Your team is likely feeling the same pressure many Canadian financial firms feel right now. Product wants a faster release cycle. Compliance wants tighter controls. IT is carrying legacy systems that were never built for mobile delivery, modern APIs, or continuous updates. Hiring locally for every specialist role takes too long, and the backlog keeps growing.

That's where financial software outsourcing becomes useful, but only when it's treated as a controlled operating model, not a shortcut. In financial services, a weak outsourcing decision doesn't just create delays. It can create audit exposure, security gaps, unclear ownership, and expensive rework. A sound one can expand delivery capacity, modernise old systems, and keep core regulatory judgement where it belongs.

Why Outsource Financial Software Now

A common starting point is a mid-sized insurer or lender with a policy administration or lending platform that still runs the business but slows every change. The internal team knows the system well, yet they're consumed by maintenance tickets, production support, and compliance changes. New work, such as partner portals, broker tools, customer self-service, or mobile apps, keeps slipping.

That's usually the point where leaders ask the wrong first question. They ask, “How much cheaper is outsourcing?” The better question is, “Which parts of delivery should stay close to the business, and which parts can a specialist partner execute faster under the right controls?”

Demand is already finance-heavy

This isn't a fringe delivery model. The global software development outsourcing market was valued at USD 534.9 billion in 2024 and is projected to reach USD 940.0 billion by 2034, while the BFSI segment held 23.7% of the market in 2024, according to software development outsourcing market figures cited by Hire With Near.

Finance sits at the centre of that demand for a reason. Banks, insurers, lenders, and wealth firms have complex integration needs, rising security expectations, and continuous pressure to deliver digital services without destabilising core operations.

The real drivers are speed, coverage, and specialist depth

Outsourcing works best when you use it to close three gaps:

Specialist capability gaps: Internal teams often don't have enough cloud engineers, QA automation specialists, DevOps engineers, business analysts, or integration developers available at the same time.

Delivery capacity gaps: Even strong in-house teams can't absorb every roadmap item, legacy upgrade, and regulatory change at once.

Execution discipline gaps: Good outsourcing partners bring repeatable delivery methods, structured QA, and release processes that many overloaded teams haven't had time to formalise.

Practical rule: Outsource to increase delivery capability, not to avoid management responsibility.

What outsourcing should actually change

A good outsourcing arrangement changes how work moves through your organisation. It introduces clearer requirements, stronger defect prevention, more formal test gates, and a more visible delivery rhythm. It can also help separate work into sensible streams, such as legacy stabilisation, API development, UX work, and regression testing.

What doesn't work is treating external engineers as an anonymous extension of a ticket queue. Financial software outsourcing fails when the client keeps architecture in people's heads, hands over unclear requirements, and expects the vendor to infer business rules from fragmented documents and old code.

If you're facing a release backlog, fragile legacy systems, and difficulty hiring for niche roles, outsourcing isn't solely about reducing spend. It's a way to regain control over delivery, provided compliance and governance are designed in before the first contract discussion.

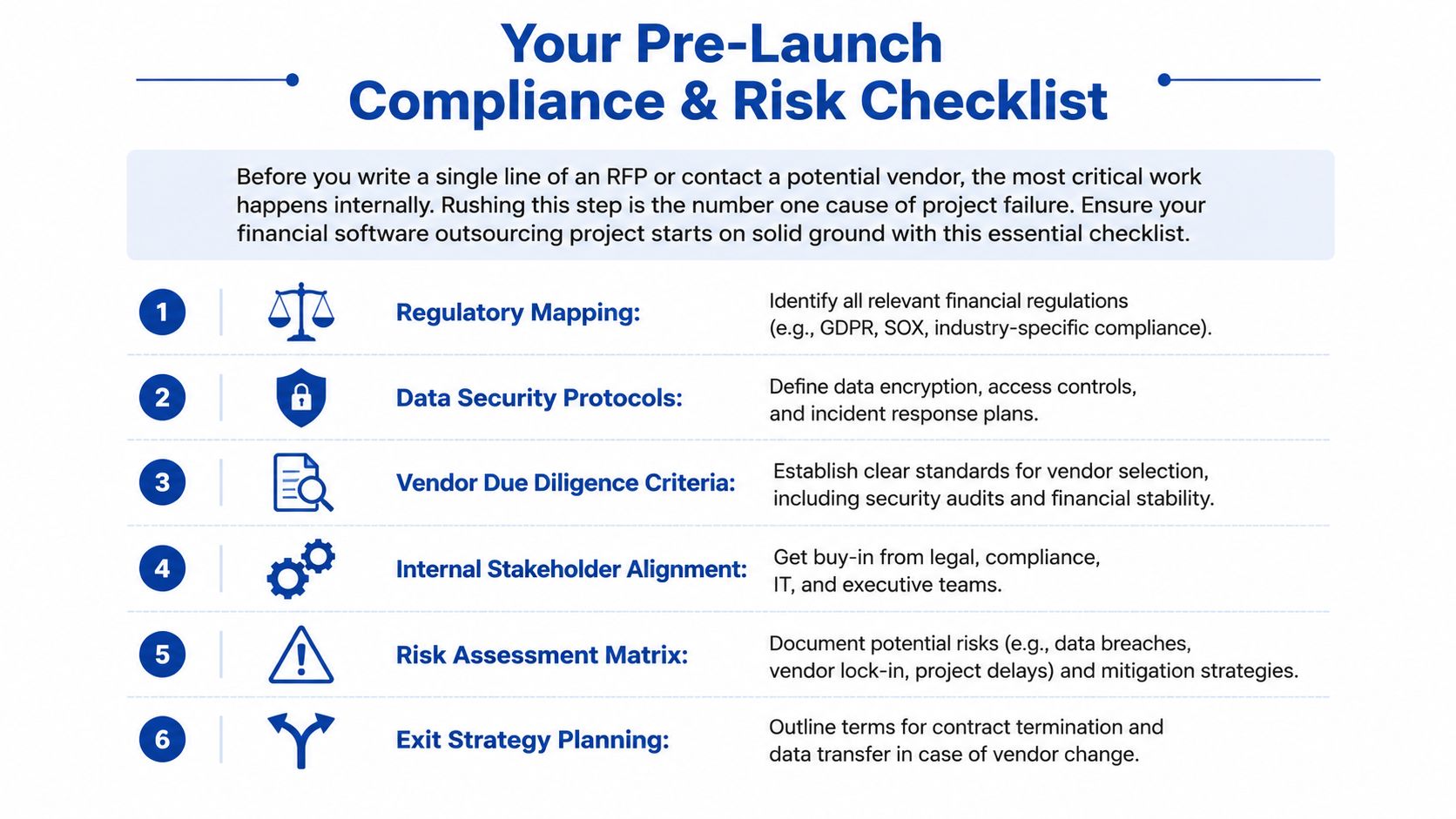

Your Pre-Launch Compliance and Risk Checklist

The most expensive outsourcing mistakes happen before vendor selection. They happen when a firm hasn't classified its data, documented its business rules, or decided which systems should never be exposed directly to an external team. In Canadian financial environments, that early discipline matters because privacy, security, and auditability aren't side concerns. They shape the delivery model.

Before you draft an RFP, freeze your assumptions and run an internal pre-flight check.

Map regulation to systems and workflows

Start with a regulatory map, not a vendor shortlist. List the systems involved, the data they process, the users who access them, and the obligations attached to each flow. For Canadian firms, that usually means understanding how OSFI expectations, PIPEDA, internal security policy, and customer consent rules affect architecture, environments, logging, and access design.

Create one working document that answers these questions:

Which applications handle customer-identifiable data?

Which integrations move data across environments or external services?

Which workflows create audit evidence?

Which modules involve core business logic that your firm considers proprietary?

If this work hasn't been done, outsourcing pushes ambiguity onto another team. That ambiguity comes back later as scope disputes, defects, and security exceptions.

A useful companion resource is this guide to fintech compliance solutions, especially if your current documentation around compliance controls is fragmented.

Classify data before you discuss delivery locations

Data classification should drive the sourcing model. Don't begin with “onshore, nearshore, or offshore?” Begin with “what data can be exposed, in what form, under what control, and by whom?”

A practical classification exercise usually separates:

Restricted financial and personal data: Customer records, transaction details, identity data, underwriting details, claims evidence, and credit information

Sensitive operational data: Internal controls, reconciliation logic, fraud rules, exception handling paths

Lower-risk engineering artefacts: UI components, test harnesses, synthetic datasets, non-production documentation

Many teams discover they don't need broad vendor access at all. They need segmented access, masked datasets, and controlled development environments.

If your delivery model requires broad production-like access just to stay functional, the architecture is usually the problem.

Define non-negotiable security controls

By the time a vendor sees your RFP, you should already know your baseline controls. Don't ask vendors what your standards should be. Tell them the minimum controls they must meet.

That baseline should cover:

Access management: Role-based access, approval paths, privileged access handling, session review

Environment separation: Development, test, staging, and production boundaries

Logging and auditability: Event logging, traceability, retention expectations, and incident evidence

Data handling: Masking, encryption requirements, secure transfer methods, retention and deletion rules

Incident response: Who gets called, in what time frame, with what evidence and escalation path

Decide what must stay in-house

Not every financial software component should be outsourced. In most first-time engagements, I advise clients to retain internal control over a few core areas:

| Keep in-house | Often suitable to outsource |

|---|---|

| Regulatory interpretation | Feature development |

| Enterprise architecture decisions | QA automation |

| Security policy ownership | Test execution |

| Production release approval | API implementation |

| Data governance | UI engineering |

That split keeps judgment close to the business while still expanding execution capacity.

Build the risk register before procurement

Your legal team, compliance lead, security lead, product owner, and engineering owner should agree on a live risk register before any vendor conversation gets serious. Include risks such as vendor lock-in, undocumented dependencies, weak handover, poor test coverage, delayed incident reporting, and unclear intellectual property ownership.

An exit plan belongs here, too. If the relationship ends, you need a defined path for source code transfer, environment documentation, credential rotation, knowledge capture, and service continuity. Teams often leave this to procurement language alone. That's not enough. The delivery team has to operationalise it.

A careful start feels slower, but it usually shortens the project. In financial software outsourcing, internal clarity is the first control, not an administrative exercise.

Selecting Your Financial Software Partner

The wrong mindset is “find a vendor who can code.” The right mindset is “choose a partner who can work inside a regulated operating model without eroding internal control.” That distinction matters more in financial services than in almost any other sector.

A polished sales process doesn't tell you much. You need evidence that the partner can handle ambiguity, document decisions, respect governance, and work with your people without displacing business knowledge.

Why the hybrid model is usually safer

One of the most useful data points for Canadian firms is this: 68% of financial software projects fail due to cultural misalignment and loss of in-house knowledge, and firms using a hybrid model with 30% senior in-house architects reduced OSFI audit findings by 42% compared to pure outsourcing, according to the Canadian fintech and Bank of Canada figures cited here.

That aligns with what works in practice. Keep a core internal architecture and compliance spine. Let the external team provide execution scale around it.

The internal group should typically retain ownership of:

target architecture

regulatory interpretation

release sign-off

security exceptions

integration priorities

core domain decisions

The partner should contribute structured delivery, technical implementation, QA capacity, and a repeatable engineering process.

What to test in vendor conversations

Skip vague questions like “Do you have financial services experience?” Ask questions that expose operating maturity.

Try questions like these:

How do you document business rules that are discovered during implementation?

Who owns the acceptance criteria when requirements evolve mid-sprint?

How do you handle masked data, synthetic data, and restricted environment access?

What's your process for defect triage when the issue may involve code, infrastructure, or unclear requirements?

How do your engineers escalate concerns about missing compliance details?

What artefacts do you leave behind if the client transitions the work elsewhere?

Their answers should be specific. You want named practices, real artefacts, and clear ownership lines.

Review their documentation habits, not just their code samples

A partner that can't write clearly usually can't deliver predictably in a regulated environment. Before signing anything substantial, ask them to respond to a scenario with sample artefacts: a backlog breakdown, risk log excerpt, test approach, architecture note, and assumptions list.

If your own team needs a stronger baseline for this stage, a solid 2026 technical requirement guide helps structure functional scope, constraints, dependencies, and acceptance logic before detailed vendor negotiation begins.

You can also compare your shortlist against practical delivery considerations in this guide to mastering fintech software development, particularly if you're balancing product speed with regulatory review.

Look for fit across four dimensions

Here's a simple way to score candidates without overcomplicating procurement:

| Dimension | What good looks like | Warning sign |

|---|---|---|

| Domain fit | Understands financial workflows and controlled delivery | Talks mostly about generic app development |

| Delivery maturity | Clear QA, backlog, release, and escalation routines | Relies on ad hoc coordination |

| Collaboration model | Comfortable with client-owned architecture and governance | Pushes for full control too early |

| Knowledge transfer | Documents decisions and supports handover | Treats delivery knowledge as tribal knowledge |

Selection advice: If a partner resists client-side architectural oversight, they're probably not the right fit for financial software outsourcing.

One practical note. Some firms will want a partner that can support custom software delivery across regulated sectors, not only financial services. In that scenario, providers such as Cleffex Digital Ltd may fit evaluation lists where the need includes custom development, agile delivery, and compliance-aware engineering, but they should still be assessed with the same discipline as any other candidate.

The best partnerships don't remove your internal ownership. They strengthen it by giving your organisation more controlled execution power.

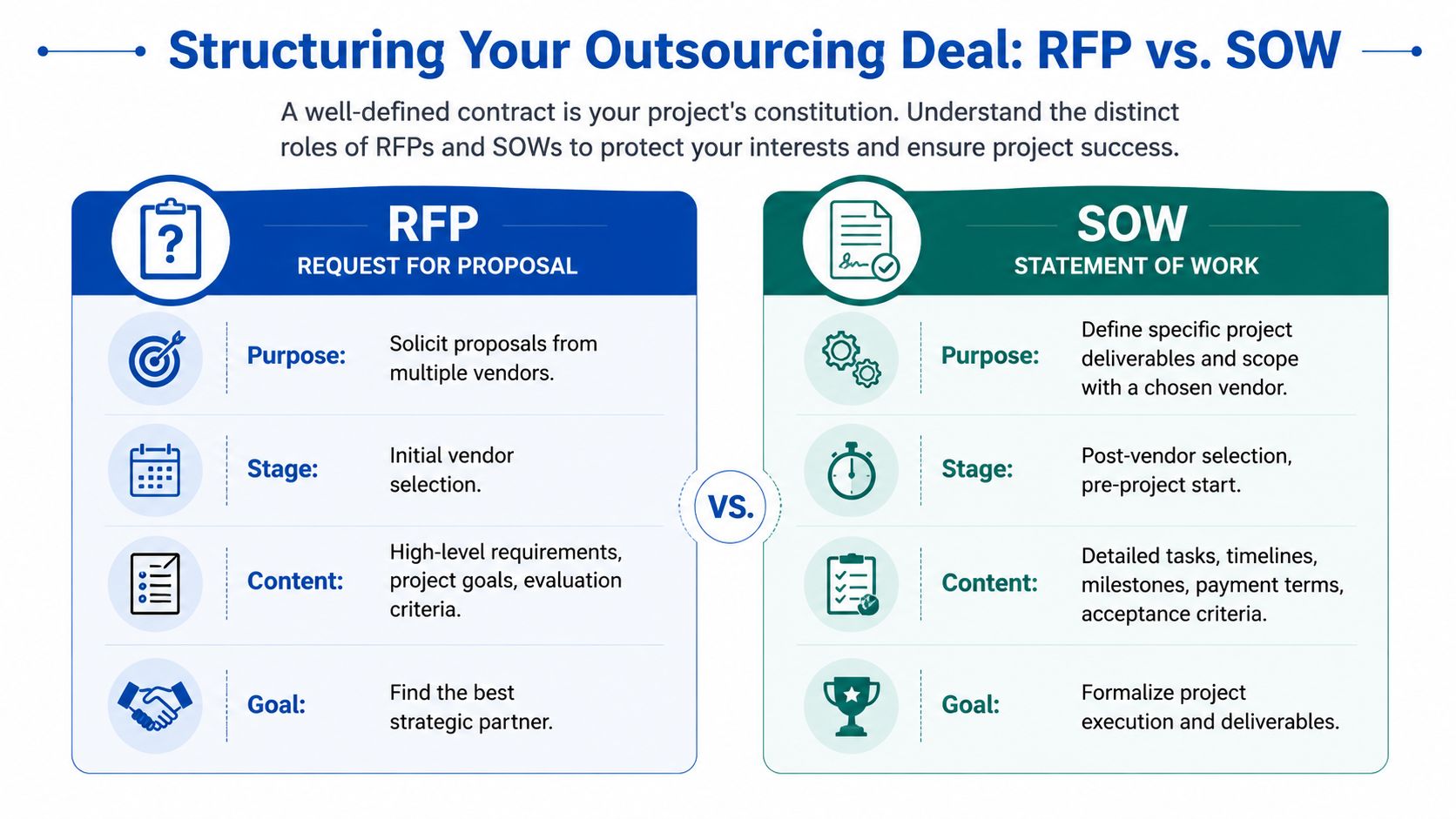

Structuring the Deal for Maximum Success

Most outsourcing disputes don't start with bad intent. They start with fuzzy scope, weak assumptions, and contracts that describe payment better than delivery. In financial software, that's dangerous because every unclear requirement can ripple into testing, controls, audit evidence, and release readiness.

Your RFP and your SOW serve different purposes. One helps you choose. The other helps you execute.

What belongs in the SOW

A workable Statement of Work should remove guesswork from the operating relationship. At a minimum, include:

Scope boundaries: What is in, what is out, and what needs separate approval

Deliverables: Code, test artefacts, documentation, runbooks, deployment support, training

Acceptance criteria: Business, technical, and security conditions for sign-off

Roles: Who approves scope, who signs releases, who owns architecture decisions

Dependencies: Client inputs, environment readiness, access approvals, third-party services

Change control: How scope changes are proposed, reviewed, priced, and approved

IP and artefact ownership: Source code, infrastructure scripts, design files, documentation

Exit support: Transition obligations, handover timelines, knowledge-transfer expectations

If these points are vague, the project will drift even with a competent partner.

Comparing the three main engagement models

Different commercial models fit different risk profiles. The right choice depends less on preference and more on how stable your scope really is.

| Model | Best fit | Strength | Risk |

|---|---|---|---|

| Fixed Price | Narrow, well-defined deliverables | Cost predictability | Expensive change requests if scope evolves |

| Time and Materials | Agile work with evolving needs | Flexibility | Can drift without strong governance |

| Dedicated Team | Long-term product or platform work | Continuity and retained context | Requires active client management |

Fixed Price

Use this when requirements are stable, integrations are known, and acceptance criteria are detailed enough to test objectively. It works best for contained initiatives such as a defined customer portal phase or a reporting module with clear business rules.

It fails when clients use it to buy certainty they haven't earned. If the business is still discovering what it wants, a fixed price hides uncertainty until change requests appear.

Time and Materials

This model fits modernisation, and iterative product work better. If you expect requirements to change as users see demos, T&M usually reflects reality more accurately.

The trade-off is management discipline. You need backlog hygiene, sprint-level acceptance, and regular budget visibility. Without that, flexibility turns into sprawl.

Dedicated Team

This is often the strongest fit for multi-quarter financial software outsourcing. You get continuity, accumulated system knowledge, and more stable team dynamics. It suits organisations building or modernising a product line rather than completing one isolated project.

The catch is that the client must behave like an engaged product owner, not a passive buyer.

A simple way to choose

Use this decision lens:

Choose Fixed Price when the scope is settled, and the business needs to spend predictably.

Choose T&M when discovery is still happening and the speed of learning matters.

Choose a Dedicated Team when the roadmap is continuous and knowledge retention matters more than short-term transaction efficiency.

A contract should describe how uncertainty will be handled, not pretend uncertainty doesn't exist.

In practice, many successful deals combine models. Discovery may run on T&M, a tightly defined MVP may move to fixed price, and post-launch development may shift to a dedicated team. What matters is alignment between commercial structure, delivery reality, and governance strength.

Effective Governance and Performance KPIs

Outsourcing doesn't reduce the need for management. It raises the quality bar for management. Strong governance isn't bureaucracy. It's the operating system that keeps delivery, compliance, and accountability connected.

Many first-time outsourcing efforts lose control when leaders sign a contract, schedule a weekly status call, and assume the vendor will self-correct. That doesn't work in regulated delivery.

Set a communication rhythm that matches the work

A practical governance cadence usually includes three levels.

Daily delivery contact keeps blockers visible. This is the level for stand-ups, test issues, environment delays, and requirement clarifications.

Weekly operational review tracks sprint progress, defects, risks, scope changes, and dependency status. Product, engineering, QA, and delivery leads should all be represented.

Monthly or quarterly steering review handles broader concerns such as budget drift, roadmap shifts, unresolved risks, audit themes, and contract-level issues.

A simple rhythm works better than a heavy one. The key is consistency and decision ownership.

Define who decides what

When governance fails, it's often because everyone is informed but no one is accountable. Document decision rights early.

| Area | Client owner | Partner owner |

|---|---|---|

| Product priority | Yes | Input only |

| Architecture approval | Yes | Recommendation |

| Sprint execution | Shared oversight | Yes |

| QA process execution | Shared standards | Yes |

| Security policy | Yes | Compliance with policy |

| Release readiness evidence | Shared review | Yes for artefacts |

This prevents the familiar problem where the partner thinks a requirement was implied and the client thinks it was obvious.

Measure process quality, not just effort

In 2024, IT automation was the most popular IT trend, and mature outsourcing providers should be assessed by their ability to automate delivery processes, while treating outsourcing as pure labour arbitrage increases risk and weakens integration, according to Statista's IT outsourcing overview.

That matters because hours billed tell you very little. Better KPIs focus on whether the delivery system is healthy.

Useful KPI categories include:

Quality indicators: Escaped defects, failed test cases, regression stability, rework volume

Flow indicators: Backlog ageing, sprint completion reliability, cycle time for approved work

Control indicators: Documentation completeness, traceability to acceptance criteria, and change approval adherence

Operational indicators: Incident response timeliness, environment availability, deployment readiness

Add quality gates to every release path

You don't need complicated tooling to create discipline, but you do need gates that nobody bypasses casually.

A solid release path usually requires:

approved scope for the release

completed test evidence

documented security or compliance checks where required

defect review with clear acceptance of residual risk

deployment runbook and rollback readiness

named approver on the client side

Good governance catches small delivery problems while they're still cheap.

Use dashboards that support decisions

The best reporting dashboard is boring. It shows open risks, milestone status, budget consumption, quality trends, and unresolved dependencies in a way that lets leaders act quickly.

Avoid dashboards stuffed with vanity metrics. If a metric doesn't trigger a decision, it's noise. Financial software outsourcing works when governance is close enough to spot drift early, but lean enough that teams still ship.

Budgeting Costs and Planning for Maintenance

The quoted day rate or sprint price is rarely the true cost of outsourcing. Teams underestimate the work required to define scope, transfer knowledge, review outputs, manage environments, and support the application after release. Then they blame outsourcing when the actual issue was incomplete budgeting.

You can save money with outsourcing, but only if you budget for the full operating model.

Look at the total cost, not just vendor invoices

The strongest financial case usually comes from separating costs into stages.

| Cost area | What it includes |

|---|---|

| Discovery and setup | requirements shaping, architecture review, onboarding, access setup |

| Core delivery | engineering, QA, design, DevOps, project coordination |

| Client-side overhead | product ownership, compliance review, security review, stakeholder time |

| Platform and tooling | cloud usage, test tools, monitoring, collaboration tools |

| Post-launch support | bug fixes, patching, support coverage, minor enhancements |

This is the budget conversation many firms skip. They compare external engineering cost to internal salaries and miss the operational load required to make the model work.

Why planning quality controls the savings

Some functions in software outsourcing can save up to 70% in development costs, but those gains depend on clear specifications and governance. Outsourcing without a detailed plan is a common cause of cost overruns, as noted in Market.us software development outsourcing analysis.

That's the key qualifier. Savings don't come from cheaper labour alone. They come from structured execution, lower rework, better utilisation of specialists, and a controlled scope.

Budget erosion usually comes from five places:

Unclear requirements: The team builds, revises, and rebuilds the same workflow

Weak knowledge transfer: External engineers spend too long uncovering basic domain logic

Client bottlenecks: Approvals, data access, and environment setup take longer than planned

Late compliance input: Rework appears after legal or security review

No maintenance agreement: Support gets handled as a series of ad hoc requests

Build maintenance into the original deal

Software isn't finished at launch. Financial applications need patching, dependency updates, incident handling, access review, and controlled enhancement work. If maintenance is treated as an afterthought, support quality drops as soon as the implementation team rolls off.

A practical maintenance plan should define:

support hours and response expectations

severity levels and escalation path

patching and upgrade responsibilities

warranty boundaries versus paid enhancement work

documentation updates after each material change

handoff process between the project and support teams

If you need a clearer view of the operational side, this detailed guide on app maintenance costs is a useful reference for planning post-launch obligations instead of treating them as miscellaneous overhead.

Budget for retention of knowledge

One cost many firms miss is continuity. If your outsourced team changes and your own team hasn't retained enough design context, every future enhancement becomes slower and riskier.

That's why maintenance budgeting isn't only about support hours. It's also about preserving architecture notes, decision logs, release history, and business rule documentation. Those artefacts reduce dependency on any single individual or supplier.

A realistic budget makes financial software outsourcing easier to govern because it funds the full lifecycle, not just initial delivery.

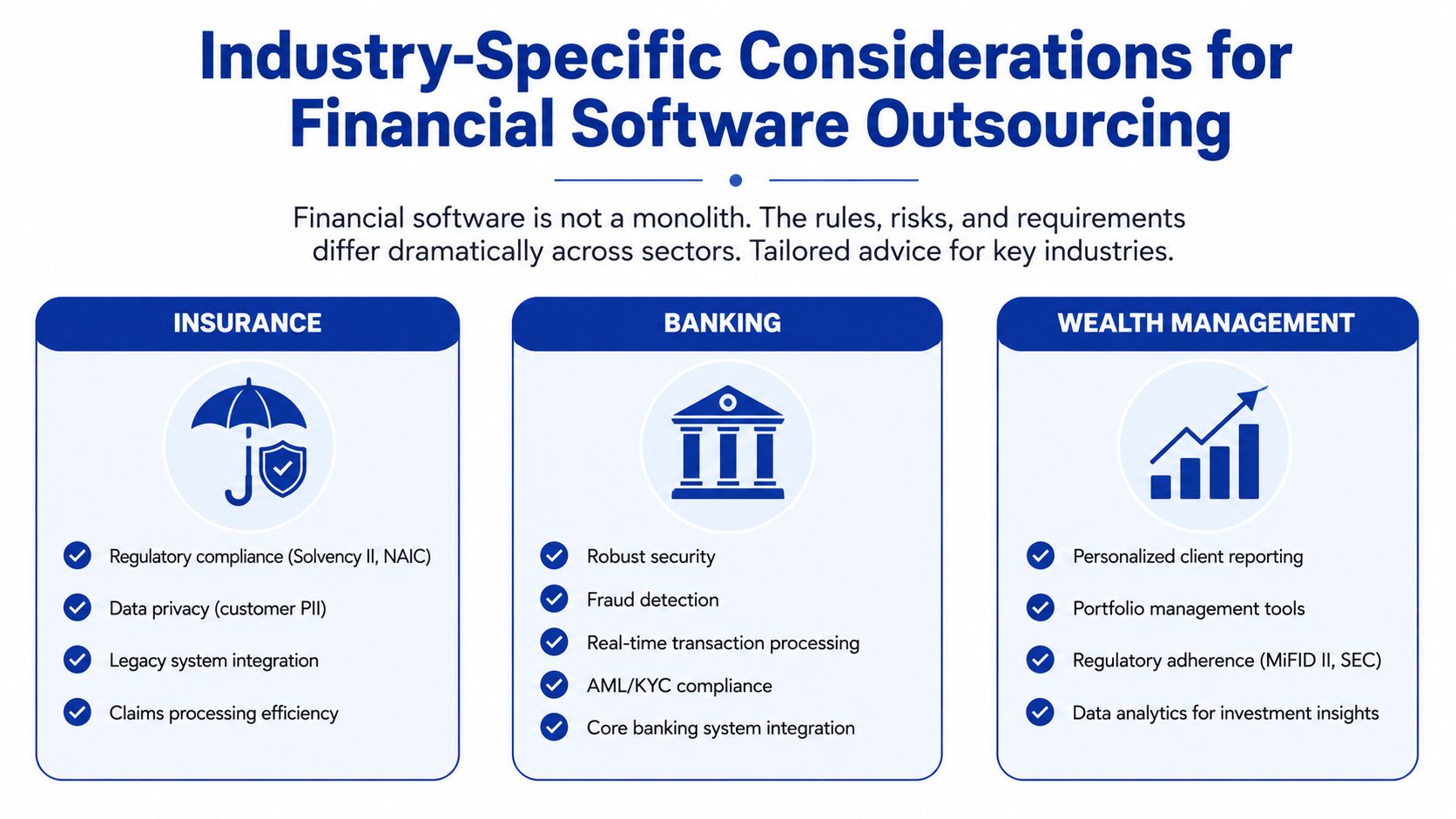

Industry Specific Considerations for Success

Financial software outsourcing changes shape depending on the business model. An insurer modernising policy systems has different risks from a digital lender launching a new onboarding flow. A wealth platform handling reporting and portfolio tools faces different pressures again. The outsourcing approach should reflect the operational reality of the sector.

Insurance and legacy policy platforms

An insurance firm often starts with a stable but rigid policy administration platform. It handles underwriting, endorsements, renewals, and claims inputs, but every integration is awkward, and every customer-facing improvement takes too long. The temptation is to give an external team broad access to the legacy core and ask them to move quickly.

That's where projects become fragile. Legacy insurance systems usually hold sensitive customer data, embedded business rules, and years of undocumented exceptions. The safer pattern is to isolate the core through controlled interfaces and let the outsourced team build around it, not directly inside it, unless there's strong internal oversight.

Banking and lender environments

A bank or lender has less tolerance for ambiguity in transaction handling, identity checks, reconciliation, and audit trails. External developers can help build channels, APIs, servicing tools, or internal operations software, but work must sit inside clearly defined control boundaries.

Documentation matters even more here. Teams that produce clean interface specifications, decision logs, and traceable test evidence are easier to govern. For organisations that need stronger internal artefacts before or during outsourcing, Fintech engineering documentation can help standardise technical records around regulated product delivery.

In regulated finance, missing documentation is often a control issue before it becomes a delivery issue.

Wealth management and reporting-heavy products

Wealth platforms depend on trust, reporting accuracy, portfolio visibility, and advisor workflows. The outsourced work often touches dashboards, client portals, analytics layers, statement generation, or integration services. The delivery challenge is less about raw transaction throughput and more about consistency, presentation quality, and data lineage.

In these environments, acceptance criteria should be unusually explicit. It's not enough for a report to render. The team needs documented rules for calculations, rounding, exception handling, role visibility, and version control of business logic.

The legacy system security trap in Canada

The most severe risk appears when Canadian financial firms outsource work on legacy systems without adding protective layers first. 74% of Canadian financial outsourcing deals trigger OSFI security incidents when legacy systems are involved, and a middleware-first model that embeds real-time audit logs and data masking before offshore access reduced those breaches by 37% among Canada's top insurers, according to Deloitte's cited discussion of software engineering in banks.

That finding points to a practical rule. Don't expose legacy cores directly if you can avoid it. Insert a control layer first.

A middleware-first pattern can help by:

Masking sensitive data before external teams interact with records

Capturing audit logs in a form your internal teams can review

Standardising access paths instead of allowing direct and inconsistent system touchpoints

Reducing accidental control bypasses during maintenance and integration work

What success looks like across sectors

The sector changes, but the successful pattern is consistent:

retain internal ownership of regulation, architecture, and release risk

outsource execution where specialist capacity is needed

use segmented access instead of broad exposure

insist on documented business rules and acceptance logic

plan maintenance and handover from the start

Financial software outsourcing is safest when the delivery model respects how regulated systems behave. The firms that do this well don't outsource judgment. They outsource controlled execution.

If you're planning your first major outsourcing initiative and need a partner that can work within a compliance-aware delivery model, Cleffex Digital Ltd is one option to evaluate for custom software development, modernisation, and regulated digital product delivery in Canadian and cross-border environments.