Canadian businesses reported over CAD $638 million in fraud losses in 2024, with cases continuing to rise year over year. For an SMB, that is not abstract market data. It shows up as chargebacks, lost inventory, manual review time, blocked payouts, and customer support work after a bad transaction slips through.

Many Canadian small and mid-sized businesses still assume machine learning fraud detection is built for banks, large marketplaces, or payment processors with dedicated data teams. In practice, a first fraud system can start much smaller. The goal is to make better payment decisions with the data you already have, the staff you already employ, and a budget that makes sense for your transaction volume.

A useful first setup usually has three jobs. Stop obvious abuse. Send uncertain cases to review. Learn from confirmed outcomes so decision quality improves over time.

That approach matters because fraud control is a business process, not just a model. If the system blocks too much, revenue drops and support tickets rise. If it lets too much through, chargebacks and operational losses climb. For Canadian SMBs, the right design is usually a layered system that combines gateway controls, a small set of well-maintained rules, and machine learning where it can reduce review effort or catch patterns rules miss.

The companies that get this right do not start with complexity. They start with clear loss targets, a realistic review workflow, and data they can trust.

The Rising Tide of Digital Payment Fraud

Card-not-present fraud is now a routine operating risk for Canadian businesses that accept payments online. As noted earlier, the pressure is rising across e-commerce, subscriptions, online booking, invoice payments, and app-based billing. For a small or mid-sized company, the problem usually shows up before anyone labels it "fraud strategy." It appears as chargebacks, missing inventory, payment disputes, account takeover complaints, and staff spending hours reviewing edge cases.

Online payments also remove several checks that help in person. A cashier can compare the card, the customer, and the purchase in real time. Your website cannot. It sees the payment request, checkout data, and whatever device, identity, and behavioural signals you collect.

Fraud rarely starts with a dramatic breach. It starts with ordinary process gaps that a criminal can test cheaply and repeat at scale.

A junior support agent approves a $2,000 order to a first-time customer because AVS passed, even though the IP geolocation points to another country, the shipping address changed twice in ten minutes, and the order contains high-resale items.

A returning customer account gets taken over after a password reset as the next order ships to a freight forwarder, uses overnight delivery, and adds a new card, but the team treats it as low risk because the account is three years old.

An accounts receivable clerk accepts an urgent payment update by email and sends a new invoice link without confirming the request through the customer's usual contact. The payment arrives, but the request came from an impersonated domain.

The payment gateway's default fraud filters stay in place for months even after the business changes products, average order value, and customer mix. The controls were set for launch, not for current risk.

These are common SMB failure points because fraud ownership is often split across finance, support, e-commerce, and operations. No single team tunes rules, reviews outcomes, or closes the loop after a chargeback lands.

Identity checks matter here too, especially for firms that onboard merchants, tenants, vendors, or business customers. A practical starting point is mastering KYC and KYB, then applying those checks where they reduce account takeover, synthetic identities, and payment abuse without creating too much friction for legitimate customers.

A first fraud system does not need enterprise tooling or a data science team. For many Canadian SMBs, a useful version is a layered setup: gateway controls for obvious abuse, a small rule set tied to real loss patterns, and machine learning added only where it reduces manual review or catches behaviour your rules miss. That keeps cost aligned with transaction volume and gives the business a way to improve decisions without building a bank-grade platform on day one.

Assessing Your Risk and Defining Your Strategy

A fraud system usually fails long before model selection. It fails when the business hasn't defined what it's protecting, where attacks enter, and which decisions need to happen in real time.

Canadian businesses have good reason to treat this as a business risk, not just an IT issue. A Payments Canada study reported that 20% of businesses experienced fraud incidents, compared with 13% of consumers, and the most common business threats were impersonator scams at 25%, intercepted e-Transfers at 22%, and fraudulent credit card charges at 20%, as covered by Insurance Business Canada's summary of the study.

Map the transaction path first

Take one payment journey and write it out plainly. Don't start with software. Start with process.

A useful map includes:

Where the transaction begins

Website checkout, payment link, subscription renewal, mobile app, invoice portal, phone order, or finance desk.What data you collect at that moment

Billing details, shipping details, customer account age, device clues, purchase history, payment method, order contents, IP-derived location, or login state.Who can intervene

Gateway rules, customer service, finance staff, fraud analyst, store manager, or nobody.What the final decisions are

Approve, decline, hold for review, request another verification step, or cancel fulfilment.

Most SMBs discover the same issue during this exercise. They have more fraud signals than they realised, but those signals are spread across the commerce platform, CRM, payment gateway, ERP, support desk, and email workflows.

Build a simple fraud profile

You don't need a thesis. You need a shortlist of failure patterns your team can act on.

A simple fraud profile often includes:

High-risk order scenarios such as first-time customers buying resellable goods with rush shipping

Account behaviour changes like a quiet account suddenly changing contact details and payment method

Payment anomalies such as repeated failed attempts followed by a successful one

Operational weak points including staff approving exceptions by email or chat

Settlement and refund gaps where refunds can be issued before proper verification

Businesses that do this well don't ask, “How do we stop all fraud?” They ask, “Which transaction types can hurt us fastest, and what signals do we already have to interrupt them?”

Identity checks matter more than many teams think

Fraud detection gets stronger when identity controls are tied to the payment flow. If your business is still treating customer verification, business verification, and transaction monitoring as separate projects, that separation creates blind spots.

For teams tightening account onboarding and counterparty checks, this guide to mastering KYC and KYB is useful because it shows how verification discipline supports downstream payment controls.

Set goals your team can operate

Good goals are operational. “Use AI to stop fraud” isn't a goal. “Reduce manual uncertainty at checkout” is closer. So is “flag suspicious transactions before fulfilment” or “route risky payment events into a review queue with clear reasons”.

Use goals that force trade-off decisions:

| Decision area | Low-friction choice | High-control choice |

|---|---|---|

| Checkout approvals | Approve more and review less | Hold more edge cases for review |

| Account changes | Allow immediate updates | Challenge risky changes with extra verification |

| Refunds | Fast customer service flow | Controlled release with validation |

| Staff workflow | Decentralised approvals | Central ownership of fraud decisions |

That strategy work matters because it tells you which detection method to use, and where.

Choosing Your Detection Methods from Rules to AI

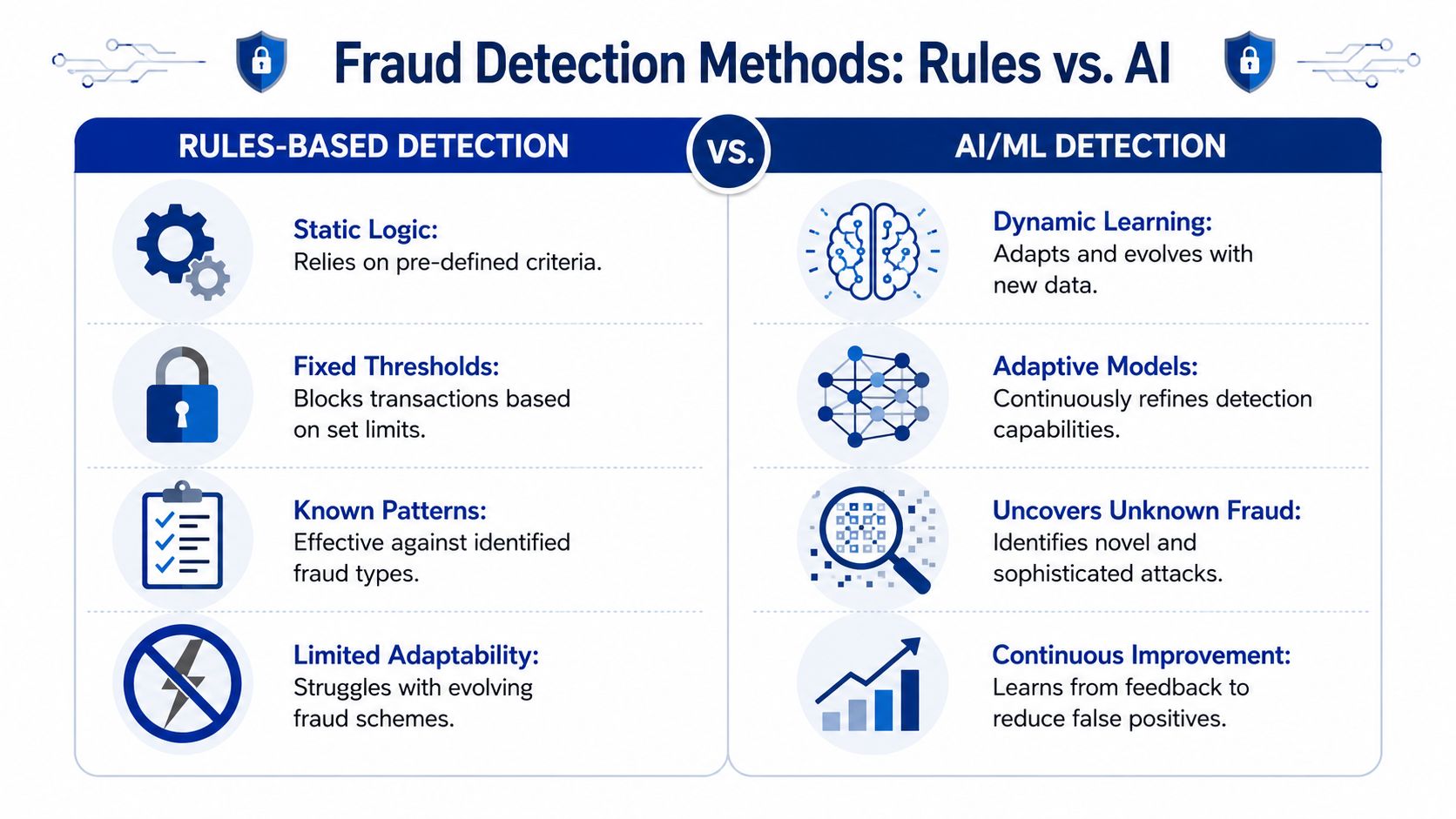

Most first-generation fraud stacks start with rules. That's sensible. Rules are fast, explainable, and easy to deploy. If a transaction comes from a blocked country, fails an address check, or hits a velocity threshold, the system can react immediately.

Rules also break down quickly. Fraudsters adapt to fixed thresholds, and honest customers don't behave in neat patterns. That's where machine learning becomes valuable. It doesn't replace rules. It sits on top of them and finds combinations a human wouldn't write by hand.

What rules do well

Rules are best when the signal is obvious, and the business rationale is clear.

Examples include:

Velocity controls that catch repeated attempts in a short window

Mismatch checks between billing and fulfilment details

Policy enforcement for gift cards, digital goods, or refund exceptions

Step-up triggers when an account suddenly changes key details

Rules are also ideal when your team needs explainability. A support lead can understand why an order was held if the trigger was explicit.

What machine learning adds

Machine learning helps when fraud hides in combinations of weak signals. One detail alone might look harmless. Several together can tell a different story.

The verified research base is strong enough to guide practical choices here. In the PMC review of fraud-detection methods, Random Forest reached up to 87.00% accuracy, and Gradient Boosting Trees reached 86.23% in comparable Australian datasets; the paper also highlights a common implementation problem: fraud data is imbalanced, so methods such as SMOTE are used to improve reliability and sensitivity.

That matters for SMBs because it points to a realistic path. You don't have to begin with the most advanced deep neural architecture. Tree-based models are often easier to implement, easier to explain, and more forgiving when your data is imperfect.

If your team is still sorting out terminology, this overview of deep learning and machine learning differences is worth reviewing before choosing a model path.

A practical comparison

| Approach | Best use | Strength | Limitation |

|---|---|---|---|

| Rules engine | Clear policy and known abuse patterns | Fast and explainable | Weak against evolving tactics |

| Random Forest | Mixed signals across many fields | Good baseline ML option | Needs labelled history |

| Gradient Boosting Trees | Pattern-heavy transaction scoring | Strong predictive performance | Tuning can get technical |

| Deep learning | Very complex behavioural patterns | Can learn subtle relationships | Usually heavier to build and operate |

What small teams should actually do

The mistake I see most often is skipping from “we need better fraud controls” to “we need a fully custom AI platform”. That's too big for most first projects.

A leaner path works better:

Start with gateway and platform controls

Use the rules your payment processor, commerce platform, or billing tool already supports. Tighten them around your known failure modes.Export decision data consistently

Keep an internal record of approvals, declines, manual reviews, refunds, disputes, and confirmed fraud outcomes. Without labels, machine learning won't help much.Add a scoring layer before full automation

A model can score risk while humans still make the final call for borderline cases.Train on your own patterns, not generic assumptions

Generic fraud tools help, but your order mix, customer base, refund patterns, and fulfilment model matter.Keep analyst feedback in the loop

Every reviewed transaction should become training input for later rule updates or model retraining.

For teams exploring how AI fits into fintech controls more broadly, this article on AI-powered fraud detection in fintech provides a useful adjacent view.

The best SMB fraud stack is usually boring in the right way. Clear rules for known threats, one sensible model for ranking risk, and a review queue that teaches the system over time.

Designing a Modern Fraud Detection Architecture

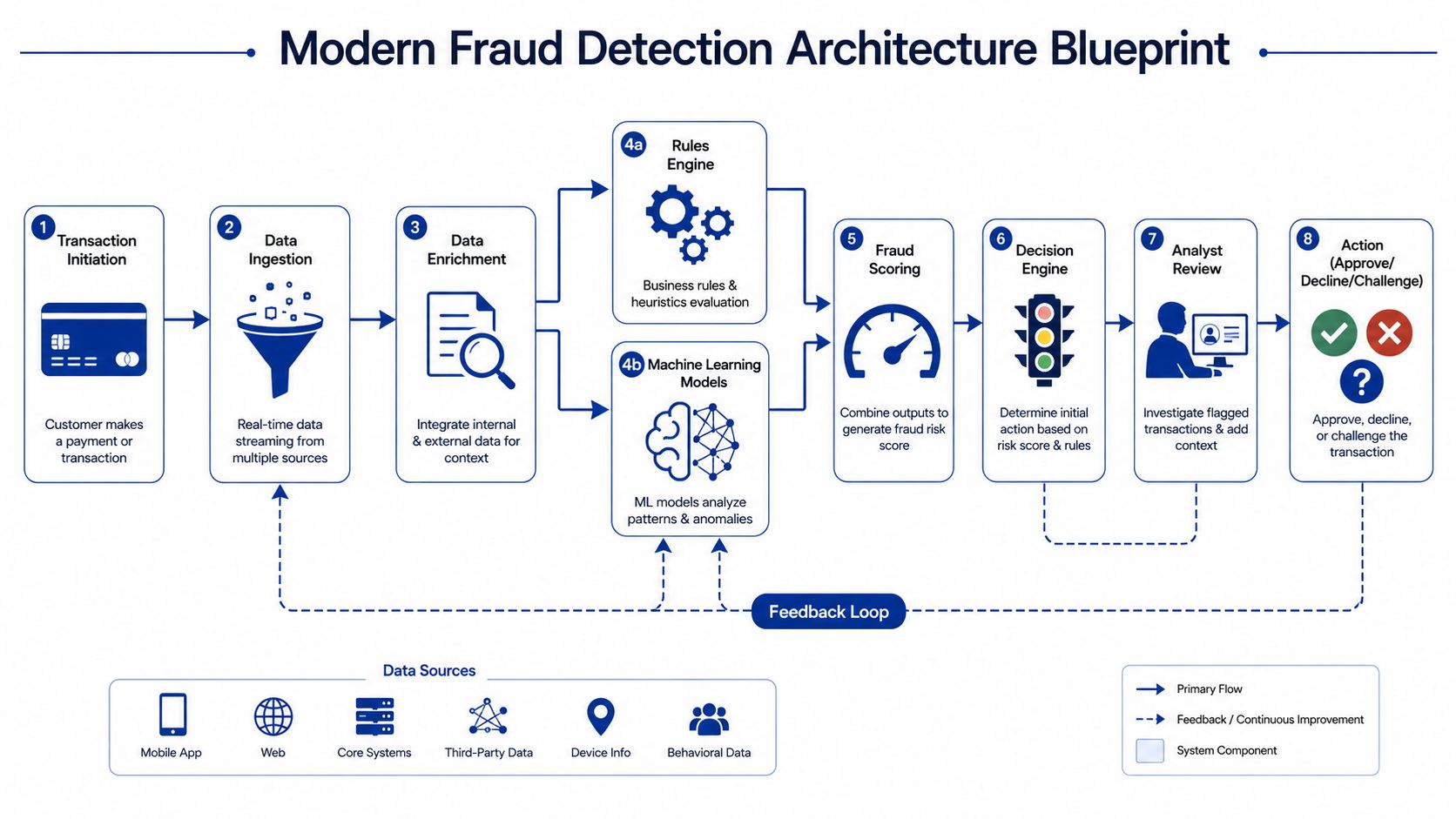

A modern fraud system should behave like a checkpoint, not a roadblock. It watches every transaction, enriches it with context, scores risk quickly, and only interrupts the customer when the evidence justifies it.

That architecture sounds expensive when described abstractly. In practice, it can be modular. A small business might connect its checkout, payment gateway, CRM, and order system into a lightweight scoring workflow. A medium enterprise might add streaming events, device intelligence, and a dedicated review console.

The core flow

At a minimum, the architecture should include these parts:

Transaction intake

The payment request enters through your website, app, invoice tool, or portal.Data enrichment

The system adds business context such as customer history, account changes, order details, and previous review outcomes.Parallel checks

Rules and model scoring run together, or in a tight sequence.Decision engine

The system approves, declines, or challenges. Borderline cases go to review.Feedback capture

Final outcomes flow back into your rules and model training set.

This model aligns with the Canadian guidance that matters most operationally. According to EY's discussion of real-time payment fraud controls in Canada, effective detection relies on AI, machine learning, and data analytics operating in real time, and success improves when institutions support real-time data sharing and automated alert generation to reduce response time.

Design for speed, not just sophistication

Many teams focus on model quality and ignore decision timing. In payment fraud detection, a good answer that arrives too late is operationally weak.

Build around these principles:

Use APIs wherever possible so checkout, payment, and order systems can share signals quickly

Separate scoring from storage so transaction decisions don't wait on heavy back-office processes

Automate alert routing so suspicious events reach the right person or queue without manual forwarding

Preserve reason codes so staff can understand why a transaction was challenged

A practical architecture also needs clear ownership. Fraud controls fail when nobody owns thresholds, overrides, and policy exceptions.

Keep the stack modular

SMBs often assume they need one large vendor to do everything. Usually they don't. A modular stack gives you room to improve one layer at a time.

| Layer | Typical purpose | Low-cost starting point |

|---|---|---|

| Payment gateway controls | Baseline filters and transaction checks | Native gateway settings |

| Business data layer | Customer and order context | CRM, commerce platform, ERP exports |

| Rules engine | Fast hard-stop decisions | Configurable logic in middleware |

| ML scoring | Risk ranking and anomaly detection | Managed cloud model service or embedded tool |

| Review console | Human decision support | Shared dashboard or ticket queue |

| Feedback loop | Continuous learning | Label outcomes in operational systems |

For businesses dealing with more complex transaction environments, especially platforms handling wallets, transfers, or digital assets, architecture choices start to overlap with designs used in crypto trading platform development, where low-latency event handling and risk controls have to work together.

If you're designing the payment layer itself, this guide to payment gateway software development is a good technical companion because gateway design and fraud orchestration are closely linked.

A strong fraud architecture doesn't have to be large. It has to be fast, observable, and easy to update when your team learns something new.

Evaluating and Operating Your System

A fraud system isn't finished when it goes live. Launch is when the substantive work starts. Fraud patterns shift, customer behaviour changes, products evolve, and staff create exceptions that gradually weaken controls unless someone reviews outcomes.

In this domain, many SMBs lose ground. They buy a tool, enable a few policies, and assume the problem is handled. But existing guidance still leaves a practical gap for smaller firms trying to build layered machine learning controls without enterprise budgets, even as under-protected smaller Canadian businesses are increasingly discussed in relation to threats described as “Maple Disruption 2025” in a Bank of Canada publication.

Measure the right things

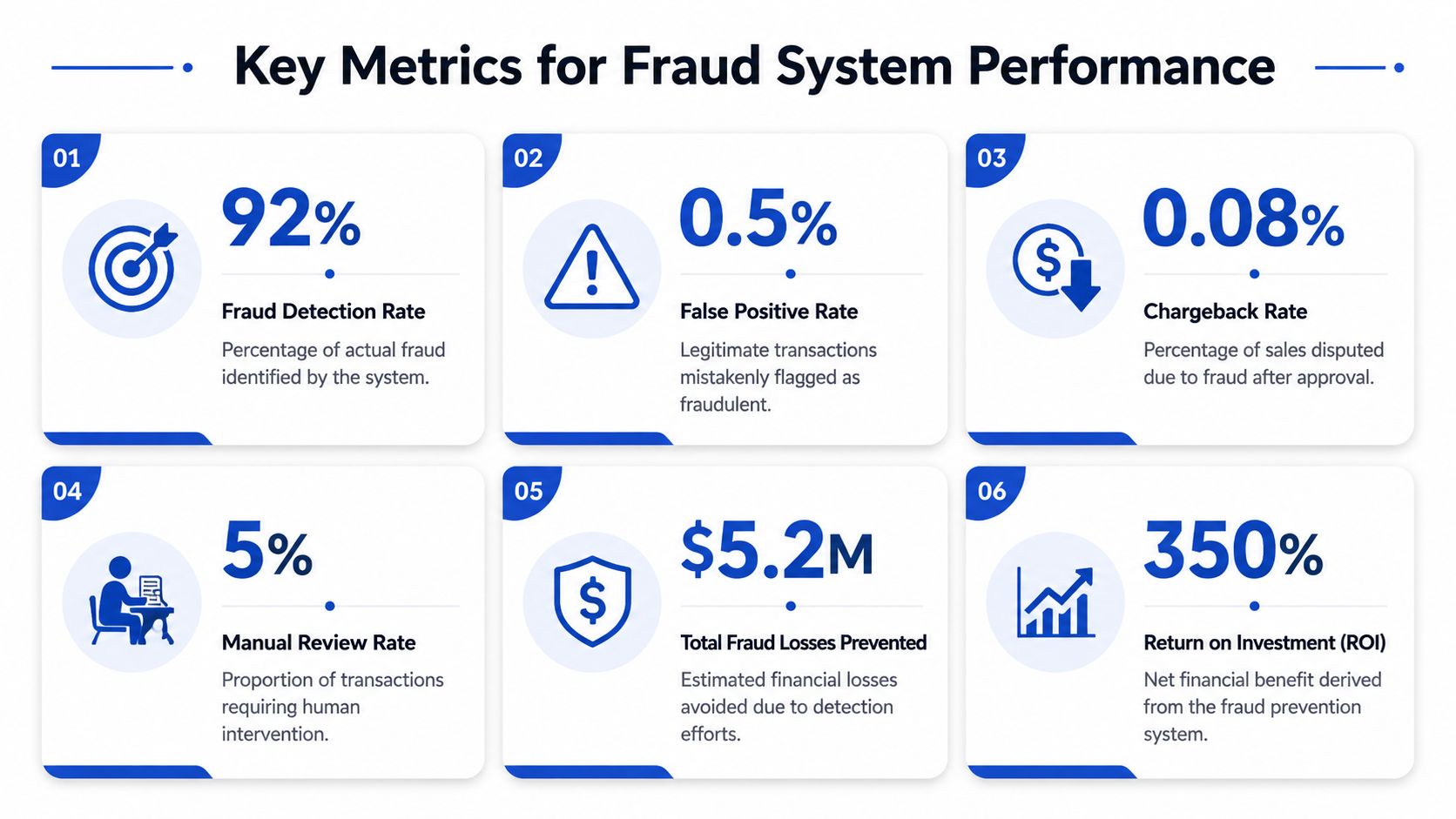

You don't need a large analytics team to run fraud operations sensibly. You do need a small set of shared metrics that both business and technical teams understand.

Focus on:

Fraud caught before completion

This shows whether the system is interrupting bad transactions early enough.False positives

These are legitimate transactions your system blocks or challenges unnecessarily. They create support tickets and lost sales.Manual review load

If too many transactions land in review, your automation isn't doing enough. If too few do, your rules may be too loose or too aggressive with auto-declines.Post-approval loss signals

Chargebacks, refund abuse patterns, and confirmed fraud after fulfilment expose blind spots.Decision explainability

Staff need to know why an alert fired. If they can't explain it, they can't tune it.

Build a review discipline

Manual review isn't a failure. It's part of the operating model. The mistake is treating review as an inbox with no learning loop.

A workable process looks like this:

Reviewers see the reason codes and supporting signals

They record the final disposition clearly

Confirmed outcomes feed rule adjustments

Labelled outcomes feed future model training

Policy owners revisit thresholds on a fixed cadence

That cadence matters. If your checkout, product mix, or customer acquisition channels change, fraud controls need to move with them.

Tune for business impact

The hardest part of payment fraud detection is balancing protection with conversion. A strict threshold catches more suspicious activity, but it can also irritate legitimate customers. A loose threshold preserves checkout flow, but more bad transactions get through.

That's why teams should evaluate controls in business language:

| Operational question | What it reveals |

|---|---|

| Are we blocking good customers? | False-positive pressure |

| Are analysts overloaded? | Poor routing or weak thresholds |

| Are confirmed fraud events repeating? | Missing rules or weak feedback loops |

| Are staff overriding alerts often? | Explainability or policy mismatch |

| Are risk checks slowing the customer journey? | Architecture or workflow friction |

One adjacent area that shouldn't be ignored is compliance. Fraud operations and data security controls overlap heavily, especially around stored payment data, access control, and system hardening. This practical PCI DSS compliance guide for businesses is useful because weak compliance hygiene often undermines fraud controls from the inside.

Teams improve fraud performance fastest when analysts, finance, operations, and engineers all review the same outcomes. Fraud isn't just a model problem. It's a process problem.

Frequently Asked Questions About Payment Fraud

What's the most cost-effective first step for a small business?

Start with the controls you already pay for. Review your payment gateway settings, tighten basic rules, require stronger verification on risky account changes, and create a manual review path for suspicious orders. Then begin storing structured outcomes. Even a modest dataset of approvals, declines, and confirmed fraud cases is more useful than buying an advanced model before your process is stable.

How does payment fraud detection relate to PCI DSS?

They're connected, but they aren't the same thing. PCI DSS focuses on protecting payment data and securing the environment around it. Payment fraud detection focuses on spotting suspicious behaviour and interrupting risky transactions. A business can be compliant and still have weak fraud decisions. It can also have smart fraud rules while storing or handling payment data badly. Mature teams treat security controls, data governance, and transaction monitoring as one operating discipline.

What should we do when fraud patterns change, and the system hasn't seen them before?

This is why layered controls beat single-method systems. Rules catch the obvious cases. Analysts investigate edge cases. Machine learning helps surface anomalies that don't match old patterns exactly. The key is feedback speed. When your staff confirms a new pattern, update rules quickly, tag the related transactions, and feed those outcomes back into later model training. Fast learning matters more than theoretical perfection.

Is a rules-only system enough?

Sometimes, for a short period. If your transaction volume is low and your fraud patterns are simple, rules may cover most immediate risk. They stop being enough when abuse starts slipping just below your thresholds or when your team spends too much time reviewing borderline cases. That's usually the moment to introduce a scoring model, not to replace all rules, but to rank risk more intelligently.

How should we think about ROI without guessing?

Keep it operational. Compare the cost of tools, staff time, and review effort against prevented losses, reduced dispute handling, cleaner approvals, and fewer bad orders reaching fulfilment. Don't reduce the question to one headline number if your business can't support that analysis yet. Early ROI often shows up first as fewer painful incidents, less staff confusion, and better control over exceptions.

Cleffex Digital Ltd helps businesses turn complex payment, compliance, and fraud-control requirements into practical software systems. If your team needs support designing a fraud-aware payment workflow, integrating risk controls into your platform, or building custom tools around secure digital transactions, explore Cleffex Digital Ltd.