You're probably dealing with some version of the same problem most insurance technology leaders face. Core systems still run the business, but they also slow it down. Claims teams want less swivel-chair work. Underwriters want cleaner data. Distribution leaders want faster launches. Compliance wants fewer surprises. Every vendor says they can help.

That's why choosing an insurance IT development partner can't be treated like ordinary software procurement. In insurance, a weak partner doesn't just miss sprint dates. They create operational risk, expose compliance gaps, and leave you with brittle integrations that nobody wants to own a year later.

The right partner should reduce uncertainty, not add another layer of it.

Why Your Next IT Partner Is a Strategic Bet

If you sit inside an insurer today, the pressure comes from all sides at once. Customers expect digital self-service that works the first time. Brokers and partners expect faster quoting and cleaner servicing workflows. Internal teams still depend on older policy, billing, and claims platforms that were never designed for modern API traffic, embedded distribution, or real-time decisioning.

That tension is why partner selection belongs in strategy discussions, not just procurement.

The spending patterns across the industry make that clear. HG Insights projects that the global insurance industry will spend $291 billion on IT over the next 12 months, with 49.8% of that market in the Americas. It also identifies 29,721 U.S. companies projected to spend $128.1 billion, with 47% of spending going to IT services and 31% to software, according to the HG Insights insurance industry report.

Why This Decision Carries Board-Level Consequences

A lot of teams still approach vendor selection as if they're buying capacity. They aren't. They're choosing who gets access to sensitive workflows, customer data, architectural direction, delivery practices, and often the political capital attached to a modernisation programme.

A strong partner helps you make better trade-offs:

What to modernise first so you don't stall in a multi-year transformation

Where to place APIs so channels can scale without exposing fragile core logic

How to design around compliance instead of patching it in later

Which workflows deserve automation now, and which should stay manual until the data is ready

A weak partner usually does the opposite. They accept every requirement at face value, overpromise on timelines, and leave the insurer to discover integration and governance problems after build starts.

Practical rule: If a partner never challenges your assumptions, they're probably not doing strategic work. They're taking orders.

The Better Framing

The better framing is simple. You're not hiring a coding vendor. You're selecting an operating partner for one of the most regulated and process-heavy environments in enterprise technology.

That's also why broad “digital transformation” language isn't enough. You need a partner who can translate insurance operations into delivery choices. If your team is still refining that wider operating model, it helps to align internally around what a true digital transformation partner is expected to do before you start evaluating suppliers.

The firms that get this right usually start with hard business constraints, not feature wish lists. They know where service bottlenecks live, where handoffs fail, and where architecture needs to stay flexible because the business won't stand still.

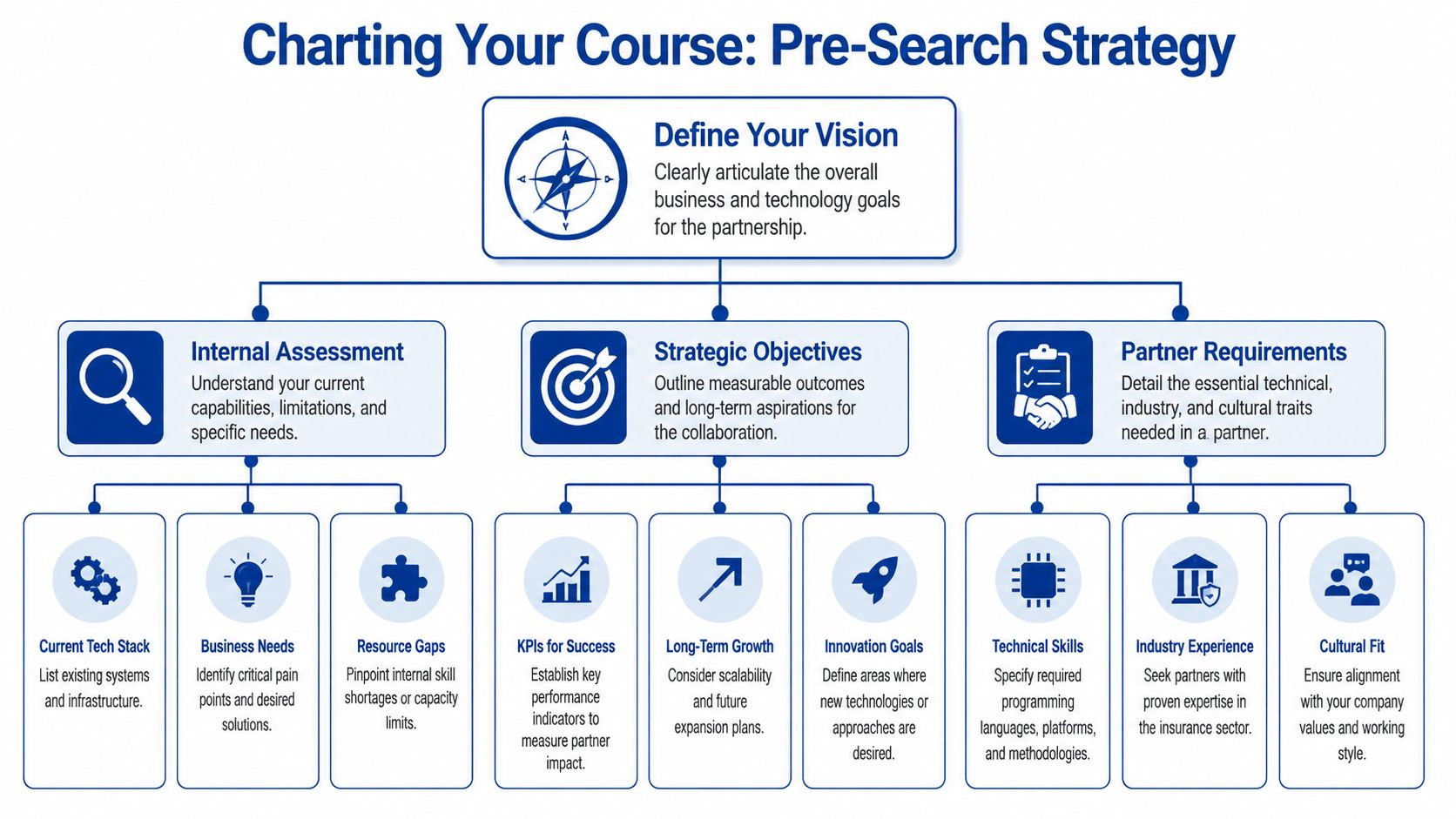

Charting Your Course Before You Search

Most failed partner searches start too early. The organisation knows it wants change, but it hasn't decided what kind of change matters first.

That leads to vague RFPs, inflated proposals, and demos that look polished but don't answer the operational problem. In Canadian insurance, that problem is often tied to claims pressure, distribution friction, or servicing inefficiency rather than a pure technology gap.

The urgency is real. Insured damages from severe weather in Canada reached CA$3.1 billion in 2023, the third-worst year on record, which strengthens the case for claims automation and better risk analytics, as noted in this insurance modernisation overview.

Start With the Business Event, Not the Tool

A useful project charter begins with a specific trigger. For example:

Claims overload after weather events exposes manual intake and triage weaknesses.

Broker dissatisfaction caused by slow quote-to-bind flows.

A planned embedded product launch that requires external partners to connect cleanly.

Service centre congestion is driven by repetitive policy changes and document handling.

Each of those problems can justify a technology investment. They don't justify the same one.

If you tell a potential insurance IT development partner that you “need AI, cloud, and automation,” you'll get a generic response. If you tell them that FNOL intake breaks because adjusters rekey data from email attachments into a legacy claims system, the conversation gets concrete fast.

Define the First Win

Teams often lose momentum because they aim at enterprise-wide modernisation before proving one outcome. In practice, the first win should be narrow enough to deliver, but important enough to matter.

Good candidates include:

Quote-To-Bind Improvement

A contained flow with visible business owners and measurable handoffs.FNOL Intake Modernisation

High operational pain, strong case for workflow and document automation.Broker or Partner Portal Integration

Useful when distribution speed matters more than internal UX refreshes.Claims Document Classification

Best when the organisation already has document volume but poor routing discipline.

A good first phase solves one painful workflow end-to-end. It doesn't try to rescue every legacy dependency in the estate.

Map Constraints Before You Speak to Suppliers

You also need an honest internal inventory. Not just of systems, but of blockers.

Create a short pre-RFP pack that covers:

Current systems: Policy admin, billing, claims, CRM, document management, data platforms

Integration posture: Existing APIs, batch jobs, vendor-managed interfaces, manual workarounds

Control requirements: Privacy, auditability, security reviews, data residency expectations

Internal capacity: Who can own product decisions, who can test, who can approve changes

Success measures: Adoption, turnaround time, accuracy, lower manual effort, better service quality

A partner can help shape the scope. They can't compensate for a buyer who hasn't decided who makes the decisions.

If your internal planning is still loose, it's worth using a structured technology roadmap template to connect business outcomes, delivery phases, dependencies, and governance in one place.

Separate MVP From Full Modernisation

Many insurance organisations blur important lines.

An MVP should prove one transaction path, one integration pattern, or one user journey. A full modernisation changes the operating model, governance, support, and often the architecture around multiple workflows.

Ask two questions before you expand the scope:

Does this first release prove a reusable pattern?

Does the data support automation decisions, or are you still cleaning inputs?

If the answer to either question is no, stay narrow. The cheapest way to create expensive technology debt is to scale an unproven design because the steering committee wants momentum.

The Vetting Process for Your Tech Partner

A capable insurance IT development partner doesn't win on slides. They win in the details: how they talk about policy workflows, how they handle failed integrations, how they design around auditability, and how quickly they move from vague ambition to an architecture you can govern.

That matters even more because the market is already tilted toward modern platforms. In the North American insurance market, cloud deployment captured 65.10% of insurance software revenue and is projected to grow at a 10.26% CAGR through 2031, according to the IMARC insurance software market analysis. If a partner still treats cloud-native delivery as optional, they're behind the operating reality of the sector.

Insurance Fluency Beats Generic Enterprise Experience

This is the first filter. Many software firms can build interfaces, integrations, and dashboards. Fewer understand how insurance decisions flow across underwriting, servicing, claims, and partner distribution.

Listen for operational fluency in discovery calls. Can they discuss quote-to-bind, FNOL, adjudication, bordereaux-style feeds, policy changes, document ingestion, referral paths, and audit trails without needing a glossary? Do they understand that insurance platforms often need to support both digital self-service and exception-heavy manual handling?

A partner with real domain depth usually asks better questions:

Where does straight-through processing break?

Which decisions need explainability?

What percentage of work lands in exception queues?

Who owns business rules today?

Which workflows cross legal entities, provinces, or channel partners?

If the conversation stays at “we build scalable apps,” keep looking.

Architecture Judgement Matters More Than Framework Preferences

In Canada, the most effective pattern for many growth and distribution use cases is a plug-and-play API stack with centralised API management. For embedded or partner-distributed insurance, the platform has to let third parties integrate with minimal effort, while underwriting, issuance, servicing, and claims remain accessible through standardised APIs. BCG also notes the platform should be secure, fault-tolerant, metered, and decoupled from core systems, as described in BCG's guidance on getting the tech stack right for embedded insurance.

That's the benchmark I'd use in partner interviews. Ask them to draw the architecture for one channel flow, not just talk about principles.

Look for these signs of maturity:

Clear API boundary design: What sits in the partner layer versus the core

Resilience thinking: Retries, queueing, idempotency, graceful degradation

Observability: Logs, tracing, metrics, alerting, transaction visibility

Release strategy: Rollback plans, environment discipline, versioning approach

The partner you want can explain where the architecture should bend and where it must not.

Delivery Process Tells You How Risk Will Be Handled

Polished vendors often unravel in such scenarios. They show nice ceremonies, but they don't show how ambiguity, defects, and late changes are managed when an insurer's internal dependencies shift.

Use live examples. Ask what they do when a core vendor blocks an integration, when business SMEs disagree on rules, or when testing reveals policy exceptions that weren't captured in design.

Strong answers usually include:

Visible backlog discipline

A decision log

Explicit assumptions

Demo-based validation

Change control that isn't bureaucratic but is still real

If you want a baseline external checklist, this guide on choosing the right software development company is a useful supplement. In insurance, though, add domain, compliance, and integration depth on top of those standard criteria.

What To Score During Final Evaluation

Instead of a generic vendor matrix, score partners against these practical dimensions:

| Evaluation area | What good looks like | What should worry you |

|---|---|---|

| Domain knowledge | Speaks comfortably about underwriting, claims, servicing, partner channels | Talks only in generic product terms |

| Technical design | Can map APIs, cloud services, workflow automation, and security controls | Focuses on front-end demos and avoids architecture depth |

| Delivery discipline | Defines assumptions, dependencies, test ownership, escalation routes | Promises speed without naming risks |

| Governance fit | Works with audit, security, legal, and business owners | Treats governance as a late-stage blocker |

| Support model | Explains post-launch ownership, SLAs, incident handling | Sees go-live as the end of responsibility |

One grounded option in this category is Cleffex Digital Ltd, which offers insurance software development and AI-enabled insurance workflow support as part of its broader custom software practice. That kind of partner may fit buyers looking for custom build capacity with insurance and compliance-aware delivery. It should still be evaluated against the same scorecard as any other vendor.

Crafting the RFP and Choosing an Engagement Model

By the time you issue an RFP, you should already know what problem you're solving, what systems are in scope, and what level of organisational change you're prepared to absorb. The RFP's job is to expose whether a supplier can operate within those constraints.

Weak RFPs produce decorative answers. Good ones force specificity.

Questions That Reveal Real Capability

Skip broad prompts like “Describe your insurance experience” or “Explain your agile process.” They invite recycled sales copy. Ask questions that require judgment, trade-offs, and evidence.

Use questions such as:

How would you approach a priority workflow first? Ask the bidder to outline a phased delivery path for quote-to-bind, FNOL, broker servicing, or another named use case.

Where would you place the API layer? Make them describe how they'd decouple partner traffic from core systems.

What assumptions are you making about our current data quality? This surfaces whether they understand automation risk.

How do you handle technical debt introduced during fast delivery? Good partners won't pretend it disappears.

What would make you recommend against a fixed-price model here? This tests commercial honesty.

Which project roles must come from our side? If they say they can do everything without business ownership, they're telling you what you want to hear.

How do you manage scope changes after discovery? You want a method, not a shrug.

What does post-launch support include? Ask for incident response, maintenance boundaries, and handover details.

Show us a sample architecture artefact, backlog structure, and risk register. Don't rely on verbal confidence.

Buying advice: The best RFP responses usually narrow the problem. The weakest ones say yes to everything.

Ask for Proof in the Right Format

Don't just request case studies. Request evidence you can inspect.

For example, ask for:

Anonymised architecture diagrams

Sample user stories

Test strategy examples

API documentation samples

A delivery plan for the first release

Named roles for the proposed team

A draft RAID log format

That gives you something more useful than a logo slide.

If you need a plain-language reference while weighing commercial structures, this breakdown of how to compare agency software pricing options is a helpful external read. It's written for agency software buyers, but the pricing logic maps well to broader insurance technology engagements.

Comparison of IT Partner Engagement Models

| Model | Best For | Pros | Cons |

|---|---|---|---|

| Fixed Price | Narrow, well-defined projects with stable requirements | Budget predictability, easier procurement approval, clear deliverables | Encourages change friction, can reward minimal compliance with the brief, risky when requirements are still emerging |

| Time & Materials | Discovery-heavy work, legacy integration, evolving product scope | Flexible, supports iteration, better for complex problem-solving | Requires stronger governance from the client side, budget can drift if priorities are weak |

| Dedicated Team | Ongoing platform work, multi-phase modernisation, internal capacity gaps | Continuity, faster knowledge retention, better for long-term product evolution | Needs clear product ownership, can become expensive if utilisation is poor |

Which Model Usually Fits Insurance Work

In practice, most meaningful insurance technology programmes don't resemble fixed-scope website builds. They involve legacy dependencies, unclear business rules, and process exceptions that only emerge when users see working software.

That's why many insurers choose a hybrid pattern:

A short discovery or PoC

Followed by time and materials for the first operational release

Then, a dedicated team will be formed if the product proves its value

Fixed price can still work for contained deliverables, such as a portal enhancement, a bounded integration, or a specific migration utility. It usually fails when buyers try to force certainty onto a problem they haven't fully understood.

Commercial structure should match uncertainty. If your requirements are still moving, don't pretend otherwise in procurement.

Spotting Red Flags and Ensuring a Smooth Onboarding

Most selection mistakes are visible before the contract is signed. The problem is that teams ignore them because the proposal looks polished or the timeline feels convenient.

When I see insurance projects struggle early, the cause is usually one of three things. The partner sold certainty where none existed. The insurer withheld critical constraints until late. Or both sides assumed “alignment” without defining how decisions would be made.

Red Flags Worth Taking Seriously

Some warning signs are obvious. Others look harmless until delivery starts.

Watch for these during final evaluation and contract discussions:

You can't speak with delivery leads: If access stays limited to sales staff, assume the handoff risk is high.

The proposal avoids assumptions: Good partners document what they know, what they don't, and what depends on you.

Everything is described as easy: Insurance workflows aren't easy. Mature firms acknowledge complexity without dramatising it.

Architecture stays vague: If they can't sketch service boundaries, integration methods, and control points, they probably haven't thought sufficiently.

Testing ownership is fuzzy: In insurance, business validation and exception handling can't be left implicit.

They resist governance artefacts: Risk logs, change records, and decision trails are not bureaucracy for this kind of work.

Support language is thin: If post-launch support reads like an afterthought, expect trouble after go-live.

If a partner promises speed but can't explain their failure-handling approach, they're selling optimism, not delivery discipline.

The First Thirty Days Matter Most

A smooth onboarding phase reduces rework later. During this phase, you convert a promising selection into an operating relationship.

Use a kickoff checklist with named owners on both sides:

Confirm Scope Boundaries

Define what is in, what is out, and what sits in a decision queue.Set Communication Rhythms

Weekly demos, delivery stand-ups, steering updates, and escalation paths should be scheduled immediately.Establish Artefact Standards

Decide how requirements, designs, API specs, test cases, and risks will be documented.Lockdown Environments and Access

Don't leave access provisioning until development is already blocked.Agree on Acceptance Criteria

Teams lose time when “done” means one thing to engineering and another to operations.

What a Healthy Working Cadence Looks Like

You don't need an elaborate ceremony. You need consistency.

A practical cadence often includes:

Weekly demo sessions with business users, not just IT

A shared backlog visible to both sides

A current RAID log is reviewed in every governance meeting

Named business approvers for rules, content, and workflow decisions

A support playbook drafted before launch, not after

This is also where trust becomes operational. The best partners don't just report progress. They surface uncertainty early, ask for decisions at the right moment, and make trade-offs visible before those trade-offs become defects.

A Case for Success: Modernising Claims Processing

A common Canadian scenario looks like this. A mid-sized insurer handles first notice of loss through a mix of phone calls, emailed forms, PDF attachments, and manual rekeying into a claims platform. During high-volume periods, intake quality drops, adjusters spend too much time sorting documents, and customers wait too long for clear next steps.

The insurer doesn't start by replacing the entire claims stack. It chooses a narrower path. It hires an insurance IT development partner to build a front-end intake layer, structured workflow routing, document capture, and API connections into the existing claims environment. The first release focuses on FNOL, triage, and adjuster assignment. Rules stay visible. Exceptions stay reviewable. Nothing critical gets buried in an opaque model.

Why This Works

This approach lines up with how insurers realise value from AI and workflow modernisation. McKinsey reports 10 to 20% improvement in new-agent success and sales conversion, 10 to 15% premium-growth uplift, 20 to 40% lower onboarding costs, and 3 to 5% claims-accuracy improvement when AI is deployed in targeted workflows, while Strategy& recommends small, agile steps, rapid prototyping, and recurring review cycles rather than a big-bang programme in its digital transformation guidance for insurers.

The lesson isn't “add AI everywhere.” It's narrower and more useful. Start with one workflow where data, decisions, and human review can be instrumented properly.

What the Insurer Gets From the Partnership

The strongest outcome isn't just a cleaner claims intake screen. It's a reusable delivery pattern.

That usually includes:

A proven API layer for legacy claims operations

Structured event and document handling

Clearer exception queues for adjusters

Audit-friendly business rules

A foundation for later automation in servicing or underwriting

Targeted modernisation tends to outperform broad transformation promises because operating teams can validate it quickly and improve it in production.

That's the value of the right insurance IT development partner. They don't just ship software. They help the insurer create a repeatable way to modernise without losing control of risk, governance, or business continuity.

If you're assessing options for an insurance IT development partner and want a team that can support custom insurance software, cloud modernisation, API-led integration, and applied AI delivery in a Canada-based context, Cleffex Digital Ltd is one firm to evaluate alongside your shortlist. The key is to use the same rigorous scorecard, RFP discipline, and onboarding controls outlined above so the partnership is judged on delivery fit, not sales polish.