmentation and vendor lock-in |

Your Next Steps in Building a Winning Payment Strategy

The strongest ecommerce payment solutions do four jobs at once. They help customers pay the way they prefer. They protect sensitive data without loading your team with unnecessary compliance work. They fit your current operating model. And they leave room for the business you're trying to become.

That means the right payment decision is rarely about features alone. It's about fit. A startup should value speed and reduced risk. An SMB should focus on friction, inclusion, and practical cross-border support. An enterprise should design for resilience, governance, and integration depth.

The direction of travel is clear. Real-time payments are expanding globally, with systems now available in over 100 countries, and Mastercard projects 575 billion RTP transactions by 2028, representing 27% of all electronic payment transactions, while global cashless payment volumes are projected to rise by more than 80% between 2020 and 2025, reaching nearly 1.9 trillion transactions, according to Mastercard's payments trends for 2025 and beyond. Merchants don't need to chase every trend, but they do need a stack that won't block the next sensible move.

A good next step is to review your checkout from three angles: customer friction, compliance exposure, and growth constraints. If one payment decision touches all three, it deserves board-level attention, not just a plugin install.

If you're evaluating ecommerce payment solutions and need help translating business goals into a practical architecture, Cleffex Digital Ltd can help scope the right stack, integration model, and supporting software for your stage of growth.