A lot of fintech teams hit the same wall at the same moment. The product finally gets traction, inbound demos increase, partners want integrations, and usage patterns stop being predictable. Then the cracks show. Logins slow down during peak periods. Payment retries pile up. Support gets flooded with “it spun forever” tickets. Finance wants cleaner reconciliation. Compliance wants a stronger audit trail. Engineering wants to stop patching a system that was never designed for this level of demand.

That's usually when scalability stops being an abstract technical objective and becomes a board-level business issue.

In Canada, that urgency is easy to understand. The fintech market is projected to reach about USD 52.92 billion by 2030, up from roughly USD 31.78 billion in 2024, according to this Canadian fintech market outlook. For any firm building payment products, embedded finance workflows, insurance platforms, healthcare payment systems, or SMB finance tools, that growth changes the architecture conversation. The question is no longer whether the platform will need to scale. The question is whether it will scale without driving up cost, risk, and delivery time.

The Inevitable Growing Pains of Fintech Success

A common failure pattern looks deceptively simple.

A team launches with a compact stack, a shared application server, one transactional database, some background jobs, and a few third-party integrations for KYC, payments, and notifications. In the early months, that setup works. Releases are fast. The team knows the whole system. Costs stay contained.

Then demand becomes uneven.

A payroll processing window creates a spike in authentication traffic. An insurer opens digital claims after a major event and uploads them to the same database used by customer-facing APIs. A healthcare payments workflow triggers more downstream calls than anyone expected. What looked efficient at low volume starts behaving like a queueing problem. The web app might still be up, but customers feel the platform is failing in slower and more expensive ways.

Where Systems Usually Break First

Most fintech products don't collapse because one server runs out of CPU. They break because growth exposes hidden coupling.

Shared databases become choke points when reads, writes, reporting, and reconciliation all compete for the same resources.

Third-party dependencies create uneven latency because your platform can only move as fast as the slowest KYC, banking, or fraud service in the request path.

Manual operations stop scaling when exceptions, reviews, and compliance checks grow faster than the operations team.

Release risk increases because tightly coupled services make every deployment feel like a full-system event.

Practical rule: If one feature launch can slow down login, payment authorisation, and reconciliation at the same time, the issue isn't traffic alone. It's architecture.

Many executives hear “we need microservices” and immediately worry that the answer is just a more fashionable kind of complexity. Sometimes that concern is justified. Scalability isn't about replacing one buzzword with three new ones. It's about designing a system that can absorb more users, more transactions, and more regulation without turning every growth milestone into an outage or a rewrite.

Why This Matters More in Canada Now

For Canadian fintech teams, timing matters. The domestic market is moving from niche digital convenience into mainstream financial infrastructure. That has direct implications for insurance carriers handling event-driven claims surges, healthcare organisations modernising billing and payments, and SMB platforms that need stable integrations with banking and reporting workflows.

A platform that works for a controlled pilot often doesn't work for a wider commercial rollout. Authentication volume grows. Payment activity becomes bursty. Fraud controls need to run in real time instead of after the fact. Reporting demands become more complex because leadership, finance, and auditors all want different views of the same data.

The practical lesson is simple. Scalable fintech solutions aren't a late-stage optimisation. They are the condition that lets growth happen safely.

What Makes a Fintech Solution Truly Scalable

Scalability gets reduced to “can the app handle more users?” That's too narrow to be useful.

A better analogy is a restaurant kitchen. A single chef can cook excellent meals for a small dining room. If demand doubles, you can buy a bigger stove and a faster mixer. That's vertical scaling. It works for a while. But once orders become continuous, the better move is to split work into stations, prep in parallel, separate dine-in from delivery, and redesign the handoff process. That's horizontal scaling. It changes the system, not just the hardware.

In fintech, the same distinction matters. A bigger server might buy time. It won't solve systemic contention between onboarding, ledger writes, fraud checks, reporting, and partner API calls.

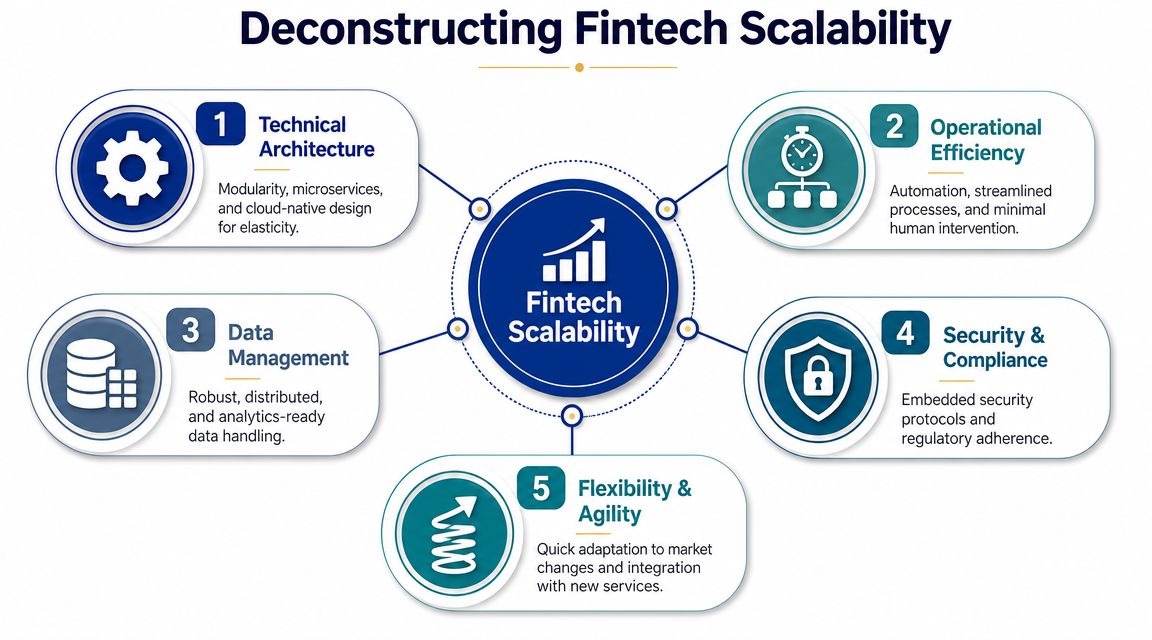

The Five Dimensions That Matter

A fintech platform is only scalable if it performs well across several dimensions at once.

Capacity under load means the system can handle more traffic and more transaction volume without sharp degradation.

Elasticity means it can expand during peaks and contract during quieter periods, so cost doesn't rise in a straight line with provisioned infrastructure.

Resilience means partial failures don't become full-service incidents.

Operational scalability means support, compliance, and reconciliation don't require more people linearly as the business grows.

Economic scalability means unit costs stay controlled as usage increases.

These aren't separate concerns. They reinforce each other. A platform that only scales technically but requires manual review for every exception will still stall the business. A platform that keeps costs low but can't isolate failures will create expensive outages and reputational damage.

Canadian Payment Volume Makes the Problem Concrete

In 2023, Canadians made 23.6 billion payment transactions totalling $11.9 trillion, with electronic payments forming the vast majority, according to this analysis of fintech transaction scale. That tells you something important about the environment fintech products operate in. Even if your platform handles a fraction of that activity, your users expect the same continuity, speed, and reliability they get from larger financial systems.

For product leaders, that translates into a few practical design consequences:

Separate interactive and background work. Customer-facing requests shouldn't wait for non-critical downstream processing.

Design for burst behaviour, not average traffic. Average load is the wrong planning model for payroll runs, premium cycles, and claims events.

Instrument the whole path. Front-end speed means little if the bottleneck sits in KYC, ledger posting, or settlement confirmation.

A scalable platform doesn't just stay online. It keeps the most important customer journeys fast when everything else is busy.

What Works and What Usually Doesn’t

What works is boring in the best sense. Small, well-bounded services. Queue-based workflows for non-blocking tasks. Clear ownership of data. Explicit service-level objectives. Automation for common operational tasks.

What doesn't work is pretending every request is equally urgent, stuffing all workloads into one database, and assuming the cloud will fix poor boundaries.

Teams also make a strategic mistake when they treat architecture in isolation from business goals. If the product roadmap includes partner integrations, rapid market experiments, or embedded finance capabilities, the architecture needs to support that path. A useful external perspective on that connection between product expansion and platform design is this piece on implementing fintech for growth, which frames scalability as an enabler of business rollout, not just a back-end concern.

Choosing Your Architectural Blueprint

The right architecture depends less on fashion and more on product shape, team maturity, and compliance exposure.

Three patterns come up repeatedly in fintech builds: microservices, event-driven architecture, and API-first design. They overlap, and many successful platforms use all three in combination. The mistake is choosing one as an identity rather than using it as a tool.

Microservices When Domain Boundaries Are Real

Microservices work well when your business domains are distinct. Payments, onboarding, policy administration, claims intake, fraud scoring, customer communications, and reporting often evolve at different speeds and have different availability requirements.

That separation creates real business value. Teams can deploy more independently. One service can scale more aggressively than another. Sensitive domains can have tighter controls. The downside is equally real. You trade monolithic simplicity for distributed systems overhead. Observability, deployment pipelines, service contracts, and incident response all get harder.

Event-Driven Systems When Timing and Decoupling Matter

Event-driven architecture shines when one action should trigger multiple downstream processes without blocking the original user flow. A payment event can update a ledger, notify a customer, feed risk analysis, and kick off reconciliation asynchronously. An insurance claim submission can spawn document review, fraud analysis, status updates, and internal workflow routing.

That decoupling is powerful, especially for high-volume or bursty workflows. But event-driven design can become difficult to reason about if event contracts are sloppy or if there's no clear ownership of retries, ordering, and idempotency. Teams often underestimate how much design discipline this pattern requires.

If your team can't answer “what happens when the same event is delivered twice?” with confidence, you're not ready to rely on asynchronous processing for critical money movement.

API-First When Integration Is the Product Strategy

API-first design matters when the platform must integrate cleanly with banks, insurers, clinic systems, accounting software, or partner apps. In Canadian fintech, this is often the practical starting point because many products succeed by fitting into existing operating environments rather than replacing them outright.

An API-first approach forces teams to clarify contracts early. That helps with partner onboarding, internal reuse, and version control. It doesn't solve every scaling problem by itself, but it creates a structure that supports scaling later.

For teams evaluating broader architecture options, Cleffex's write-up on enterprise application architecture patterns is a useful reference point because it frames pattern choice around operating context rather than trend-following.

Architectural Pattern Comparison for Fintech

| Criterion | Microservices | Event-Driven Architecture | API-First Design |

|---|---|---|---|

| Best fit | Products with clear business domains and separate release cycles | Workflows with multiple downstream actions and bursty processing | Platforms that depend on partner integration and reusable service contracts |

| Development speed early on | Moderate. Setup overhead is higher | Moderate. Event design takes planning | Often faster for integration-heavy products |

| Operational complexity | High. More services to monitor and deploy | High. More moving parts across queues and consumers | Moderate. Contract discipline matters more than service count |

| Scaling strength | Strong for independently scaling domains | Strong for handling asynchronous peaks | Strong for ecosystem growth and partner enablement |

| Failure isolation | Good if service boundaries are clean | Good if consumers fail independently | Depends on downstream system design |

| Team skill requirement | Strong DevOps and service design capability | Strong messaging, observability, and recovery design capability | Strong API governance and lifecycle management |

| Cost profile | Can rise with service sprawl | Can rise with operational tooling and event infrastructure | Usually simpler at first, but may need deeper back-end changes later |

| Where it fails | When teams split too early and create distributed monoliths | When event ownership and replay handling are vague | When APIs are clean on the surface but backed by tightly coupled internals |

A Practical Selection Method

Architects usually get better outcomes by choosing according to business pressure.

Choose microservices when independent scaling and release autonomy are worth the operational overhead.

Choose event-driven patterns when customer experience improves by pushing expensive work off the request path.

Choose API-first design when your growth depends on external integration, channel partnerships, or internal platform reuse.

Most fintech platforms shouldn't start with maximum complexity. They should start with clear boundaries and a migration path. That gives the business room to grow without forcing the engineering team to maintain an architecture they didn't need yet.

Selecting the Right Cloud and Platform Foundation

Cloud choice isn't mainly about vendor preference. It's about how much control you need, how quickly you need to ship, and how tightly your architecture must align with Canadian operational and compliance realities.

For fintech, the platform decision usually comes down to three operating models: IaaS, PaaS, and serverless. Each can work. Each creates a different balance between flexibility, engineering effort, and operational visibility.

Where Each Model Fits

IaaS gives the most control. Teams can tune networks, operating systems, runtime behaviour, and deployment patterns in detail. That matters when you have legacy integration constraints, strict security controls, or unusual workload requirements. The trade-off is management overhead. You own more of the stack, so you also own more patching, hardening, and operational complexity.

PaaS reduces that burden. It's often a strong fit for business workflows, internal tools, and less specialised services because the platform handles more of the infrastructure management. The trade-off is less fine-grained control and occasional friction around custom networking, performance tuning, or platform-specific limitations.

Serverless is attractive when demand is uneven and speed-to-market matters. It can work well for event processing, scheduled jobs, lightweight APIs, and isolated automations. The downside appears when cold starts, execution limits, or vendor-specific patterns begin shaping the product more than the product requirements do.

What Canadian Fintech Teams Need To Account For

A key technical pattern for Canadian fintechs is autoscaled container orchestration, such as Kubernetes, combined with database replication across Canadian regions to maintain both high availability during traffic spikes and data residency compliance, as outlined in this discussion of hyperscalable fintech infrastructure.

That pattern is useful because it addresses two problems at once. First, it helps the platform absorb burst demand in APIs, fraud checks, and transaction processing. Second, it gives teams a practical way to keep regulated data handling aligned with residency and availability expectations.

A Sensible Cloud Decision Framework

When comparing AWS, Azure, and Google Cloud, most fintech buyers shouldn't ask “which is best?” They should ask a narrower set of questions.

Which provider aligns with our core workloads? If your roadmap leans heavily on containers, managed data services, and eventing, compare maturity in those areas first.

How much managed service adoption are we comfortable with? Managed databases and messaging reduce toil, but they can increase lock-in.

Where will sensitive data live and replicate? This needs a concrete answer before the architecture is finalised.

What can our team operate well? A theoretically elegant platform is a poor choice if the team can't support it under pressure.

What Usually Works in Practice

For many fintech builds, the strongest middle path is containerised services on a managed Kubernetes platform, with selective use of managed databases, object storage, secrets management, and event services. That model gives enough control for security and performance tuning without forcing teams to manage every infrastructure layer manually.

It also handles mixed workloads well. A healthcare payments platform may need strict control over protected data flows, while an insurance claim notification service may be a good candidate for serverless processing. An SMB finance product might run core transaction services in containers while using platform-native queues and scheduled jobs around the edges.

What To Avoid

Two mistakes are common.

The first is overbuilding with multi-cloud before there's a business reason. That adds cognitive and operational load quickly.

The second is underestimating platform dependency. If a product relies heavily on one provider's proprietary workflows, migration becomes harder, procurement options narrow, and negotiation power drops. Sometimes that's acceptable. It should be intentional, not accidental.

Integrating Security and Compliance From Day One

Security is often discussed as if it competes with speed. In fintech, the opposite is usually true. Weak controls slow delivery later because every release triggers more review, every incident adds more oversight, and every manual check becomes a scaling problem.

A platform that grows without strong controls doesn't become scalable. It becomes fragile at a larger size.

Fraud Pressure Changes What Scale Means

In Canada, the risk picture is tightening. FINTRAC has reported a sharp rise in suspicious transaction reports, and the Canadian Anti-Fraud Centre reported over $638 million in fraud losses in 2023, according to this discussion of fraud, AML pressure, and scalable controls. For architects, that shifts the target. Scale can't just mean handling more transactions. It also has to mean handling more risk without proportionally increasing manual intervention.

That's why effective fintech platforms build controls directly into transaction flows.

Real-time risk scoring helps decide when to allow, delay, or escalate activity.

Step-up verification introduces extra checks only at higher-risk moments.

Case-management automation routes suspicious activity into structured workflows instead of burying analysts in email and spreadsheets.

Audit-ready event trails preserve evidence for investigations and reporting.

Security Patterns That Support Growth

The best security controls are often invisible to low-risk users and unavoidable for high-risk behaviour.

A practical baseline usually includes tokenised handling of sensitive data where possible, strong identity and access management, encryption in transit and at rest, secrets management, least-privilege service access, and environment separation. But controls only become scalable when they're connected operationally. Fraud signals should affect authentication. Device anomalies should inform transaction review. Manual decisions should feed back into risk logic instead of living in isolated tooling.

Good fintech security adds friction selectively. It removes friction for legitimate users by concentrating scrutiny where the risk actually is.

PCI, Payment Scope, and Operational Reality

Payment products add another layer because the compliance scope expands quickly when card data, merchant onboarding, and transaction handling aren't designed carefully. Teams often discover too late that architecture decisions changed their compliance burden.

For payment-heavy products, a grounded resource on managing merchant PCI levels is worth reviewing early, especially when deciding how much card-related scope the platform should absorb directly.

For broader implementation planning, Cleffex has also published a practical overview of fintech compliance solutions, including how development teams can structure controls so compliance doesn't remain a separate afterthought.

What Doesn’t Scale

Some anti-patterns show up repeatedly:

Late-stage compliance retrofits that force redesign after core workflows are already live

Shared privileged access across teams and environments

Manual spreadsheet-based review queues for suspicious activity

Single approval bottlenecks for onboarding, fraud operations, or exception handling

Security controls isolated from product telemetry, which makes incident response slower and less reliable

The business consequence is predictable. Every new customer segment, partner integration, or feature launch becomes harder because the control model wasn't built to expand.

The better approach is to treat security architecture as product architecture. In fintech, trust, throughput, and compliance are tied together. You can't scale one sustainably without the others.

Real-World Scalable Fintech Applications

The most useful way to judge architecture is to look at what it enables in the field. Different industries need different forms of scale. Insurance needs burst handling and workflow orchestration. Healthcare needs secure interoperability and careful data access. SMB platforms need low-friction rollout, manageable cost, and simple operations.

Insurance After a Claims Surge

An insurer doesn't experience demand as a smooth upward line. Demand arrives in waves. A weather event, a policy renewal cycle, or a broker campaign can trigger a sudden jump in claims intake, document uploads, customer notifications, and internal review tasks.

A scalable approach usually combines a stable customer-facing API layer with asynchronous claim-processing pipelines. The intake experience stays responsive because expensive downstream tasks don't sit on the same request path. Document processing, fraud screening, triage, and adjuster assignment can all run independently with clear retry behaviour.

What doesn't work is forcing every claim action through one synchronous workflow. That design looks simple until the queue forms in the wrong place and customers start resubmitting forms because the interface appears frozen.

Healthcare Payments and Connected Data Flows

Healthcare organisations often need fintech capability without looking like a fintech company. Clinics, health-tech startups, and care networks may need payment plans, billing automation, disbursement flows, or reimbursement logic while also handling strict privacy expectations.

In this setting, API-first architecture pays off. Patient-facing applications, internal billing platforms, insurer connections, and partner systems can exchange data through explicit contracts instead of brittle point-to-point integrations. Security boundaries are easier to define, and changes are easier to test.

This is also where AI-assisted support can reduce operational load if it's implemented carefully. For teams considering conversational tools in financial workflows, SupportGPT's guide to banking AI is a useful read because it focuses on practical support and service use cases rather than novelty.

SMB Finance Products That Need To Launch Without Overbuilding

Small and mid-sized business finance products often face a different constraint. They need to get to market quickly, but they can't afford a platform that becomes expensive to operate six months later.

For these products, a compact architecture often wins at the start. A clean API layer, managed services that reduce toil, event handling for non-blocking work, and strong observability can support growth without introducing unnecessary service sprawl. Cleffex Digital Ltd is one option in this space for custom fintech software development, particularly when a business needs custom integrations with core systems and third-party services rather than an off-the-shelf product.

The key is resisting premature fragmentation. A small team doesn't need twenty services to prove a business model. It needs clean boundaries, a sensible data model, and a migration path when volume or complexity justifies deeper separation.

Scale Also Means Inclusion in Canada

A Canadian definition of scale has to go beyond urban, always-online usage. FCAC's survey found that 90% of Canadians had some form of online banking, but a more useful angle on scalability is hybrid models that also serve offline-first populations, as discussed in this piece on connecting underserved communities to financial technologies.

That matters for rural communities, older adults, lower-income users, and people who don't move comfortably through app-first onboarding flows.

Practical design responses include:

Assisted onboarding through call centre or branch-adjacent workflows

Low-bandwidth interfaces that don't assume perfect connectivity

Multilingual support paths for identity verification and customer help

Hybrid operating models that allow digital continuation after non-digital entry points

For fraud-heavy environments, these inclusion models need strong back-end intelligence. A platform can expand reach without weakening controls if it combines alternative customer journeys with strong monitoring and escalation logic. Cleffex's article on AI-powered fraud detection in fintech is relevant here because it ties detection capability to real operational workflows, not just model selection.

The strongest fintech platforms don't just scale up. They scale across different user realities.

Measuring Success and Planning Your Next Steps

A scalable platform should be measurable in business terms, not just technical ones.

Uptime matters, but it's only part of the picture. Leadership teams need to know whether the platform stays responsive during peak periods, whether control costs stay contained, whether fraud and compliance handling remain manageable, and whether new product changes can ship without destabilising core services.

The KPI Set That Usually Matters

Use a compact scorecard that combines product, operations, and risk.

Transaction latency under load shows whether critical journeys remain usable when demand spikes.

Authorisation and processing success rates reveal whether integrations and downstream dependencies are holding up.

Reconciliation lag tells finance how quickly the platform closes the loop operationally.

Cost per transaction or per active workflow helps identify whether scale is improving economics or just increasing spend.

Time-to-market for new features shows whether the architecture is enabling delivery or obstructing it.

Manual review volume reveals whether compliance and fraud controls are becoming operational bottlenecks.

Incident recovery time indicates whether failures are isolated and recoverable or broadly disruptive.

A Practical Readiness Checklist

Before committing to a build or major rebuild, ask these questions:

Are the most important business domains clearly separated?

Can high-cost background work run outside the user request path?

Does the platform have a credible data residency and availability plan?

Are fraud, verification, and audit controls built into workflows instead of layered on later?

Can the team observe bottlenecks across APIs, queues, databases, and external services?

Will the chosen cloud and service model match the team's operating capability?

If the answer to several of these is no, the issue usually isn't a missing tool. It's that the platform needs stronger design decisions before more features are added.

What Good Next Steps Look Like

The best fintech programmes don't start by trying to perfect everything. They start by identifying the highest-risk customer journeys, the biggest operational bottlenecks, and the decisions that are expensive to reverse later. Then they sequence the work. Domain boundaries first. Data strategy early. Security architecture from the beginning. Automation where manual effort will compound fastest.

That's the practical path to scalable fintech solutions. Not bigger infrastructure alone. Not trend-driven architecture. A system that can grow in users, transactions, integrations, and regulation without losing control of cost, speed, or trust.

If you're planning a fintech platform for insurance, healthcare, SMB services, or a regulated enterprise product, Cleffex Digital Ltd can help assess the architecture, cloud model, and compliance design needed for a scalable build. The useful starting point is usually a working session around your core workflows, integration dependencies, and risk constraints, so the solution fits your business model instead of forcing your roadmap into a generic template.