You're probably seeing the same pattern in your business right now. A customer gets close to buying, applying, or booking, then hits a point where money has to move. Suddenly, they're pushed to a bank page, a financing form, or a third-party portal that looks nothing like your brand. Some complete the process. Many don't.

That gap is where embedded finance solutions matter. They let a non-financial business offer payments, lending, insurance, payouts, or account-like experiences inside the product customers already trust. For a Canadian business leader, that sounds attractive. It also raises harder questions. Who carries the regulatory burden? What happens to customer data? How do PIPEDA and OSFI requirements affect the design?

Those are the questions most generic guides skip. This one doesn't.

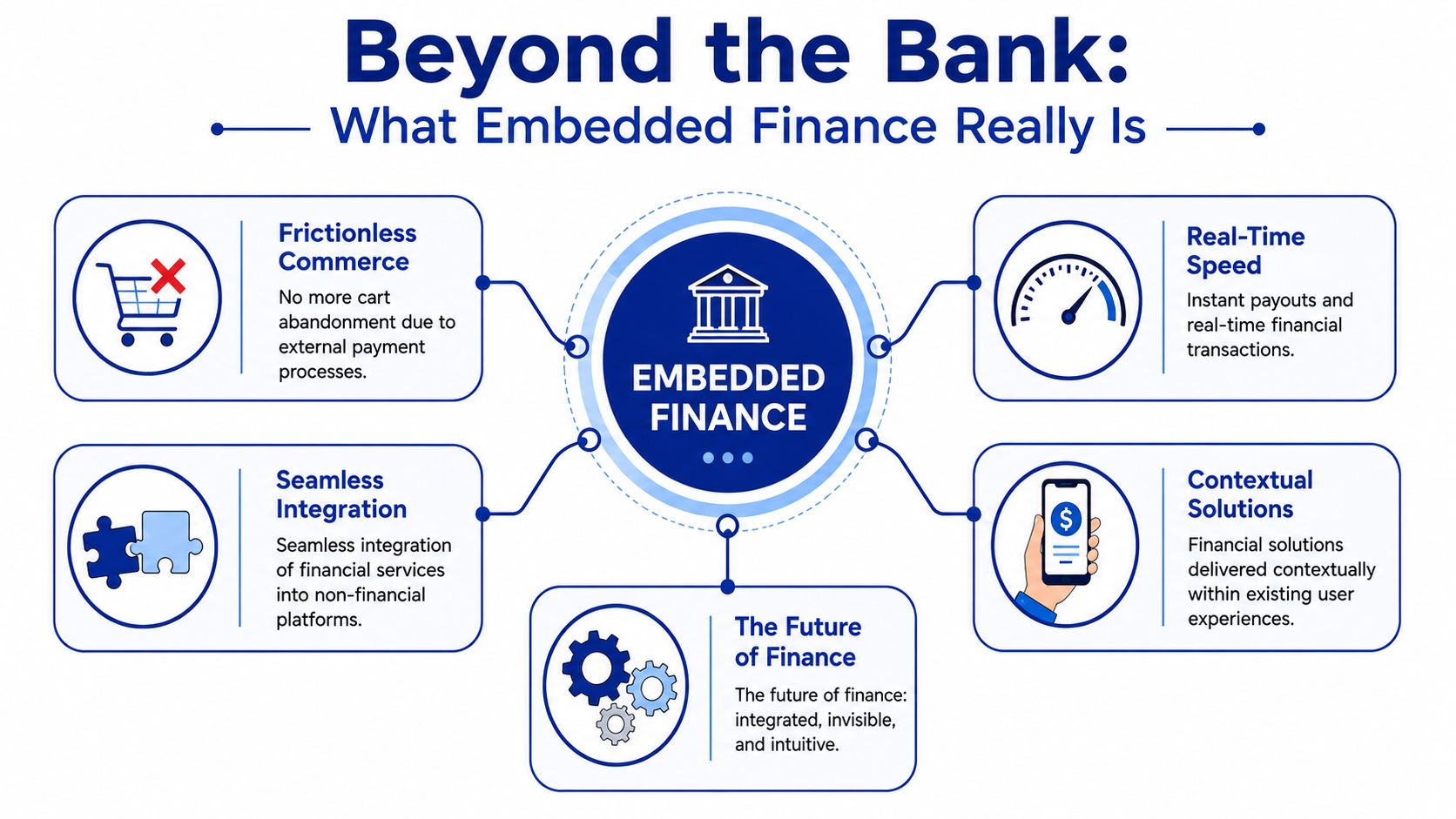

Beyond the Bank: What Embedded Finance Really Is

Embedded finance is easiest to understand when you stop thinking about it as a banking product and start thinking about it as infrastructure.

Electricity is a useful analogy. People don't buy a house because it has wires behind the walls. They value what those wires enable: light, heat, internet, and appliances. Embedded finance works in a similar way. Your customer doesn't wake up hoping to “interact with financial infrastructure”. They want to pay, get approved, receive funds, or protect a purchase without friction.

The shift from destination to built-in utility

In the old model, finance sits somewhere else. Your customer shops on your site, then gets redirected. Your patient books with your clinic, then has to call a financing provider. Your policyholder submits a claim, then waits while payment moves through disconnected systems.

With embedded finance solutions, the money step stays inside the experience.

That might mean:

At checkout: A shopper pays or selects an instalment option without leaving your store.

Inside a claims portal: A customer receives a digital payout in the same place they filed the claim.

Within business software: A small business user accesses payments or working capital from the platform they already use every day.

Why businesses care now

This isn't a niche add-on anymore. The global embedded finance market is projected to grow from USD 148.38 billion in 2025 to approximately USD 1,732.53 billion by 2034, at a CAGR of 31.53%, and the embedded payment segment held 39% of revenue share in 2024, according to Precedence Research's embedded finance market analysis.

That scale matters because it shows a broad business shift. Customers increasingly expect financial tasks to happen where the need arises, not on a separate website.

Practical rule: If a customer has to pause their main task to “go deal with finance somewhere else”, you've introduced friction at the worst possible moment.

What it is and what it isn't

A lot of confusion comes from treating embedded finance as one product. It isn't. It's a delivery model.

A simple way to frame it:

| Term | Plain meaning |

|---|---|

| Embedded payments | Paying inside your app, portal, or checkout |

| Embedded lending | Offering credit or financing during a transaction or workflow |

| Embedded insurance | Presenting protection options in the buying journey |

| Embedded payouts | Sending money to users directly within your platform experience |

The key idea is context. Finance appears when it solves an immediate problem. That's why embedded finance solutions often feel less like “extra features” and more like a smoother version of the service your business already provides.

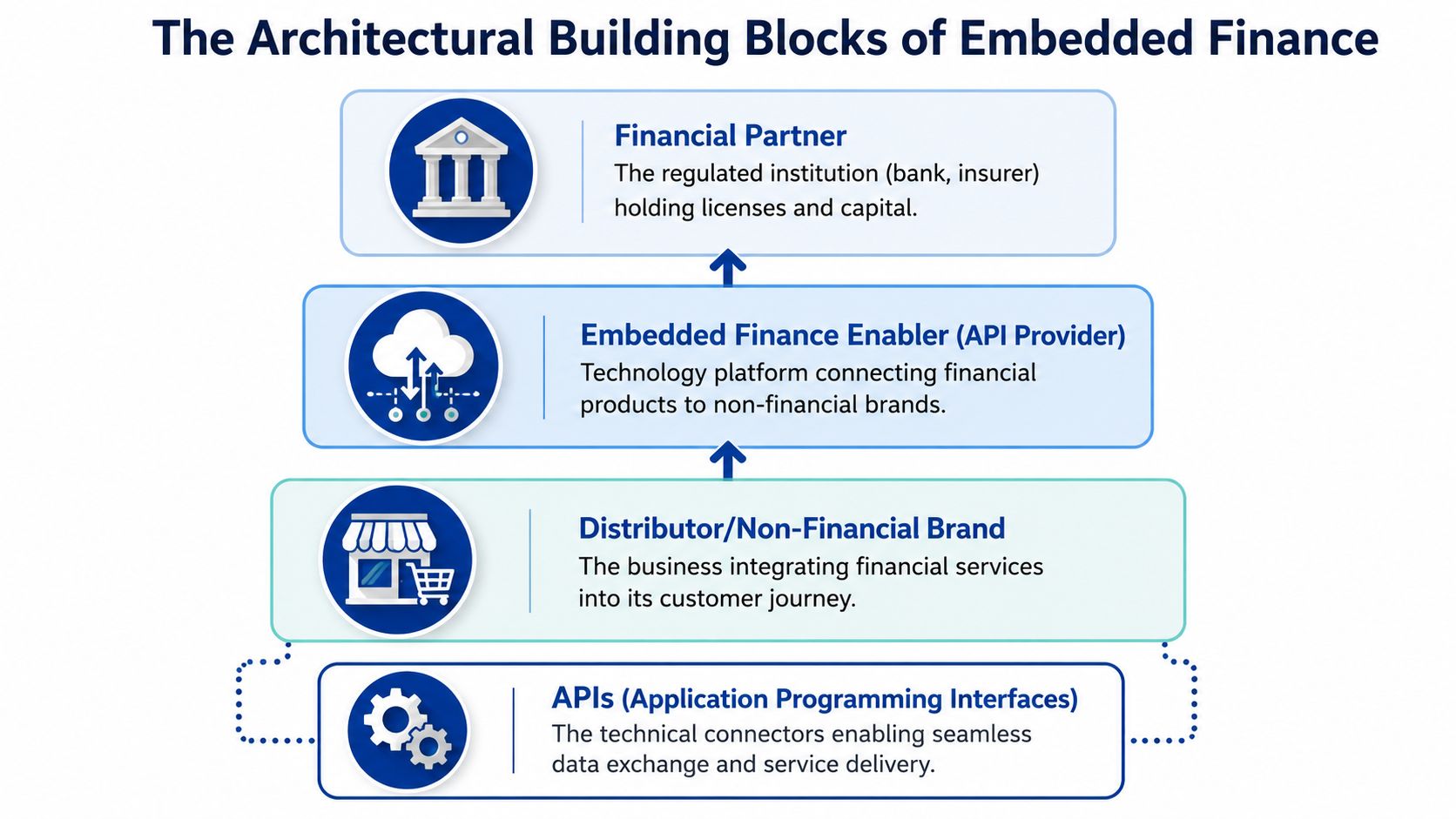

The Architectural Building Blocks of Embedded Finance

The technology stack sounds intimidating until you break it into layers. Most embedded finance solutions in Canada involve three parties working together, plus one technical connector that ties them all together.

The three layers that make it work

At the top sits the financial partner. That's usually a bank, lender, insurer, or other regulated provider. They hold licences, manage capital, and take responsibility for the underlying financial product.

In the middle is the embedded finance enabler. This is the platform that exposes the financial capability through APIs, SDKs, workflow tools, and compliance features. If the bank is the engine, the enabler is the transmission system that lets another business use it.

At the customer-facing layer is your application. That might be your e-commerce site, patient portal, dealership system, claims app, or SaaS platform.

APIs are the Lego blocks

An API is a controlled way for one system to ask another system to do something. In embedded finance, that could be:

Create a payment

Check identity

Request a loan offer

Issue a refund

Trigger a payout

Lego is a better mental model than plumbing. You don't need to rebuild the whole house. You connect standardised blocks to assemble a new capability.

That's one reason finance is showing up inside software products that weren't built as banks. A vertical SaaS company, for example, can plug payment or lending functions into an existing workflow instead of replacing its entire platform. If you're already modernising finance operations more broadly, ReceiptsAI's automation guide is a useful companion because it shows how financial workflows become more valuable when they're connected rather than handled in isolated tools.

Why architecture choice changes the business result

The biggest technical mistake is treating embedded finance like a bolt-on widget. That often leads to a monolithic setup where one failure can disrupt the entire user journey.

Modern systems usually work better with modular APIs and microservices. Instead of one large application doing everything, smaller services handle distinct jobs such as identity checks, ledger updates, payment initiation, notifications, and reporting. That makes the system easier to change, test, and scale.

In Canada, that architectural choice has had a measurable impact. Embedded finance solutions using modular API architectures have reduced transaction latency by 40–60% for SMEs, and a 2025 CDAP report found that 68% of SMEs integrating these APIs saw a 35% increase in customer retention due to the smoother in-platform experience.

Embedded finance rarely fails because “the API didn't work”. It usually fails because the business stitched together disconnected services without a clear orchestration layer.

The orchestration layer most leaders miss

Orchestration is the traffic control system. It coordinates all the steps behind a simple user action.

Take a repair financing request at an automotive service centre. One tap from the customer might trigger identity verification, affordability checks, lender routing, consent capture, approval logic, contract generation, and payment release. The customer sees one clean flow. Your systems handle a chain of specialised actions.

That's why open banking and banking API design matter even for non-banks. If you want a clearer view of how Canadian firms approach these integrations, this complete guide to Canada's open banking solutions gives helpful context around the broader ecosystem.

Unlocking New Revenue and Lasting Customer Loyalty

A lot of executives first approach embedded finance as a product enhancement. That's too narrow. The stronger case is strategic. Embedded finance solutions can change where revenue is earned, how loyalty is built, and which company controls the customer relationship.

Revenue moves closer to the point of action

When finance is integrated into the same flow as the primary transaction, the business stops treating payments or financing as back-office necessities and starts treating them as part of the commercial model.

There are several ways this can create value:

Transaction participation: A platform may share in the economics tied to payment volume.

Service expansion: A business can add financing, protection, or payout features without becoming a bank.

Higher workflow completion: Customers are less likely to stall when the final money step stays in context.

The wider market supports that logic. In North America and Europe, the total addressable market for embedded finance across core categories is about $185 billion, with only around $32 billion currently captured, meaning over 80% remains untapped, according to BCG's analysis of embedded finance adoption.

Loyalty improves when the workflow feels complete

Customer loyalty often sounds abstract until you map where customers leave. A platform becomes “sticky” when it removes extra steps. If your software helps someone run payroll, book treatment, file a claim, or manage inventory, they're more likely to stay when it also handles the money movement tied to that task.

That's why embedded payments have become so influential inside vertical software. BCG notes that SaaS providers with integrated payment solutions accounted for 36% of SME acquiring revenues in the last year, with a projection to reach 45% by 2028 in the same BCG embedded finance report.

The business case is often clearer in B2B than leaders expect

Many people associate embedded finance with consumer checkout. But Canadian businesses should also look at B2B scenarios where cash flow timing shapes buyer behaviour.

For example, a distributor or marketplace can use embedded payment terms to reduce friction between invoice creation and settlement. If you want a practical comparison point outside Canada, this guide to UAE B2B payment terms shows how financing terms become part of the commercial experience rather than a separate negotiation.

If customers depend on your platform to complete a high-value task, adding finance at that exact moment can deepen the relationship more effectively than adding another dashboard or reporting feature.

The important nuance is this: revenue potential is real, but it only compounds when the customer experience, partner model, and data strategy are designed together.

Embedded Finance Use Cases Across Canadian Industries

Abstract definitions only go so far. The clearest way to understand embedded finance solutions is to watch what changes in a real customer journey.

Insurance claims that don't end in waiting

A policyholder opens an insurer's mobile app after a minor home incident. They upload photos, answer a few questions, and receive a decision. The old process would end there, with the payment arriving later through another channel.

With embedded payouts, the claim and the disbursement sit in one experience.

The user doesn't need to wonder which department has the file or when funds will appear. For the insurer, that changes the emotional tone of the claim. The digital channel no longer just collects information. It resolves the problem.

Healthcare portals that handle treatment and payment together

Healthcare administrators know the awkward moment well. A patient is ready to proceed with a treatment plan, but hesitates when they see the out-of-pocket amount. If the clinic sends them elsewhere to sort out financing, the delay can undermine both conversion and trust.

An embedded finance approach keeps the payment plan inside the clinic portal. The patient reviews options in the same secure environment where they manage appointments and forms.

A useful way to think about it is not “selling credit”. It's reducing the administrative distance between medical decisions and financial clarity.

Automotive service centres that solve the surprise repair problem

Vehicle owners rarely plan for urgent repairs. They authorise diagnostics, hear the quote, and then face a sudden affordability decision at the service desk.

A dealership or service centre using embedded finance can present approved financing options during the repair workflow itself. The customer doesn't need to search for a lender on their phone in the lobby. The service advisor doesn't have to turn into an amateur loan broker.

That makes the conversation more practical:

The service team keeps the repair order moving.

The customer sees manageable options in real time.

The business reduces the risk that approved work gets postponed.

Small retailers and startups that want smoother checkout

For an online seller, the most familiar use case is checkout. A shopper fills the cart, enters details, and gets to the final screen, a point when momentum is highest, and patience is lowest.

Embedded payments and pay-later options work because they keep the buyer in one branded flow. The customer doesn't need to re-enter information in a new interface or wonder whether they've been redirected to a trusted partner.

Software companies serving other businesses

The B2B version is often even more compelling. A Canadian SaaS platform serving trades, clinics, legal practices, or field service firms can embed payments into invoicing, collections, deposits, or recurring billing. That changes the software from a system of record into a system of action.

The best use cases don't feel like finance products. They feel like the shortest path between the customer's intent and the completed task.

The common thread across industries is timing. Embedded finance works best where a financial decision sits inside a broader workflow, and removing interruption improves the whole experience.

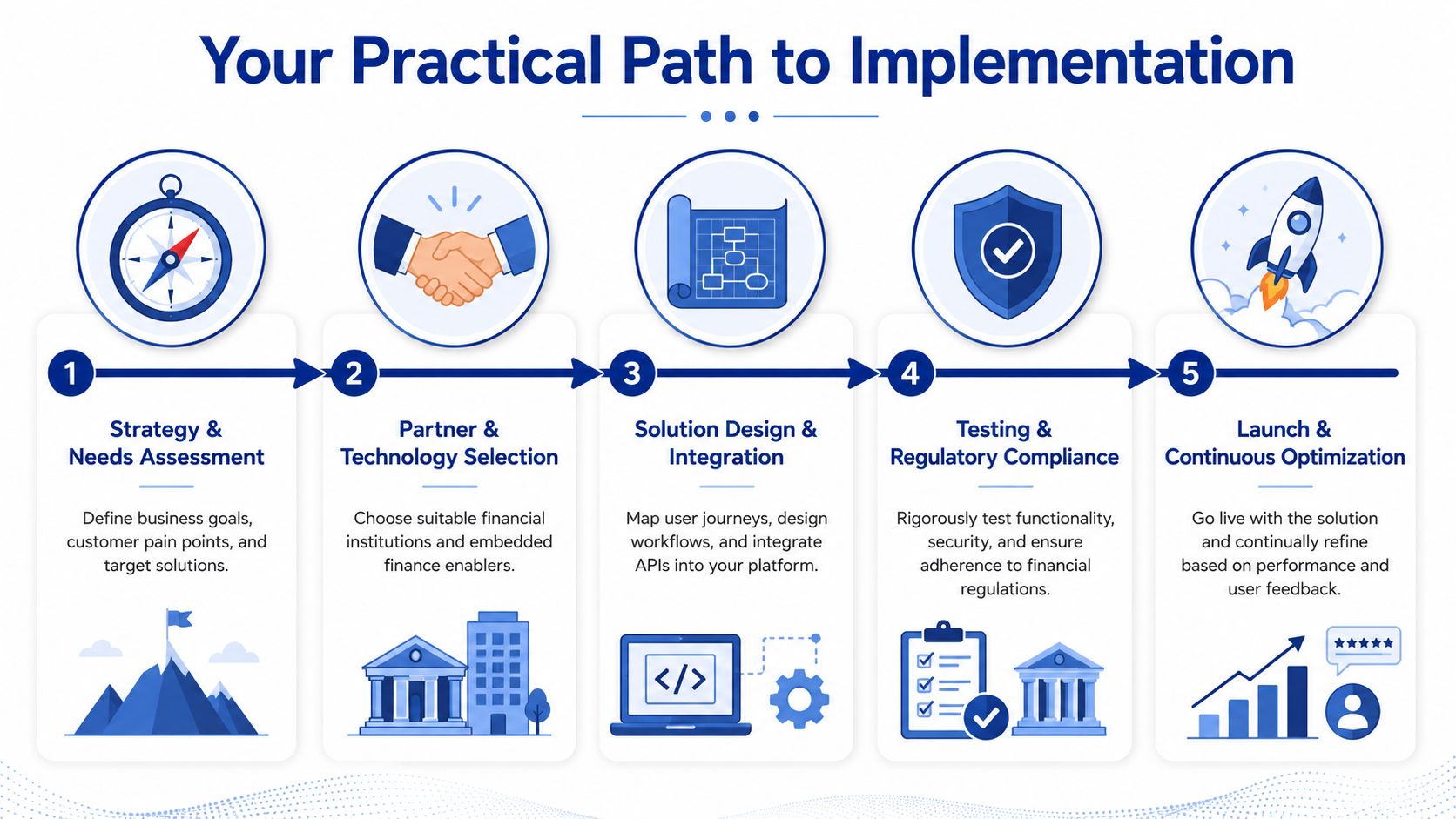

Your Practical Path to Implementation

Most failed projects don't fail because the idea was wrong. They fail because the business tried to launch a complex financial capability before it had clarity on use case, partner fit, security design, and operational ownership.

Start with one high-friction moment

A good implementation starts with a narrow problem, not a broad ambition. Don't begin with “we want embedded finance”. Start with a moment where customers or staff lose momentum because money has to move through a disconnected process.

That could be:

A checkout drop-off point

A claims payout delay

A patient financing handoff

A repair approval bottleneck

An invoice payment lag inside a SaaS workflow

Choose one use case where the financial step is already present and painful. That makes the value easier to prove.

Evaluate partners like an operator, not a buyer

Vendor selection shouldn't focus only on feature lists. You're assessing whether the provider can support a regulated, customer-facing workflow over time.

Look for signals such as:

API quality

Clear documentation, stable versioning, and predictable behaviour matter more than a flashy demo.Compliance support

The partner should explain responsibilities plainly. Who handles identity, consent, audit trails, and reporting?Operational transparency

Can your team see failures, retries, and exceptions in real time?Commercial clarity

Pricing needs to be understandable before volumes scale.

If your internal team wants a more technical planning reference, this banking API development guide from start to finish is a practical resource for framing integration decisions.

Build for Canadian compliance from day one

For Canadian implementations, the technical baseline isn't optional. Solutions must comply with the 2023 PIPEDA and the 2025 OSFI Digital Identity Standard, requiring AES-256 encryption and OAuth 2.0. Successful platforms also use event-driven microservices, which have been associated with a 50% increase in system resilience and a drop in failure recovery time from 45 minutes to under 8 minutes.

Those details matter because they affect architecture choices early. If your platform stores customer consent poorly or treats audit logging as an afterthought, remediation becomes expensive.

A simple checklist helps:

| Area | What to confirm |

|---|---|

| Identity and access | OAuth 2.0 flows are properly designed and monitored |

| Data protection | Sensitive data is encrypted with AES-256 in transit and at rest where required |

| Auditability | Real-time logging captures who did what, when, and through which service |

| Resilience | Event-driven services can fail gracefully without breaking the full journey |

Implementation test: If your compliance lead, product lead, and engineering lead can't all explain the customer flow in the same way, the design isn't ready.

Launch small, then harden the workflow

The first launch shouldn't aim for maximum feature breadth. It should aim for controlled learning.

A sensible rollout often includes a limited customer segment, one workflow, and clear exception handling. Teams should review not just adoption, but edge cases: failed payments, approval reversals, duplicate submissions, support escalations, and data handoff issues.

Embedded finance solutions reward discipline. The businesses that do well are usually the ones that treat the launch as an operational capability, not a feature release.

Navigating Common Challenges and Hidden Risks

The optimistic version of embedded finance says you add a few APIs, improve customer experience, and generate new revenue. That story leaves out the harder Canadian reality.

Regulatory uncertainty is a business blocker

For many SMEs, the main problem isn't technical integration. It's uncertainty about what they're allowed to offer, under whose licence, and with which controls.

A 2025 Canadian Bankers Association report found that 68% of Canadian SMEs cite regulatory uncertainty as their primary barrier to adopting embedded finance. That concern is understandable. Generic vendor playbooks rarely explain the practical boundary between a software platform, a regulated financial activity, and a licensed partner.

Legal, compliance, and product teams need to work together early. If your organisation is sorting through Canadian requirements, this overview of fintech compliance solutions is a useful starting point for framing governance discussions.

Data sovereignty is the risk many teams notice too late

The less discussed issue is data control.

A business might launch embedded payments or financing and assume it's strengthening customer loyalty. But if the fintech partner controls transaction records, behavioural signals, or consent history, your company may lose visibility into the very relationship it wanted to deepen.

That risk is especially important in Canada, where data handling expectations under PIPEDA push businesses to be explicit about collection, use, access, and accountability. If customer insight is fragmented across partners, your support teams, marketers, and operators may all end up working with partial information.

Practical ways to reduce the downside

You don't eliminate risk by avoiding embedded finance. You reduce risk by structuring the operating model properly.

A more resilient approach includes:

Data contract discipline

Define who owns transaction data, who can use it, and how it can be exported before signing the commercial agreement.Role clarity with partners

Ask the provider to map which compliance obligations sit with them and which remain with your business.Traceable customer consent

Don't rely on vague platform terms. Make consent states visible, reviewable, and auditable.Exit planning

If you change providers later, can you migrate records, customer history, and workflow logic without losing continuity?

The hidden cost of a poorly designed embedded finance programme isn't only compliance exposure. It's losing direct understanding of your own customer while someone else sits in the middle of the transaction.

The strongest Canadian operators treat embedded finance as both a growth initiative and a control question. They ask not only “Can we launch this?” but also “What relationship assets are we giving away if we do?”

Planning Your First Embedded Finance Pilot Project

The safest first move isn't a platform-wide rollout. It's a pilot tied to one business problem that matters enough to test but is small enough to control.

Pick the use case with the clearest business pain

A strong pilot usually has three qualities. Customers already feel the friction. Your team can describe the current process without guessing. And the value of fixing it is visible to both operations and leadership.

Good candidates often include:

A checkout payment step with obvious abandonment risk

A claims payout flow that creates avoidable waiting

A patient payment-plan handoff that slows approvals

An invoice collection flow inside a business portal

A service financing option for urgent repairs

Don't choose the most ambitious idea. Choose the one your organisation can explain in one sentence.

Use a simple screen before committing resources

Before selecting a partner or building anything, test the idea against four questions:

| Question | What a good answer sounds like |

|---|---|

| Customer fit | “Users already need this in the workflow” |

| Operational fit | “A team owner can manage exceptions and support” |

| Compliance fit | “We know which partner and controls are required” |

| Data fit | “We can preserve access to the insight created” |

If one of those answers is vague, the pilot probably isn't ready.

Define success in plain language

For a first pilot, success measures should be practical. Did customers complete the workflow more smoothly? Did staff spend less time chasing manual follow-up? Did the business gain clearer visibility into payment or financing status? Did support issues stay manageable?

This is also the stage where financial risk discipline matters. If you want a broader lens on operational preparedness, this practical guide to financial resilience is helpful because it frames risk management as an ongoing capability rather than a policy document.

A good pilot does more than test demand. It tests coordination across product, engineering, compliance, finance, and customer support. That's why the first embedded finance project is often more valuable as an organisational learning exercise than as a revenue event.

The businesses that move well in this space usually do one thing differently. They start narrow, document everything, and build a repeatable decision model before expanding into the next use case.

If your team is weighing an embedded payments, lending, insurance, or payout initiative in Canada, Cleffex Digital Ltd can help you scope the right pilot, assess architecture options, and design a compliant implementation path that fits your business model.