For years, the insurance industry has operated by looking in the rear-view mirror. It analyzed past events to make decisions about the future. Now, imagine swapping that mirror for a smart GPS that not only shows the road ahead but anticipates traffic jams, warns of icy patches, and suggests faster, safer routes.

That’s what predictive analytics brings to the table for Canadian insurers. It’s a fundamental shift from a reactive "wait-and-see" model to a proactive, forward-thinking one.

The Future is Now: Understanding Predictive Analytics

Predictive analytics is all about looking forward, not back. Instead of just using historical claims data to set next year's premiums, it digs deeper. It combines past data with real-time information, feeding it all into sophisticated statistical algorithms to forecast what’s likely to happen next.

For a Canadian insurer, this means getting answers to critical questions before they become expensive problems.

This isn't about gazing into a crystal ball; it's a disciplined, data-driven science. The technology sifts through enormous datasets to find subtle patterns and connections a human analyst could easily miss. Think of it as connecting thousands of seemingly random dots to paint a surprisingly clear picture of the future. This gives insurers the power to anticipate events with a remarkable degree of accuracy.

From Reaction to Proaction

The most significant change that predictive analytics delivers is the move from a defensive, reactive posture to an offensive, proactive strategy. The old way was built on responding after something happened, a claim was filed, a policy lapsed, or fraud was discovered too late.

The new model is all about getting ahead of these events.

This proactive approach has a massive impact on core business functions:

Smarter Risk Assessment: Insurers can move beyond broad demographic buckets. Now, they can analyze an individual's specific behaviours and circumstances to set fairer, more accurate pricing.

Faster Claims Management: The moment a claim is submitted, predictive models can flag it as potentially fraudulent. This allows investigators to focus their time and energy where it matters most.

Better Customer Retention: By spotting the subtle signs that a customer is unhappy or likely to shop around at renewal time, insurers can step in with a targeted offer or improved service to keep them.

Predictive analytics gives insurers the foresight to act, not just react. It’s the difference between repairing a house after a storm and reinforcing the roof before the storm even hits. It saves money, time, and improves outcomes for everyone.

Setting the Stage for Change

Grasping this fundamental shift is the first step to seeing how it can benefit the entire insurance lifecycle. Every department, from underwriting and claims to marketing and customer service, stands to gain.

By getting a better handle on risk, fraud, and customer needs, Canadian insurers can build more resilient, efficient, and client-centred businesses. This guide will serve as your roadmap. We'll dive into specific use cases, break down implementation strategies, and navigate the unique regulatory landscape here in Canada. The goal is to get practical and show you how this technology is already reshaping the industry for a smarter, more responsive future.

Reshaping Risk Management for Canadian Insurers

Insurance has always been a game of managing risk. For centuries, the tools of the trade were static actuarial tables, broad-stroke generalizations built on historical data. But that old model is being dismantled, as predictive analytics in Canadian insurance operations replaces educated guesswork with genuine precision.

This isn't just a minor update. It’s a fundamental shift away from relying on basic demographics. Insurers can now pull in and analyze a staggering amount of data from countless sources, creating dynamic, living risk profiles for every policyholder. The result is a much sharper, more accurate picture of the real risks involved.

Building a Hyper-Accurate Risk Picture

So, how does this new level of precision work? It starts with data, and a lot of it. Predictive models comb through an expansive well of information, mixing traditional data with new, real-time streams to find connections and patterns that were simply invisible before.

These models are powered by a few key sources:

Historical Claims Data: Sifting through past claims helps identify common patterns, how often events happen, and how severe they are in certain areas.

Real-Time Weather Patterns: Meteorological data can forecast the odds of a hailstorm, a blizzard, or a flash flood hitting a specific postal code.

Telematics and IoT Data: Information from vehicle sensors or smart home devices gives a direct window into real-world behaviour, like driving habits or how well a property is maintained.

Geospatial Information: This involves mapping property locations against detailed environmental data, like how close a home is to a floodplain or an area prone to wildfires.

By weaving these datasets together, insurers generate risk scores that are incredibly nuanced. To really see the difference, it helps to understand the fundamentals of insurance underwriting, which is the core process this technology is overhauling. This data-first approach leads directly to fairer, more personalized premiums, where customers pay based on their actual risk, not the averaged-out risk of their entire demographic group.

To see this evolution clearly, let's compare the old way with the new.

Table: Traditional vs Predictive Risk Assessment in Canadian Insurance

| Aspect | Traditional Approach | Predictive Analytics Approach |

|---|---|---|

| Data Sources | Static historical data, demographics (age, gender), and postal code. | Dynamic and diverse: real-time weather, telematics, geospatial data, social media trends, claims history. |

| Risk Model | Based on broad, pre-defined segments and historical averages. One-size-fits-many. | Individualized, dynamic risk scores that update based on new information. Hyper-personalized. |

| Pricing | Premiums are based on the average risk of a large group. Less precise. | Premiums reflect an individual’s specific risk profile, leading to fairer, more accurate pricing. |

| Timeframe | Looks backward at what has already happened. | Looks forward, forecasting the probability of future events. Proactive and preventative. |

| Regional Nuance | Applies generalized provincial or national risk factors. | Models can be tuned to specific local risks, like urban flooding in Toronto or wildfires in Fort McMurray. |

This table shows a clear move from a static, reactive model to one that is dynamic, proactive, and deeply personalized.

Addressing Uniquely Canadian Risks

Canada’s sheer size and geographical diversity create unique challenges that predictive models are perfectly built to handle. A risk in British Columbia is completely different from one in Atlantic Canada, and predictive analytics allows insurers to finally account for that crucial regional detail.

For example, models can be trained to focus on specific Canadian environmental threats. Insurers can now model the rising risk of wildfires in Western Canada by analyzing forest density, historical burn patterns, and real-time drought conditions. Likewise, they can pinpoint potential flood zones in the Prairies by combining topographical data with snowmelt rates and river-level monitoring.

This kind of advanced analysis is essential for managing the growing impact of climate change, a major concern for every insurer in the country. Actuaries can use these forward-looking models to adjust their strategies ahead of time, ensuring they’re ready for more frequent and severe weather. This capability is absolutely vital for staying solvent and serving customers when they need it most.

A home in Kelowna, BC, and a home in St. John's, NL, face entirely different primary risks. Predictive analytics allows an insurer to price both policies with an accuracy that reflects their unique environmental realities, rather than relying on a blunt, nationwide average.

Ultimately, this leads to a more resilient and stable insurance market. When insurers can accurately price risk, they are better capitalized to handle large-scale events, making sure they can pay out claims when disaster strikes. While predictive analytics is all about forecasting, it's also worth noting how its counterpart, generative AI, is opening up new doors. For more on that, check out our guide on generative AI in the insurance industry to see how these powerful technologies can work in tandem.

Here is the rewritten section, designed to sound like an experienced human expert:

Where the Rubber Meets the Road: Predictive Analytics in Action

Predictive analytics isn't just a fancy term for better spreadsheets; it’s fundamentally changing how Canadian insurers get work done. When you look past the buzzwords, you can see it bringing real, measurable value to the core functions of the business: underwriting, claims, and keeping customers happy. It’s all about turning slow, manual processes into smart, automated ones.

This isn't about replacing seasoned professionals. Quite the opposite. The goal is to let the models handle the high-volume, data-intensive tasks so your experts can focus their time and energy on the tricky, nuanced cases that truly require human judgment. Let's walk through what this looks like day-to-day in a few key departments.

From Days to Seconds: A New Era for Underwriting and Quoting

Anyone who has been in the industry for a while knows the traditional underwriting drill. It was often a slow, paper-heavy process that involved manually digging through data and cross-referencing generalized risk tables. A potential customer could be left waiting for days just to get a quote, giving them plenty of time to get a better offer from a competitor.

Predictive analytics completely flips that script.

The Old Way: An underwriter would get an application, manually check it against static actuarial tables, and maybe pull a standard credit or driving report. The whole thing could take days, relied on a handful of data points, and often resulted in a quote that was more of a ballpark estimate than a precise calculation.

The New Way: An automated system sifts through an applicant's data, comparing it against thousands of variables in real time. It can pull from multiple data sources, spot complex risk patterns a human might miss, and generate a highly accurate, personalized quote in seconds. The underwriter is now freed up to manage exceptions and apply their expertise to complex, high-value policies.

This speed is a game-changer. A customer can get a firm quote almost instantly, which massively improves their experience and makes them far more likely to sign on the dotted line. For Canadian insurers, this means getting more efficient, cutting operational costs, and gaining a real edge in a very competitive market.

Smarter Claims and Proactive Fraud Detection

Historically, the claims department has been a major bottleneck. Legitimate claims would get stuck in a queue while adjusters waded through paperwork. Meanwhile, fraudulent claims could slip through, only to be discovered after the money was already gone, a huge financial drain.

Predictive analytics brings much-needed speed and a proactive defence to the entire claims process. Models can analyze claims the moment they come in, instantly sorting them by complexity and the likelihood of fraud.

Think of it this way: a model can learn from thousands of past claims, recognizing the subtle red flags of fraud, like a claim filed right after a policy is activated or one with details that just don't add up. It can then automatically flag a new, suspicious claim for immediate review by a specialist.

This intelligent routing creates two huge benefits:

Fast-Track for Honest Claims: Straightforward, low-risk claims can be approved and paid out in a matter of hours, not weeks. This is a massive win for customer satisfaction, especially when a policyholder is going through a stressful time.

Isolate Suspicious Claims: High-risk claims are immediately sent to your specialized fraud teams. This lets your investigators focus their skills where they'll have the biggest impact, boosting recovery rates and discouraging future fraudsters.

This one-two punch, delighting good customers with fast service while efficiently stopping fraud, is one of the most powerful applications of predictive analytics in Canadian insurance operations.

Keeping Your Customers: Retention and Smarter Marketing

Finally, predictive analytics gives you a much clearer window into what your customers are thinking. In the past, you often didn't know a customer was unhappy until you got the cancellation notice in the mail. At that point, it was already too late.

Today, predictive models can spot the early warning signs of a customer who is thinking of leaving. By looking at data like payment patterns, recent interactions with the call centre, or changes to a policy, an algorithm can assign a "churn score" to every single policyholder.

A customer with a high churn score can be flagged for a proactive retention effort. Maybe it’s a personalized email, a special discount offer, or a quick call from a service agent to see if everything is okay. This targeted strategy is infinitely more effective and budget-friendly than generic marketing blasts. It helps insurers put their retention efforts where they count the most, building loyalty and protecting their bottom line.

Boosting Efficiency and Enhancing Customer Journeys

The biggest win with predictive analytics in Canadian insurance is its powerful one-two punch: it simultaneously sharpens up internal operations while creating a far better experience for customers. These two benefits are completely intertwined. When an insurer runs smarter on the inside, customers feel it on the outside.

This isn't about small, incremental tweaks. It's about automating the repetitive, data-heavy work that used to bog down skilled professionals. Think about all the time claims adjusters spend on simple, low-risk files or underwriters spend manually checking standard application details. Predictive models can now handle a huge chunk of that workload, and they often do it faster and more accurately.

This frees up your human experts, the adjusters, underwriters, and service agents, to focus on the tricky, high-value work where they truly make a difference. Instead of being buried in paperwork, they can navigate complex claims, structure sophisticated policies, or provide genuine, solution-focused customer support.

Smarter Operations Mean Happier Customers

The efficiencies gained from predictive analytics aren't just about cutting costs; they translate directly into a smoother, faster, and more intuitive journey for the policyholder. A good analytics strategy lays the groundwork for a modern, client-first insurance experience.

Here’s how those internal improvements lead to real-world customer benefits:

Intelligent Claim Routing: Imagine a complex auto claim is filed, involving multiple vehicles and injuries. A machine learning model can instantly analyze its key features, identify its unique needs, and route it straight to a specialist adjuster with the right experience. For the customer, this means no more frustrating handoffs or waiting in a general queue; the right person is on their case from day one, leading to a much faster resolution.

Anticipatory Customer Service: A chatbot backed by predictive analytics can be more than just an FAQ machine. By looking at a customer’s policy history and recent website activity, it can figure out what they might need next. For example, if a home insurance client has been reading articles about flood damage during a week of heavy rain, the chatbot can proactively offer information on making a water damage claim. That's real value, delivered exactly when it's needed.

Relevant Product Suggestions: Forget about generic marketing blasts. Predictive models can spot life events that often trigger new insurance needs. A customer who just registered a new business or bought a bigger house could get a timely, relevant suggestion for commercial or expanded property coverage. It makes them feel understood, not just sold to.

The Direct Line from Automation to Loyalty

The Canadian insurance market is more competitive than ever, and customer experience is now a primary battleground. Predictive analytics directly connects better operational efficiency with a more customer-focused approach. Insurers are using real-time data and machine learning to automate tasks like claim routing and flagging potential fraud. This not only cuts down on manual errors and speeds up investigations but also helps insurers respond much more quickly, building customer trust along the way.

Investing in operational efficiency is fundamentally an investment in the customer relationship. Faster settlements, more accurate quotes, and personalized interactions are the tangible outcomes of a smarter, data-driven back-end.

This drive to create a seamless and responsive service builds the kind of loyalty that sticks. When customers feel their insurer is efficient, fair, and gets their individual needs, they're far less likely to shop around when it's time to renew. For a deeper look into this connection, check out our guide on creating an AI-driven customer experience in insurance. At the end of the day, boosting internal efficiency isn't just an operational goal; it's a core strategy for building a resilient, customer-focused business that can thrive in a demanding market.

Your Strategic Roadmap for Implementation

Jumping into predictive analytics isn't just a tech upgrade; it's a fundamental business shift. For any Canadian insurance firm looking to make this leap, a thoughtful, step-by-step plan is the only way to guarantee success. This roadmap breaks down the essential stages for building a predictive analytics capability that actually delivers results.

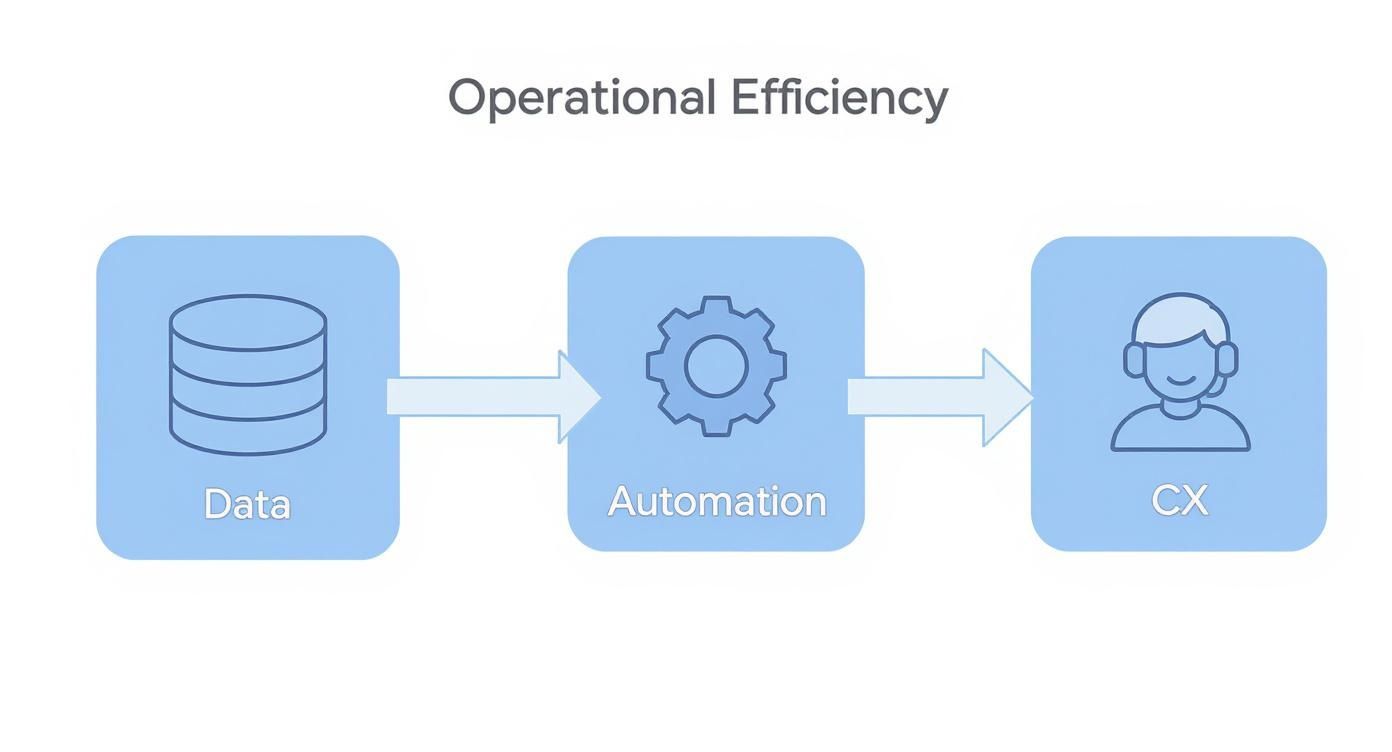

Everything starts and ends with one critical element: data governance. Think of it like building a house. You wouldn't dream of putting up walls without first pouring a solid, level foundation. Your data is that foundation. If it's messy, incomplete, or disorganized, any model you build on top of it will be wobbly at best and completely useless at worst.

The old saying "garbage in, garbage out" is the golden rule in data science. Before you do anything else, you must establish crystal-clear policies for data quality, security, and accessibility. This is the single most important step for making predictive analytics work in Canadian insurance operations.

This infographic shows how that foundational data gets turned into real-world benefits like operational efficiency and a better customer experience.

As you can see, the path begins with quality data. That data then powers automation and smarter processes, which ultimately lead to a smoother journey for your customers.

Choosing Your Technology Path

Once your data house is in order, you'll face the classic "build versus buy" dilemma. This is a major decision that hinges on your company's resources, long-term ambitions, and the talent you have on hand.

Building an In-House Team: This route gives you ultimate control. You can hire your own data scientists and engineers to build proprietary models perfectly suited to your specific business challenges. It’s a bigger investment upfront, but over time, you create a powerful, competitive asset that nobody else has.

Leveraging Third-Party Platforms: For those looking for a faster start, partnering with a specialized vendor can be a great option. You get immediate access to proven tools and experts, which can dramatically shorten your time-to-value and lower the initial cost. It’s a smart way for firms to dip their toes in the water or for those without a deep bench of data talent.

There's no universally "right" answer here. The best path depends entirely on your strategic priorities and budget.

Fostering a Data-Driven Culture

Here's a hard truth: the best technology in the world will fail without the right culture. A successful program requires a real shift in mindset, where data becomes the common language spoken across every department. Silos are the enemy of good analytics.

The real magic happens when you get the actuaries, who live and breathe risk, talking to the data scientists who build the models, and the business leaders who set the strategy. This blend of expertise is what ensures your analytics are not just technically brilliant but also strategically relevant and, most importantly, actionable.

This kind of collaborative environment is what turns raw model outputs into solutions for real business problems.

Start Small and Prove Value

Whatever you do, don't try to boil the ocean. A massive, company-wide rollout from day one is a recipe for disaster. Instead, kick things off with a well-defined pilot project. Pick one specific, high-impact problem to solve, like getting better at spotting fraud in a single line of business or predicting which customers are most likely to leave.

A successful pilot project is a game-changer. It does two things beautifully:

It delivers a clear, measurable ROI, which makes getting budget for the next phase a whole lot easier.

It creates believers out of executives and other key stakeholders, building the momentum you need for a wider rollout.

By securing a focused, early win, you can iron out your processes, fine-tune your models, and build the internal support necessary to scale your predictive analytics capabilities across your entire Canadian operation.

Navigating Canadian Regulatory and Ethical Waters

Rolling out predictive analytics isn't just a tech project; it's a massive responsibility. In Canada, insurers wading into these powerful waters must navigate a complex web of regulations and ethical questions. Getting this right is fundamental to maintaining public trust and simply operating within the law.

This means every application of predictive analytics in Canadian insurance operations has to be built on a solid foundation of compliance. The use of personal information is tightly controlled by both federal and provincial privacy laws.

The big one, of course, is the Personal Information Protection and Electronic Documents Act (PIPEDA). This federal law sets the national standard for how private companies collect, use, and share personal information. For insurers, this means data handling has to be transparent and absolutely secure.

The Challenge of Algorithmic Bias

Beyond the black-and-white of the law lies the ethical minefield of algorithmic bias. Here’s the problem: a predictive model is only as good and as fair as the historical data it learns from. If your past data contains traces of societal bias, your new, shiny model can accidentally perpetuate or even amplify those same prejudices.

Imagine a model that starts quoting higher premiums or denying more claims for people in certain postal codes. The algorithm isn't being malicious; it's just spotting correlations in old data that may be linked to demographics or other protected characteristics, not true individual risk.

This isn't just an ethical stumble; it attacks the very principle of fairness that the entire insurance industry is built on. That’s why actively hunting for and rooting out bias isn't just a "nice-to-have", it's a critical step in building responsible models.

A model that is technically accurate but systematically unfair is a failure. The goal is to build systems that are not only predictive but also equitable, ensuring that every customer is assessed on their own merits.

Building Fair and Explainable Models

To do this right, Canadian insurers need to be obsessed with creating models that are fair, transparent, and explainable. You have to be able to explain, to a customer or a regulator, exactly why a decision was made.

Here are a few core principles to guide you:

Bias Detection Audits: Don't just build a model and walk away. Regularly test it against diverse datasets to spot and fix any skewed outcomes that might be affecting certain groups of people.

Transparent Data Usage: Be upfront with customers. Tell them what data you’re collecting and how it's being used to price their policy or handle their claim.

Model Explainability: Whenever possible, choose algorithms that aren't a complete "black box." If a customer asks why their premium went up, your team needs a better answer than "the computer said so." They need to provide a clear, data-backed reason.

Finding this balance is key. If you want to dive deeper into these issues, our guide on AI and data privacy in insurance is a great resource. By making fairness and transparency a core part of their analytics strategy, Canadian insurers can use this technology not just to improve efficiency, but to build real, lasting trust with the people they serve.

Gaining the Competitive Edge in Canadian Insurance

In the fast-moving Canadian insurance market, predictive analytics isn't some far-off concept anymore, it's become the engine for growth and, frankly, for survival. The benefits are hitting home: from pinpoint-accurate risk modelling and smoother claims processing to creating genuinely personal customer experiences, this technology builds a more resilient and efficient business. Insurers who get on board with this data-first mindset are carving out a serious competitive advantage.

And the horizon looks even more interesting. We're seeing the integration of artificial intelligence with real-time data from Internet of Things (IoT) devices, such as vehicle telematics or smart home sensors, which adds incredible new layers of precision. This shift allows for truly dynamic underwriting and lets insurers get ahead of risks, moving the whole industry from a reactive stance to a proactive one.

The Future Outlook for Canadian Insurers

One of the biggest trends right now is the deep fusion of AI with predictive analytics. This powerful combination is fundamentally changing how insurers operate by automating once-manual processes and sharpening risk assessment to a fine point. The Canadian General Insurance Market is forecast to hit USD 87,562 million by 2030, a powerful indicator that technological adoption is the key to unlocking future growth. You can dive deeper into this market forecast in MarkNtel Advisors' research.

This move from static analysis to predictive intelligence is about more than just numbers; it’s about creating real value for clients and stakeholders. To see how this translates directly into revenue and a stronger market position, it's worth reviewing some dedicated strategies for predictive analytics in sales.

The ultimate goal is to build an insurance operation that is not just prepared for the future but is actively shaping it. This means being more agile, more customer-centric, and more intelligent in every decision.

For Canadian insurers, the path forward is clear. Committing to a data-driven strategy is the only way to build a more profitable, efficient, and customer-focused business that's ready for whatever comes next.

At Cleffex Digital Ltd, we help businesses solve complex challenges with innovative technology and agile practices. Discover how our custom software solutions can power your data-driven transformation. Visit us to learn more.