More than 85% of financial institutions are actively using AI, and more than 40% are using Generative AI. That changes the conversation. AI-powered financial services are no longer a lab project for global banks. They're part of day-to-day operations.

For Canadian businesses, that matters well beyond banking. Insurers need better claims review. Healthcare groups need cleaner billing workflows. E-commerce teams need sharper fraud controls and faster cash-flow visibility. Mid-sized enterprises need finance operations that don't stall on manual reviews, document handling, or fragmented systems.

The practical question isn't whether AI belongs in finance. It's where it creates value first, which controls must be built around it, and how to implement it without creating a compliance problem or an expensive pilot that never reaches production.

The New Standard in Financial Operations

Canadian firms that still treat AI as optional are drifting away from the operating model now taking hold in finance. As noted earlier, adoption has moved well beyond pilots. The practical shift is clear. AI is being built into fraud monitoring, risk review, and back-office workflows that used to depend on manual triage.

That change reaches any business handling payments, lending, claims, subscriptions, receivables, onboarding, or regulated customer records. A finance team that reviews invoices one by one, checks onboarding documents manually, or relies on fixed rules for exceptions is usually working with slower cycle times, higher labour costs, and less consistent control. Competitors are using pattern detection and workflow automation to route routine cases automatically and send only the ambiguous ones to staff.

Where the pressure shows up first

Cost usually gets attention first. Then speed. Then control.

I see the same pattern across Canadian organisations. An SMB feels it when payment exceptions stack up at month-end and cash application slips. A healthcare operator feels it when billing teams spend hours reconciling codes, remittances, and supporting documents. An insurer feels it when fraud review turns into a backlog instead of a control function. The surface problem changes by industry, but the root issue is the same. Teams are making high-volume financial decisions with systems built for simple automation rather than adaptive analysis.

Architecture matters as much as the model you choose. Companies that buy an AI feature before sorting out data access, system integration, and workflow ownership often add one more disconnected tool to an already messy stack. If you're comparing packaged platforms with custom development, this guide on choosing the right fintech tech stack is a useful starting point because it frames the technical decisions that shape cost, security, and maintainability.

For Canadian firms, the design question is broader than tooling. Data residency, auditability, model oversight, and integration with bank and payment infrastructure all affect what can go into production. Teams planning around account connectivity and transaction data should also review Canada's open banking solutions and what they mean for implementation.

AI works in finance when it is tied to a specific operational bottleneck, clear ownership, and controls that satisfy audit and compliance requirements.

What leaders should expect now

The strongest use cases today are operational, measurable, and close to existing workflows:

Faster reviews: Document-heavy approvals move with less manual sorting and fewer handoffs.

Better exception handling: Staff spend less time on routine cases and more time on cases that need judgment.

Stronger controls: Suspicious activity is flagged earlier, with a clearer review trail.

Cleaner service delivery: Customers get quicker answers on onboarding, claims, billing, and account support.

The new standard in financial operations is straightforward. Finance teams are expected to process more volume, with better accuracy, tighter controls, and no proportional increase in headcount. AI can help deliver that. Only if it is set up around real processes, clean governance, and the regulatory conditions Canadian businesses have to handle every day.

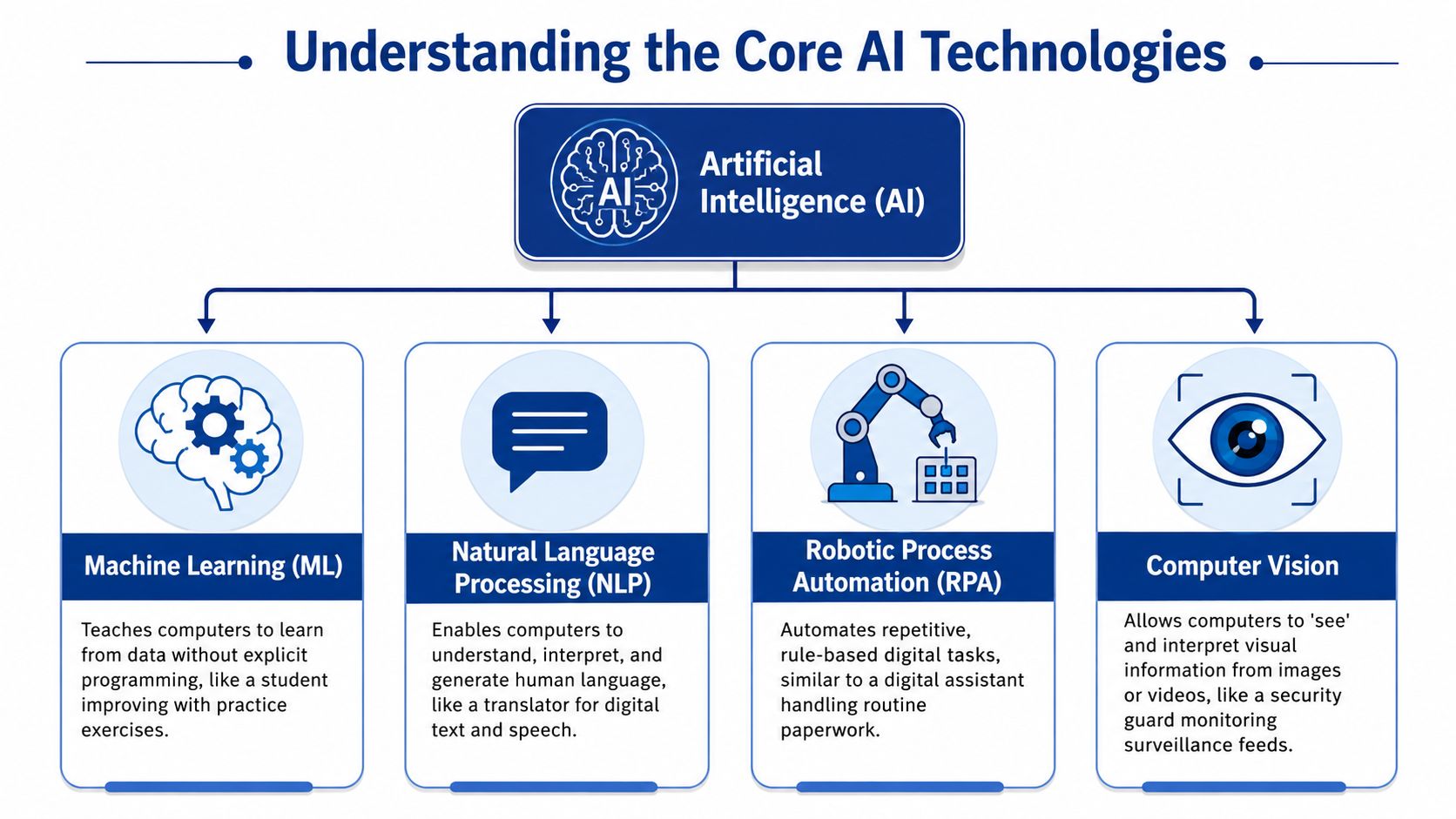

Understanding the Core AI Technologies

Most confusion around AI-powered financial services comes from using one label for several very different technologies. In practice, finance teams usually combine a few of them. Each solves a different class of problem.

Machine learning and why rules alone stop working

Machine learning is best understood as a junior analyst who improves with exposure to more examples. A traditional rules engine says, “if this condition is true, take this action.” That works for stable, predictable tasks. It breaks down when fraud patterns shift, customer behaviour changes, or the data arrives in messy formats.

A better comparison is a paper map versus a GPS. A paper map gives fixed directions. A GPS adjusts when traffic changes. In finance, machine learning does the same kind of adaptation. It identifies patterns in repayment behaviour, transaction anomalies, claim submissions, or cash-flow signals and updates how it prioritises risk.

That's especially relevant in environments with many exceptions. The more your process depends on analysts spotting subtle patterns by hand, the more likely machine learning belongs somewhere in the stack.

NLP, RPA, and Computer Vision in Real Workflows

Natural language processing, or NLP, is the layer that reads and interprets human language. Think of it as a translator that can work across contracts, emails, policy documents, customer chats, notes, and compliance records. In finance, that means extracting obligations from agreements, routing support tickets, summarising long files, or searching large document sets with plain-language questions.

Robotic process automation, or RPA, is different. It doesn't “understand” much by itself. It follows structured steps. Used properly, it handles repetitive digital tasks like moving data between systems, generating standard forms, or triggering follow-up actions after approvals. Used badly, it becomes a brittle patch over a broken process.

Computer vision lets systems interpret images and visual documents. In financial operations, that often means reading scanned forms, validating identity documents, checking uploaded evidence, or classifying paperwork before a reviewer sees it.

Here's a practical way to think about the differences:

| Technology | Best for | Weak point |

|---|---|---|

| Machine learning | Pattern recognition, scoring, anomaly detection | Needs quality data and monitoring |

| NLP | Reading and querying text-heavy content | Can misread context without guardrails |

| RPA | Repetitive, rules-based steps across systems | Breaks when process steps change often |

| Computer vision | Processing images, scans, document inputs | Depends on input quality and validation |

Where Generative AI fits

Generative AI is the newest layer many teams recognise first, but it shouldn't be the first thing they deploy everywhere. It's useful when staff need a drafting partner, coding assistant, document query interface, or case summariser. It can help produce responses, extract action items, or prepare analyst-ready outputs from large volumes of content.

The mistake is treating GenAI as a complete finance solution. It isn't. It's strongest when paired with governed data, workflow rules, and human review. Security teams should also think carefully about model access, logging, and policy controls. This overview of ISO 27001 and AI for security is a helpful reference point when building those controls into the design rather than adding them later.

For organisations preparing for broader data-sharing and ecosystem change, Cleffex's guide to Canada's open banking solutions is also worth reading because open financial infrastructure changes what AI systems can access, automate, and analyse.

The best financial AI stacks don't rely on one model. They combine prediction, language handling, workflow automation, and governance.

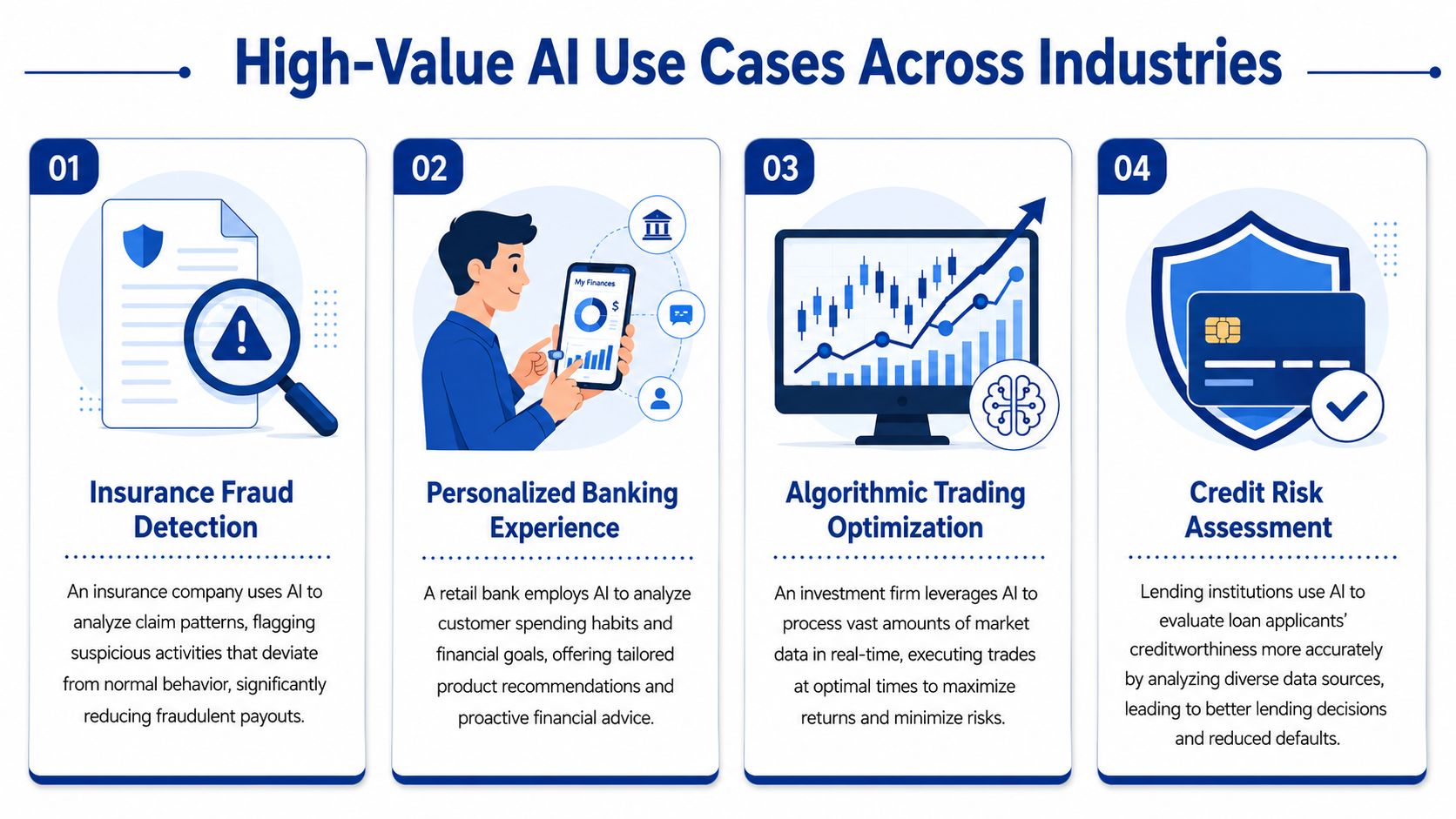

High-Value AI Use Cases Across Industries

The strongest AI programmes in finance don't begin with “let's use AI.” They begin with a blocked workflow. Claims take too long. Invoice approvals stall. Fraud losses are hard to isolate. Billing staff spend their day cleaning data instead of resolving issues. Once the bottleneck is clear, the right use case usually becomes obvious.

Insurance and financial risk operations

An insurance team processing claims often faces the same problem every finance department knows well. Most submissions are ordinary, but a small set needs deeper review. AI helps by scoring claims against behavioural and document patterns, then pushing only suspicious or incomplete files into specialist review queues.

That changes the economics of claims handling. Adjusters stop wasting time on low-risk files. Fraud teams get better triage. Customers with straightforward claims get faster responses because the queue is no longer clogged by manual first-pass review.

In broader finance operations, the pattern is similar. Transaction monitoring tools can flag unusual sequences, vendor payment systems can detect out-of-pattern invoice behaviour, and account support teams can surface risk signals before a customer issue turns into a loss event.

SMB finance teams and mid-market operations

For a small e-commerce business, the best AI use case may have nothing to do with lending or trading. It may be demand-linked cash management. If sales, refunds, supplier costs, and ad spend move quickly, finance teams need better forecasting than a spreadsheet updated every Friday.

AI can help classify spend, identify likely receivables delays, and surface inventory decisions that affect cash. It can also prioritise suspicious orders, especially where high-value transactions, new customer accounts, and delivery mismatches create fraud exposure.

Mid-sized enterprises usually see faster value in shared-service finance functions:

Accounts payable automation: AI reads invoices, matches them to purchase records, flags anomalies, and routes exceptions.

Expense and policy review: NLP checks receipts, notes, and supporting documents for missing or inconsistent information.

Collections support: Models prioritise outreach based on payment behaviour and account context.

Management reporting: GenAI can summarise trends and assemble first-draft narrative commentary for finance leaders.

Practical rule: If a process involves repetitive review, unstructured documents, and frequent exceptions, it's a strong candidate for AI.

Healthcare, automotive, and customer-facing finance

Healthcare clinics and provider groups often struggle with patient billing because records, coverage details, supporting notes, and payment follow-ups sit across multiple systems. AI can extract billing details from documents, classify claims-related correspondence, and help staff answer account questions faster. The value is operational. Fewer handoffs, fewer avoidable delays, and less staff time spent searching through fragmented records.

Automotive businesses have a different workflow, but the same logic applies. Dealerships and service networks handle financing applications, warranty paperwork, service-package pricing, and payment follow-ups. AI can pre-screen documents, identify missing items in deal files, and route customer finance cases to the right queue without making staff search manually through each submission.

A useful way to evaluate use cases is to score them on four dimensions:

| Use case | Operational pain | Data readiness | Compliance sensitivity | Likely implementation path |

|---|---|---|---|---|

| Claims review | High | Medium to high | High | Pilot with human-in-the-loop review |

| Invoice processing | High | High | Medium | Fast automation candidate |

| Onboarding checks | High | Medium | High | Controlled rollout with audit logging |

| Billing support | Medium to high | Medium | High | Start with assistive AI before automation |

The common thread is simple. High-value AI use cases in finance aren't abstract. They sit inside approval queues, exception handling, fraud review, onboarding, and billing operations where staff already know the pain.

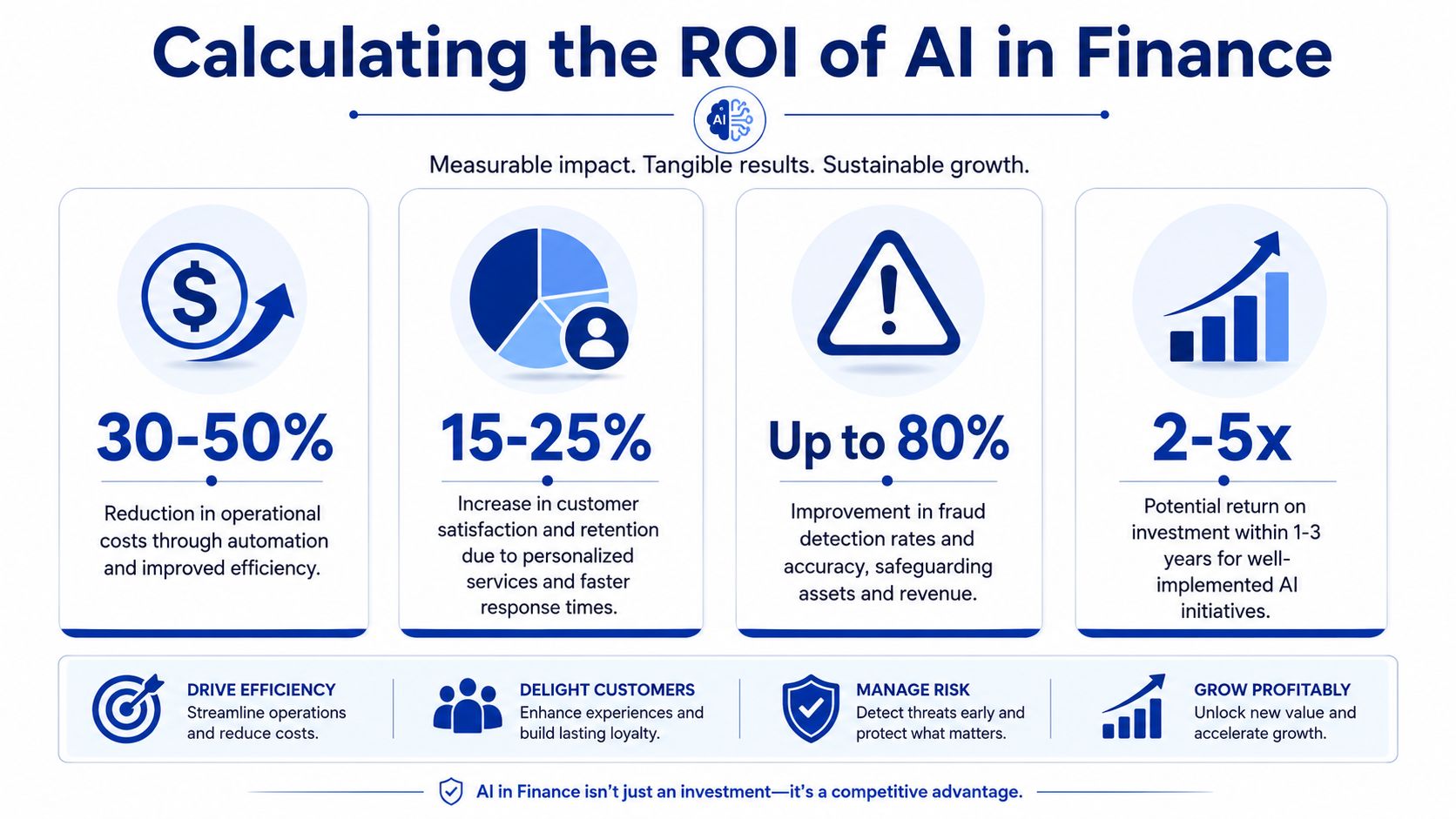

Calculating the ROI of AI in Finance

AI projects fail financially when leaders can't connect the model to an operational metric. “Better insights” won't survive budget review. A stronger business case starts with a process that already has visible cost, delay, leakage, or compliance burden.

The most credible ROI discussions in finance come from a small number of measurable categories. Risk teams look for fewer missed anomalies and better prioritisation. Operations teams look for reduced manual effort. Customer-facing teams look for faster onboarding or cleaner service resolution.

The metrics that matter

In Canadian finance, there are a few data points worth paying attention to. AI-powered systems have shown a 35% improvement in proactive risk management over traditional models, and some Canadian banks have reported a 40% reduction in client verification costs through AI-driven onboarding tools. Those are the kinds of outcomes that justify investment because they tie directly to workflow performance and cost control.

The challenge is translating that logic into your own environment. Don't ask whether AI will “transform finance.” Ask whether it will improve one expensive workflow enough to pay for itself.

A practical scorecard usually includes:

Manual review volume: How many items can be auto-classified, pre-filled, or routed without staff intervention?

Cycle time: How long does onboarding, approval, reconciliation, or exception handling take before and after deployment?

Loss prevention: Are you catching more suspicious behaviour earlier?

Unit economics: What happens to the cost per verification, invoice, claim review, or account case?

Quality and rework: Do staff have to correct outputs constantly, or are they spending time only on exceptions?

Build the business case from one workflow

The fastest way to lose confidence in an AI initiative is to spread it across too many objectives. Start with a single finance process and build a baseline.

For example, if onboarding is the target, measure current staffing effort, turnaround time, abandonment points, and remediation effort for incomplete files. If accounts payable is the target, track the volume of invoices, exception rates, average approval time, and time spent matching records across systems.

Then compare approaches:

| Approach | What you can expect |

|---|---|

| Rules-only automation | Good for stable, repetitive tasks, poor with messy inputs |

| Assistive AI | Staff move faster with summaries, extraction, and recommendations |

| Decision-support AI | Better for prioritisation, scoring, and anomaly detection |

| End-to-end automation | Highest upside, but only when governance and exception handling are mature |

Teams that need a faster market scan before building internally can review specialist directories, such as AI tools for finance. The key is to use them as inputs to evaluation, not as substitutes for a business case.

If you can't name the workflow, the owner, the baseline cost, and the success metric, you're not calculating ROI. You're funding exploration.

Navigating Canadian Regulations and Risks

Canadian finance teams do not get to treat AI governance as a policy exercise that happens after launch. In practice, governance decisions shape model design, vendor selection, approval flows, and what can safely go live.

That pressure is higher in Canada because financial AI often sits inside regulated workflows. Lending, onboarding, fraud review, claims handling, treasury forecasting, and service operations all raise questions about privacy, explainability, recordkeeping, and fairness. A model that performs well in a demo can still fail internal risk review if no one can explain its inputs, approval logic, or escalation path.

The compliance issues that deserve attention

Four issues usually surface first.

Data handling: Customer and financial data needs clear rules for collection, storage, access, residency, and retention.

Model explainability: Staff must be able to explain why a transaction was flagged, a file was prioritised, or an application received a higher-risk score.

Bias and fairness: Alternative-data models can expand access, but they can also carry historical patterns that disadvantage certain groups.

Operational accountability: A named owner should control thresholds, exception rules, overrides, and incident response.

Bias deserves more attention than it often gets. In Canadian credit and insurance contexts, weak testing can create uneven outcomes for newcomers, Indigenous communities, and lower-income applicants whose records do not match traditional scoring patterns. That is not only a legal or reputational problem. It directly affects approval quality, dispute volumes, and customer retention.

Governance that supports production use

Good governance supports delivery. It defines what the model may do, what data it may use, when a human review is required, and how decisions are challenged or reversed.

For finance teams, that usually means setting controls in five places:

Use-case boundaries: Define whether the system assists staff, recommends an action, or influences a decision.

Input controls: Approve data sources in advance and prevent unapproved mixing of customer, behavioural, or third-party data.

Bias and drift testing: Test before launch, then retest on a schedule tied to model risk and business impact.

Human review rules: Require manual review for adverse actions, high-value transactions, low-confidence outputs, or edge cases.

Customer remediation: Keep a clear path for disputes, corrections, and explanation requests.

I have seen teams slow projects down by trying to govern every possible future use case. The better approach is narrower. Set controls around the workflow in scope, document decision rights, and log every override from day one. That gives compliance, risk, and operations a shared record of how the system behaves in production.

For regulated teams that need a practical reference, Cleffex's guide to fintech compliance solutions for Canadian financial operations connects policy requirements to delivery decisions such as hosting, audit trails, access controls, and vendor review.

Fairness in financial AI shows up in daily operations. It affects who gets approved, which cases are escalated, how disputes are resolved, and whether staff can give a customer a clear reason for the outcome.

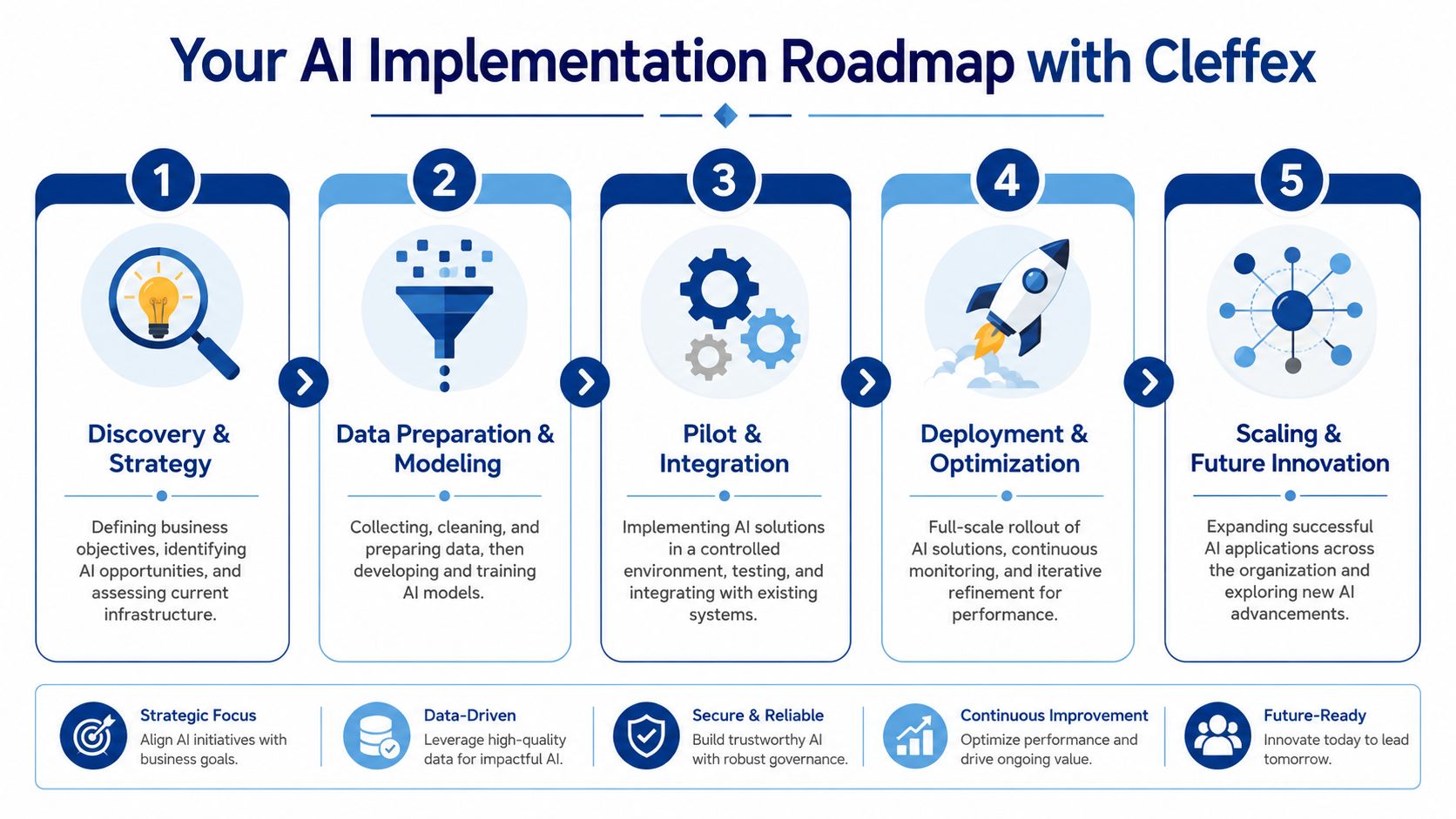

Your AI Implementation Roadmap with Cleffex

Most finance leaders don't need a grand AI programme on day one. They need a delivery path that reduces risk while proving value quickly. The strongest implementations usually move in phases, with each phase answering a specific question before the next one begins.

Phases one and two

Discovery and strategy come first. Teams identify one finance workflow worth improving, define the owner, audit the available data, and decide whether the first release should assist staff or automate part of the process. At this stage, leaders should also decide what success looks like operationally. Faster reviews, cleaner onboarding, lower handling costs, or stronger fraud escalation.

Data preparation and modelling come next. This stage is often underestimated. Finance data sits across ERP systems, CRMs, payment platforms, document repositories, and email trails. Before any model delivers value, teams need to clean records, label examples, resolve access issues, and map where outputs will return to the workflow. If the data foundation is weak, even a good model will perform badly in production.

Phases three and four

Pilot and integration should happen in a controlled environment. The point of the pilot isn't to impress stakeholders with a demo. It's to test the model against real process friction. Does it classify correctly? Does it reduce handling time? Do reviewers trust it? Can it integrate cleanly with the systems staff already use?

Deployment and optimisation begin only when the workflow, controls, and exception paths are clear. Monitoring matters here. Teams should watch where the model struggles, where staff override it, and whether outputs remain consistent as input patterns change. Production AI in finance isn't “launch once and move on.” It needs tuning, governance review, and operational ownership.

Phases five and partner selection

The final phase is scaling and future innovation. Once one use case works, organisations can extend the pattern into related workflows. A successful onboarding model can lead to better document intake. A strong invoice-processing system can support broader finance automation. A fraud triage model can provide stronger support and investigation workflows.

When choosing an implementation partner, look for a team that can do more than train a model. They should be able to work across product design, integration, cloud architecture, workflow mapping, security, and compliance constraints. That's especially important in Canada, where organisations often need custom delivery rather than rigid software that assumes a generic operating model.

A sensible evaluation checklist includes:

Workflow understanding: Do they understand lending, claims, billing, onboarding, or finance operations in practical terms?

Integration capability: Can they connect with your ERP, CRM, document systems, and support tools?

Governance maturity: Do they design for logging, review thresholds, and explainability?

Delivery method: Can they pilot quickly, learn from real users, and adapt without locking you into a brittle scope?

For a broader market view, Cleffex's article on AI adoption in Canadian enterprises adds useful context on how organisations are moving from pilots to scaled implementation.

The Future of Your Business Is Intelligent

AI-powered financial services are becoming part of the normal business infrastructure in Canada. Not because the term is fashionable, but because finance teams need better ways to handle risk, documents, exceptions, onboarding, billing, and customer-facing decisions without adding endless manual review.

The practical path is clear. Start with one constrained workflow. Choose the right mix of machine learning, NLP, RPA, computer vision, or Generative AI. Define success in operational terms. Build governance in from the start. Scale only after the first use case proves that it works in the operational environment your team operates in.

The firms that benefit most won't be the ones that buy the most AI tools. They'll be the ones that connect AI to actual financial outcomes, staff workflows, and Canadian compliance requirements.

If your organisation is looking at finance transformation now, the opportunity isn't to copy what large banks are doing. It's to build the specific capabilities your business needs, with enough control to trust them in production.

Cleffex Digital Ltd helps Canadian businesses design and build secure, practical AI solutions for finance, operations, and regulated workflows. If you're exploring automation in onboarding, fraud controls, billing, claims, or document-heavy financial processes, connect with Cleffex Digital Ltd to discuss a customised implementation strategy.